Resources

A Financial Instrument is any contract that gives rise to a financial asset of one entity and a financial liability or equity instrument of another entity (IAS 32.11).

Classification

Financial instruments are essentially contracts between two parties that create enforceable rights and obligations.

Broad Categories (IAS 32)

From a balance sheet perspective, instruments are categorized as:

- Financial Assets: Contractual right to receive economic benefits (e.g., cash, receivables, equity of another entity).

- Financial Liabilities: Contractual obligation to deliver economic benefits (e.g., payables, bonds issued).

- Equity Instruments: Contracts that act as legally recognized evidence of ownership rights in an enterprise (e.g., ordinary shares).

Measurement Categories (IFRS 9)

For recognition and measurement purposes, financial instruments are classified into three specific types:

1. Debt Instruments

Contractual obligations of the issuer to repay the lender in accordance with a specified maturity and under the contractual terms (e.g., bonds, loans).

2. Equity Instruments

Contracts that act as legally recognized evidence of ownership rights in an enterprise, for example, ordinary shares. They represent a residual interest in the assets of an entity after deducting liabilities.

3. Derivatives

A derivative is a financial instrument whose value is derived from an underlying variable. According to IFRS 9, it must meet three characteristics:

- Its value changes in response to an underlying (e.g., interest rate, price, index).

- It requires no or little initial net investment.

- It is settled at a future date.

Options vs. Forwards

There is a fundamental difference in the “obligation” aspect of these instruments:

| Feature | Options | Forwards (& Futures) |

|---|---|---|

| Nature | A right, but not an obligation. | Both a right and an obligation. |

| Execution | Only executed if favorable (Calls/Puts). | Must be settled at the fixed future date. |

| Value | Cannot have a negative value (worst case is zero). | Can have a positive (asset) or negative (liability) value. |

| Examples | Call: Buy Siemens stock at 140 on June 30. Put: Sell Siemens stock at 120 on June 30. | Speculation: Obligation to buy/sell crude oil at 80 USD on June 30. |

Hedging vs. Speculation

While forwards are often used for hedging (reducing price risk), this course focuses on their use for speculation, where the measurement rules below apply. Standardized forwards traded on exchanges are called Futures.

Recognition and Measurement

The accounting lifecycle of a financial instrument follows specific rules for when it enters the books and how its value is updated.

Recognition & Initial Measurement

All financial instruments are recognized on the balance sheet exactly when the entity becomes a party to the contractual provisions of the instrument (IFRS 9.3.1.1). It is initially measured at its Fair Value plus or minus any transaction costs that are directly attributable to the acquisition or issue of the financial instrument. The only exception is for instruments classified as FVTPL, which are measured at Fair Value without including transaction costs.

| Standard | Initial Measurement Rule |

|---|---|

| IFRS 9 | Fair Value transaction costs. (Exception: FVTPL is Fair Value only). |

| German GAAP | Always at Cost (including transaction costs). |

Subsequent Measurement (IFRS 9)

Subsequent measurement determines how changes in value are recorded over time. It depends heavily on the type of instrument and the intent behind holding it.

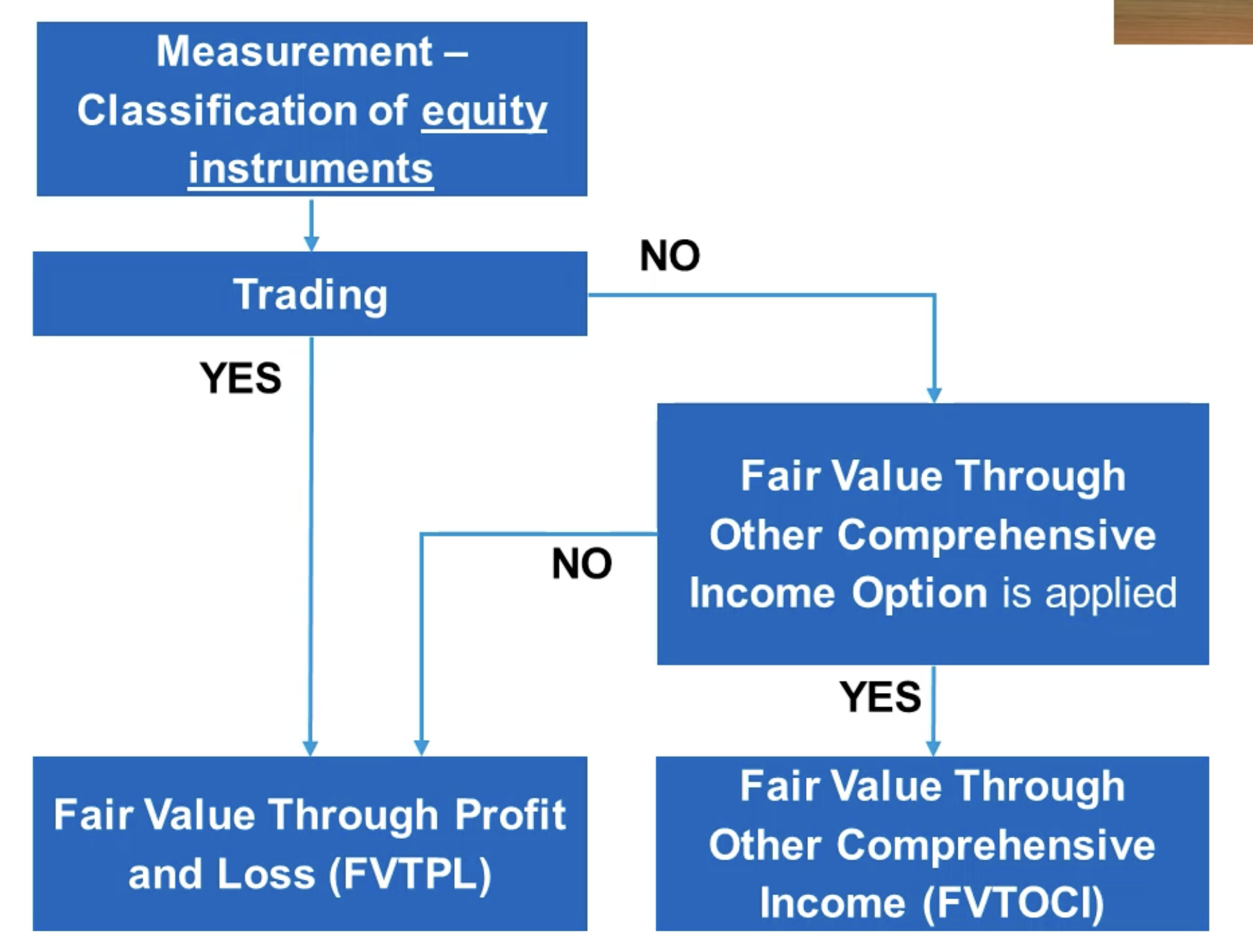

Equity Instruments

Equity instruments (e.g., shares in other companies) are always measured at Fair Value. The distinction lies in where the value changes are recorded.

| Scenario | Measurement Category | Details |

|---|---|---|

| Held for Trading | FVTPL (Fair Value Through Profit or Loss) | Default category. All fair value changes are recognized in Net Income. |

| Not Held for Trading (Strategic Investment) | FVTPL (Default) | Unless the option below is chosen, it remains FVTPL. |

| FVTOCI (Fair Value Through Other Comprehensive Income) | Irrevocable Option at initial recognition. - Fair value changes go to OCI (Equity). - Only dividends are recognized in Net Income. - No recycling: Gains/Losses are never moved to Net Income, even on sale. |

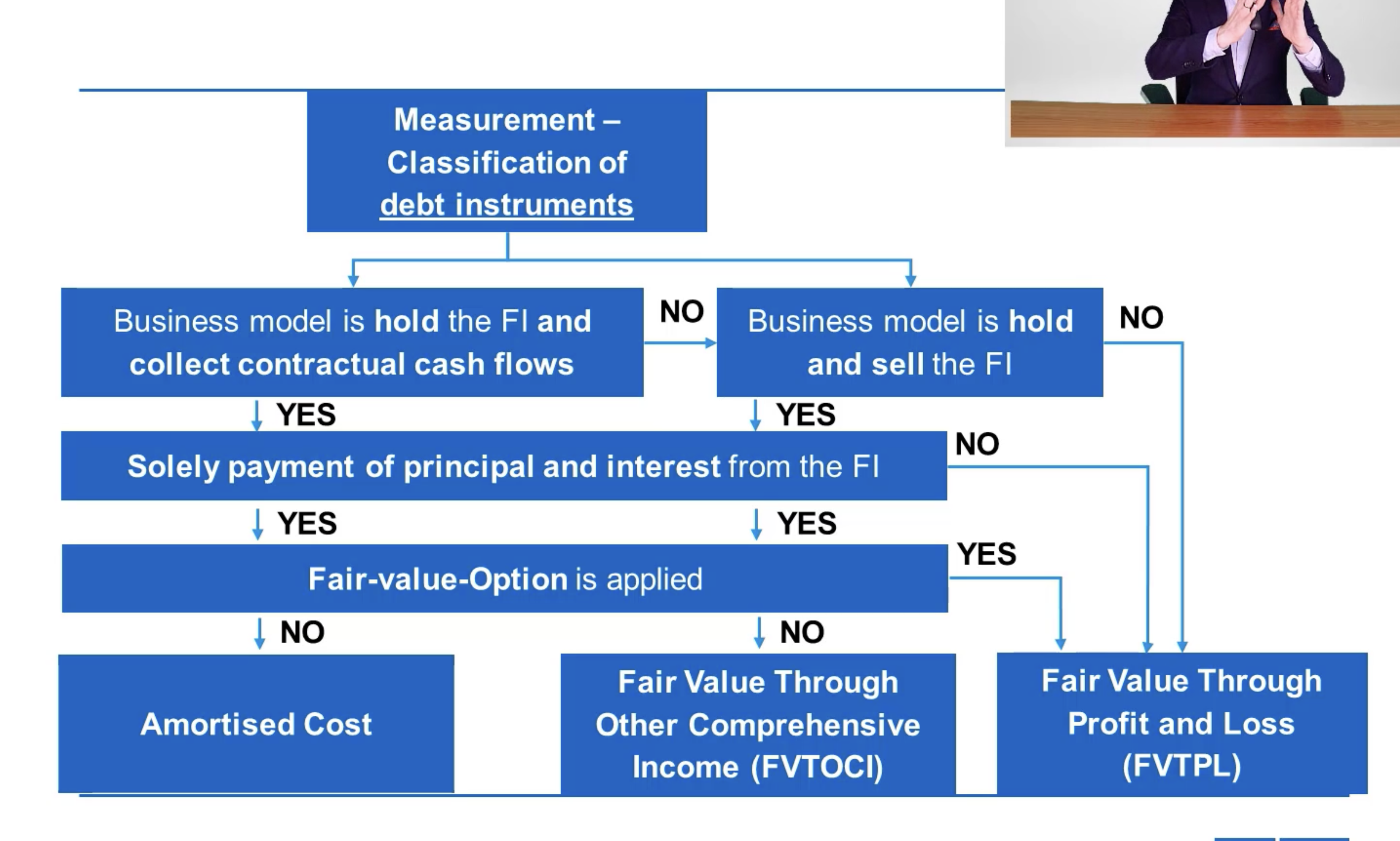

Debt Instruments

For debt instruments (e.g., bonds, loans), the measurement category is determined by two tests: the Business Model Test and the SPPI Test (Solely Payments of Principal and Interest).

SPPI Test (Contractual Cash Flow Characteristics)

Do the contractual terms give rise to cash flows that are solely payments of principal and interest? Are they not linked to changes in equity or commodity prices?

- Pass: Proceed to Business Model Test.

- Fail: Must be measured at FVTPL.

If SPPI is passed, the Business Model determines the measurement:

| Business Model | Goal | Measurement Category |

|---|---|---|

| Hold to Collect | Hold asset to collect contractual cash flows (Principal + Interest). | Amortized Cost |

| Hold to Collect & Sell | Both collecting cash flows and selling financial assets are integral. | FVTOCI (with recycling)* |

| Other / Residual | Held for trading, or management performance managed on fair value basis. | FVTPL |

*Note for Debt FVTOCI: Interest income, impairment, and FX effects are in Net Income. Other FV changes are in OCI. On sale, accumulated OCI is “recycled” to Net Income.

Derivatives

The subsequent measurement of derivatives is always at Fair Value Through Profit and Loss (FVTPL). There are no other options (unless hedge accounting is applied, which is out of scope).

Comparison with German GAAP

German GAAP (HGB) differs significantly as it does not have a legal definition of financial instruments and relies on the realization and prudence principles.

Lower of Cost or Market Value (LCM)

Under German GAAP, subsequent measurement is at cost less impairment.

- Permanent Impairment: Must always be written down to the lower market value.

- Non-Permanent Impairment: Depends on the classification:

- Non-Current Assets (Strategic interest): Diluted LCM (Option to write down).

- Current Assets (Trading purpose): Strict LCM (Obligation to write down).