Resources

- Learning Path as PDF

There will be an EY guest lecture for this topic.

Corporate Sustainability

Sustainable Development

As defined in the Brundtland Report (1987), this is development that meets the needs of the present without compromising the ability of future generations to meet their own needs. The two key concepts:

- Needs: Basic needs of the world’s poor should be prioritized.

- Limitations: Technological and social progress should be harnessed to reduce environmental degradation and improve resource management.

There are four main dimensions of corporate sustainability:

- Economic Sustainability: Ensuring that economic growth is inclusive and benefits all segments of society. This includes long-term profitability, innovation, and economic resilience.

- Societal Sustainability: Promoting social equity, cohesion, and inclusion. For example, fair labor practices, community engagement, and human rights.

- Environmental Sustainability: Protecting natural resources and ecosystems for future generations. e.g., reducing carbon footprint, waste management, and sustainable resource use.

- Governance / Institutional Sustainability: Building effective, accountable, and inclusive institutions. This includes data privacy, transparency, and ethical business practices.

To achieve sustainable development, integrated approaches are necessary, considering the interconnections between these dimensions.

Triple Bottom Line

The Triple Bottom Line (TBL) framework expands the traditional reporting framework to include social and environmental performance alongside financial performance. The three pillars are People (social), Planet (environmental), and Profit (economic).

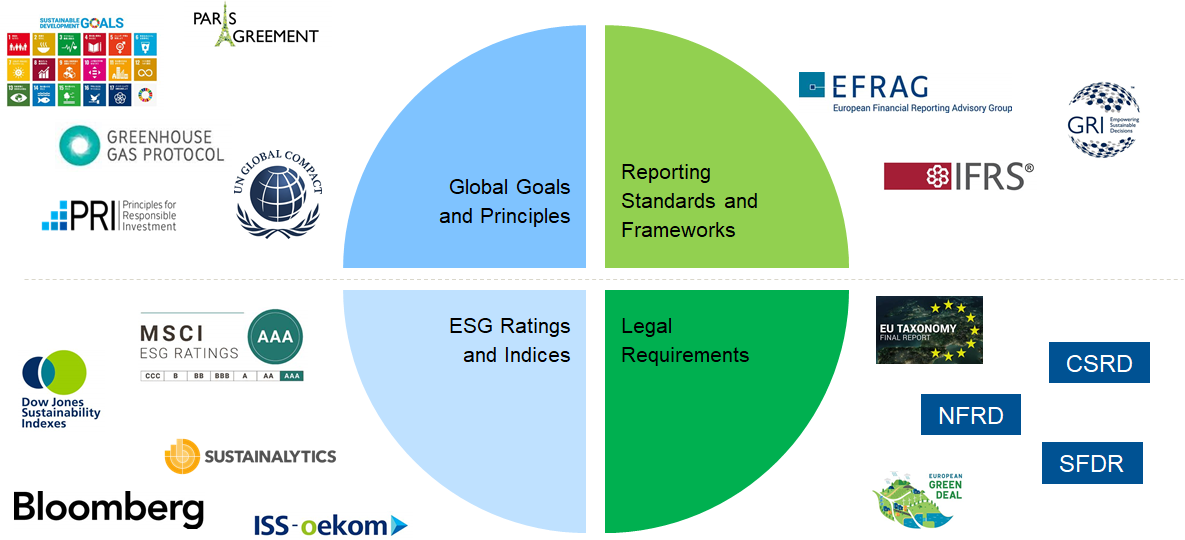

Reporting Landscape

Standards and rules for sustainability reporting are set by various organizations and regulatory bodies:

- Legal Requirements like the European Green Deal

- Reporting Standards and Frameworks, such as the GRI, ISSB, and EFRAG

- ESG Ratings assessing companies on non-financials, e.g. the Dow Jones Sustainability Index

- Global Initiatives promoting sustainability practices, like SDGs, Paris Agreement, or the GHG Protocol. GRI provides guidance on linking corporate reporting to SDGs.

European Green Deal

The EU Sustainable Finance framework aims to reorient capital flows towards sustainable investments, manage financial risks stemming from climate change, and foster transparency and long-termism in financial and economic activities. It is built around three main pillars:

- EU Taxonomy: A classification system establishing a list of environmentally sustainable economic activities.

- Corporate Sustainability Reporting Directive (CSRD): A directive that mandates large companies to disclose information on their sustainability practices and impacts.

- Sustainable Finance Disclosure Regulation (SFDR): A regulation requiring financial market participants to disclose how they integrate sustainability risks and consider adverse sustainability impacts in their investment decision-making processes.

EU Taxonomy

The EU Taxonomy is a classification system that establishes a list of environmentally sustainable economic activities. It aims to provide companies, investors, and policymakers with definitions to guide investment decisions towards sustainable projects and activities.

The Taxonomy requires companies subject to the CSRD to report capital expenditure (investments in long-term assets for business operation) and operational expenditure (ongoing costs for running business operations) that are sustainable (in line with the Taxonomy).

EU Reporting Requirements: CSRD and NFRD

The CSRD expands and replaces the previous NFRD (2017-2024, planned), significantly increasing the number of companies required to report on sustainability matters and enhancing the detail and scope of the information to be disclosed.

Non-Financial Reporting Directive (NFRD)

The NFRD (Directive 2014/95/EU) requires public-interest companies (listed companies, creditors, insurances) with 500+ employees to disclose non-financial information related to:

- Environmental matters

- Social and employee aspects

- Respect for human rights

- Anti-corruption and bribery issues

- Diversity policies applied to administrative, management, supervisory bodies

This applies since 2017 financial years, but is now being replaced by the CSRD. The non-financial statement may rely on recognized frameworks and be included in the management report or as a separate report, and auditing is limited to the provision of the report.

Corporate Sustainability Reporting Directive (CSRD)

The CSRD (Directive 2022/2464/EU) expands the scope of sustainability reporting requirements to all large companies as wave 2, and listed SMEs as wave 3 (planned in 2026). It introduces more detailed reporting requirements:

- Increase in the level of detail and scope of sustainability information, including scope 1 (direct), scope 2 (indirect from purchased energy), and scope 3 (other indirect) emissions, pollution, waste, water management, etc.

- Mandatory audit of reported sustainability information

- Mandatory reporting in line with the European Sustainability Reporting Standards (ESRS)

- Obligation to digitally tag reported information for machine readability

Despite being in force on the EU level since 2023, it is not yet implemented in Germany. In the meantime, it was postponed and may be weakened by the Omnibus regulation (see below).

ESRS, or European Sustainability Reporting Standards, are being developed by EFRAG (European Financial Reporting Advisory Group) to provide detailed guidelines for reports and better international comparability.

Omnibus

The Omnibus sustainability rules simplification amendment postponed CSRD implementation by 2 years. Additionally, there is a political agreement to exclude SMEs from the reporting obligation, increase the threshold to 1000 employees, add a 40 million EUR revenue threshold, and exclude certain categories of companies (e.g. financial holdings). This, however, has not been adopted yet.

Sustainable Finance Disclosure Regulation (SFDR)

The SFDR requires financial market participants and financial advisors to disclose how they integrate sustainability risks and consider adverse sustainability impacts in their investment decision-making processes, or how sustainability risks may affects a product’s performance. The regulation aims to increase transparency in the market for sustainable investment products, prevent greenwashing, and ensure comparability across financial products.

Sustainable Reporting Standards

There are many different standard setters and frameworks for sustainability reporting. Some of the most prominent ones include the Global Reporting Initiative (GRI), the European Financial Reporting Advisory Group (EFRAG), and the International Sustainability Standards Board (ISSB).

| Dimension | GRI | EFRAG (ESRS / CSRD) | ISSB (IFRS S1/S2) |

|---|---|---|---|

| Scope | Voluntary, widely used worldwide | Mandatory for in-scope EU companies; ESRS set 1 adopted, more coming | Global baseline disclosures for capital markets |

| Focus | Broad sustainability impacts (E/S/“economic”) | Broad ESG via ESRS E, S, G | Enterprise-value risks & opportunities; climate standard in place (IFRS S2) |

| Structure | Universal + Sector + Topic standards | Cross-cutting + Topical + Sector-specific (planned) | One general (IFRS S1) + one climate (IFRS S2); no sector-specific |

| Materiality | Impact materiality | Double materiality (impact + financial) | Financial materiality (enterprise value) |

Global Reporting Initiative (GRI)

The independent GRI framework is the de-facto global standard for sustainability reporting. It provides a comprehensive set of standards covering economic, environmental, and social impacts. GRI standards are widely used by organizations around the world to report on their sustainability performance.

The GRI system is modular, consisting of:

- Universal Standards: Applicable to all organizations

GRI 1: Principles for using the standards

GRI 2: General Disclosures

GRI 3: Material Topics - Sector Standards: Industry-specific disclosures

- Topic Standards: Disclosures on specific sustainability topics (e.g., GRI 305 for Emissions, GRI 403 for Occupational Health and Safety)

A key concept in GRI is “Impact”, which has to be considered across the three dimensions (economy, environment, people.

Material topics are those that reflect the organization’s significant impacts or influence the assessments and decisions of stakeholders. Sector standards provide a list of potential material topics for specific industries, while topic standards provide detailed disclosure requirements for each material topic.

European Financial Reporting Advisory Group (EFRAG)

In the area of financial reporting, EFRAG plays a key advisory role in the EU endorsement process of IFRS standards. In sustainability reporting, EFRAG develops the European Sustainability Reporting Standards (ESRS) on behalf of the European Commission.

The ESRS is built on 3 layers:

Sector-Agnostic Standards in ESRS

These standards apply to all companies, regardless of their industry or sector. They cover general sustainability disclosures that are relevant across different types of organizations.

- Cross-cutting standards: Cover general sustainability disclosures applicable to all companies (e.g., governance, strategy, risk management). They define concepts and principles, including double materiality (impact on people and environment as well as financial impacts on the company).

- Topical standards: Address specific sustainability topics (e.g., ESRS E1 climate change) with detailed disclosure requirements regarding impacts, risks, opportunities, targets, and performance metrics.

Sector-Specific Standards in ESRS

These standards provide additional disclosure requirements tailored to specific industries. They recognize that different sectors have unique sustainability challenges and impacts that need to be addressed in reporting.

These standards increase comparability within sectors by requiring disclosure on typical material topics, alongside the sector-agnostic standards.

Entity-Specific and SME Standards in ESRS

This layer addresses case where the general ESRS don’t cover a material matter in specifics, or for smaller entities (though mandatory reporting for SMEs may be cancelled with Omnibus).

If a company has material impacts/risks/opportunities that are not sufficiently covered by ESRS, it must provide additional entity-specific disclosures to ensure users can understand those matters.

For SMEs, there is a voluntary standard with simplified and modular disclosure requirements to ease the reporting burden (VSME).

International Sustainability Standards Board (ISSB)

The ISSB exists next to the IASB under the IFRS Foundation and focuses on developing global sustainability disclosure standards. The ISSB aims to create a comprehensive global baseline of sustainability-related disclosure standards to meet investors’ information needs.

So far, two standards have been issued:

- IFRS S1: General Requirements for Disclosure of Sustainability-related Financial Information

- IFRS S2: Climate-related Disclosures, following the four pillars, e.g. GHG in all scopes