Resources

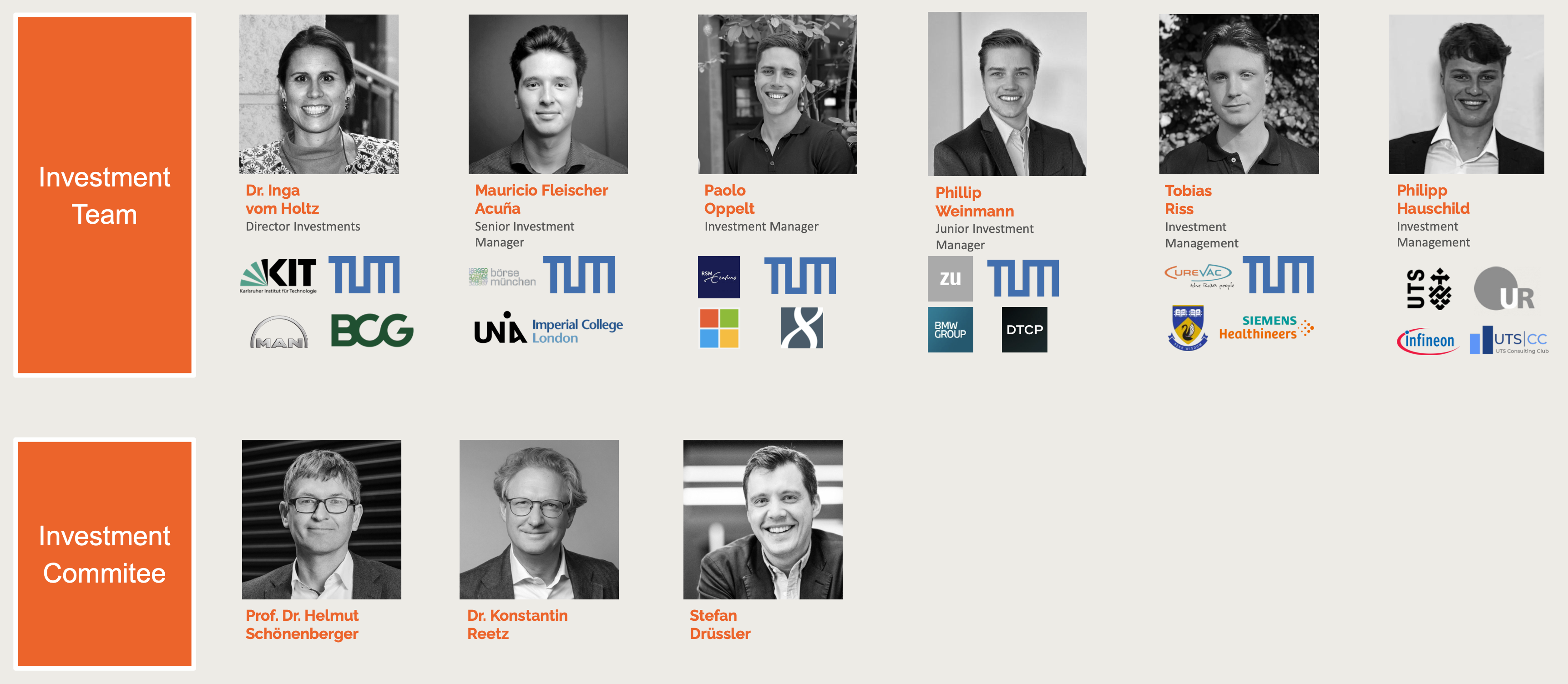

Dr. Inga vom Holtz

Director Investments at UnternehmerTUM, managing the pre-seed initiative “Funding for Innovators,” investing in early-stage B2B deep-tech startups from the UnternehmerTUM ecosystem.

Awarded “Investor of the Year 2025” by Startup-Verband.

Background: started at BCG, worked closely with innovative ventures during her PhD at TUM, returned to the automotive world, then decided she really wanted to work with startups.

Phillip Weinmann

Junior Investment Manager at UnternehmerTUM.

Background: BMW Startup Garage (identifying and collaborating with startups in the automotive sector), then early-stage startup in Berlin, followed by a stay in Silicon Valley for more exposure to the startup ecosystem.

Startups and Venture Capital

Startups:

- Founder-led

- Use an innovative process or product to solve a market problem

- High uncertainty and risk

- High growth potential

- Often struggle to secure funding due to lack of track record and collateral

Venture capital (VC):

- Provides equity financing to startups in exchange for ownership stakes

- Shares both risk and potential upside with founders

- Not the only way to found a company (bootstrapping is an alternative)

- Particularly valuable for startups that need high-paced:

- Growth

- Innovation

- Employment

- Capital

The VC industry is very small. When applying to multiple, do not tell them you are applying elsewhere (especially the name).

VCs are more than money, they bring expertise, network, credibility, and support. Therefore, choosing the right investor is not only dependent on valuation but also on strategic fit.

Bootstrapping:

- Can be a viable way to start

- But when competing with well-funded rivals, lack of capital becomes a major risk

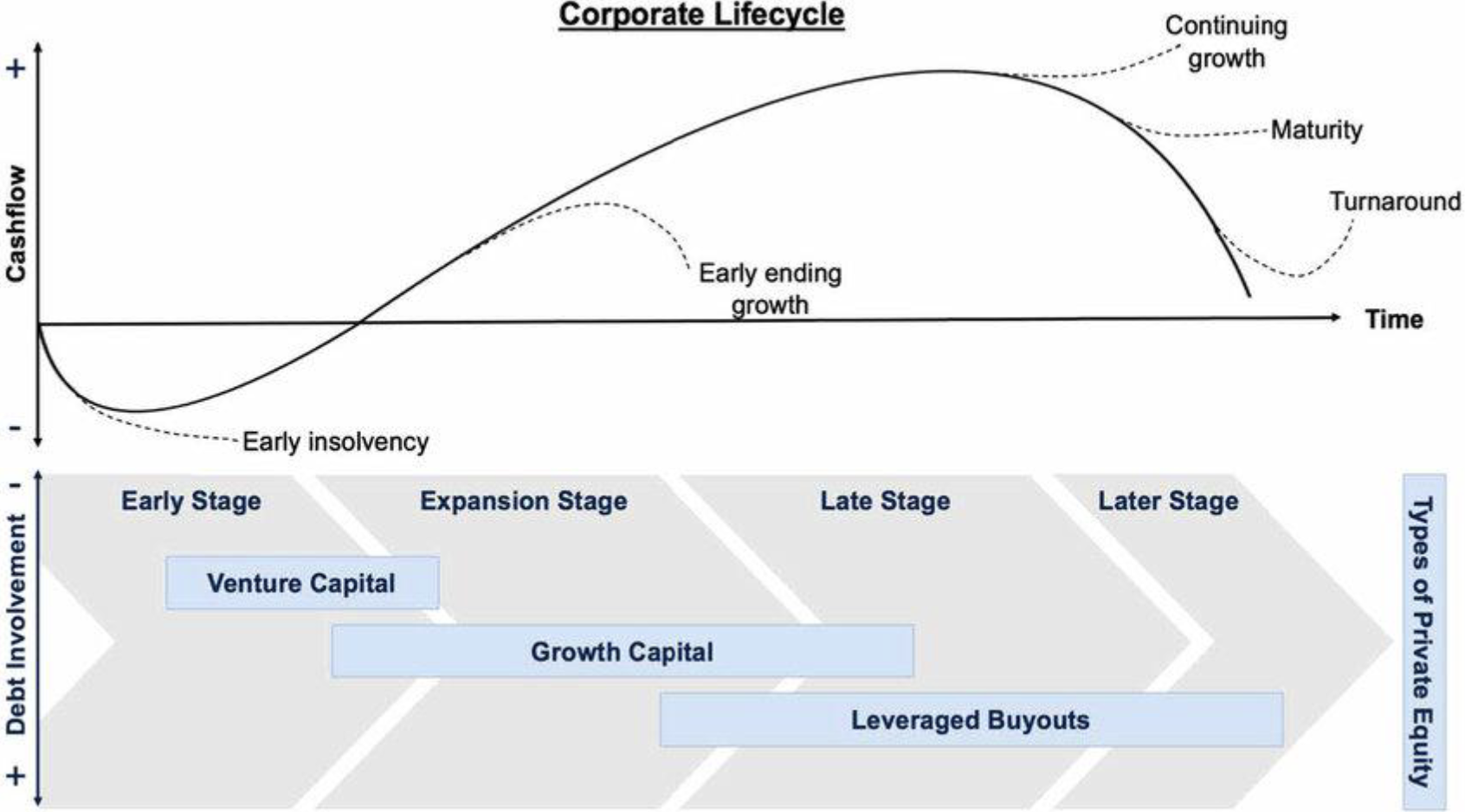

Financing Phases

In the early stages, startups exhibit negative cash flow, requiring upfront investment (bootstrapping, founding grants). They need to avoid early insolvency and may raise venture capital to finance growth and development.

In the expansion stage, growth capital can help scale operations, enter new markets, and develop new products. Here, early ending growth should be avoided.

In later stages, leverage buyouts or IPOs can provide liquidity for investors and founders, while also fueling further growth. The venture may continue growing, reach maturity, face decline, or turn around.

UnternehmerTUM and Ecosystem

Role of UnternehmerTUM

- Largest European entrepreneurship center, supporting teams from idea to IPO.

- Close connection to TUM and the broader innovation ecosystem.

2024 highlights

In 2024, UnternehmerTUM and its ecosystem achieved:

- 1100+ startup teams supported

- 120+ new scale-ups created

- 2bn+ EUR in funding raised by startups

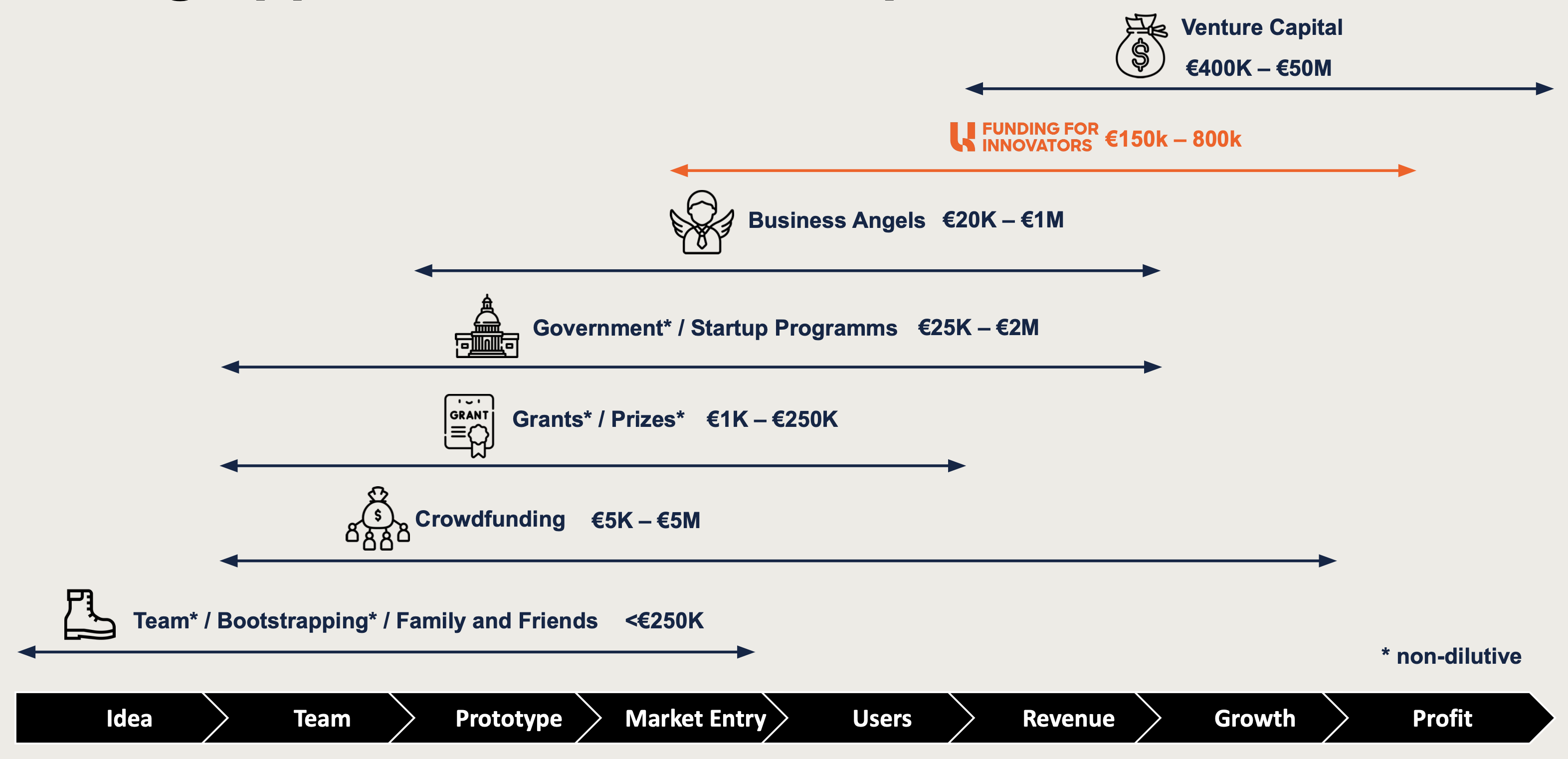

Funding for Innovators

UnternehmerTUM Funding for Innovators is a pre-seed fund focused on B2B deep-tech startups from the UnternehmerTUM ecosystem.

- Invests in roughly 8–10 startups per year

- Focus: deep-tech ventures with high growth and scalability

- Stage: very early (pre-seed), before or around first significant funding rounds

Team

Opportunities

Funding for Innovators offers three main types of support:

- Prototyping grants

- Two rounds per year

- For deep-tech solutions needing capital to build their prototype

- Pre-Seed Capital program

- For deep-tech startups aiming to close their first funding gap

- Follow-on funding

- Additional investment in later rounds on an individual basis

- Requires a lead investor in the round

Assessment Criteria

Formal Requirements

A startup should:

- Be part of the UTUM ecosystem (e.g., incubated at TUM and often already associated with UnternehmerTUM)

- Be B2B and deep-tech focused (no B2C)

- Have at least one team member who completed a Master’s or PhD, and be founded as a team (not a solo founder)

- Hold the relevant intellectual property within the company

- Represent a strong VC case:

- High growth potential

- Scalable business model

- Not yet at IPO stage (obviously)

- Have a reasonable valuation

- If valuation is too high, future funding becomes difficult

- FFI offers significant support and consulting on valuation

- Be ESG compliant

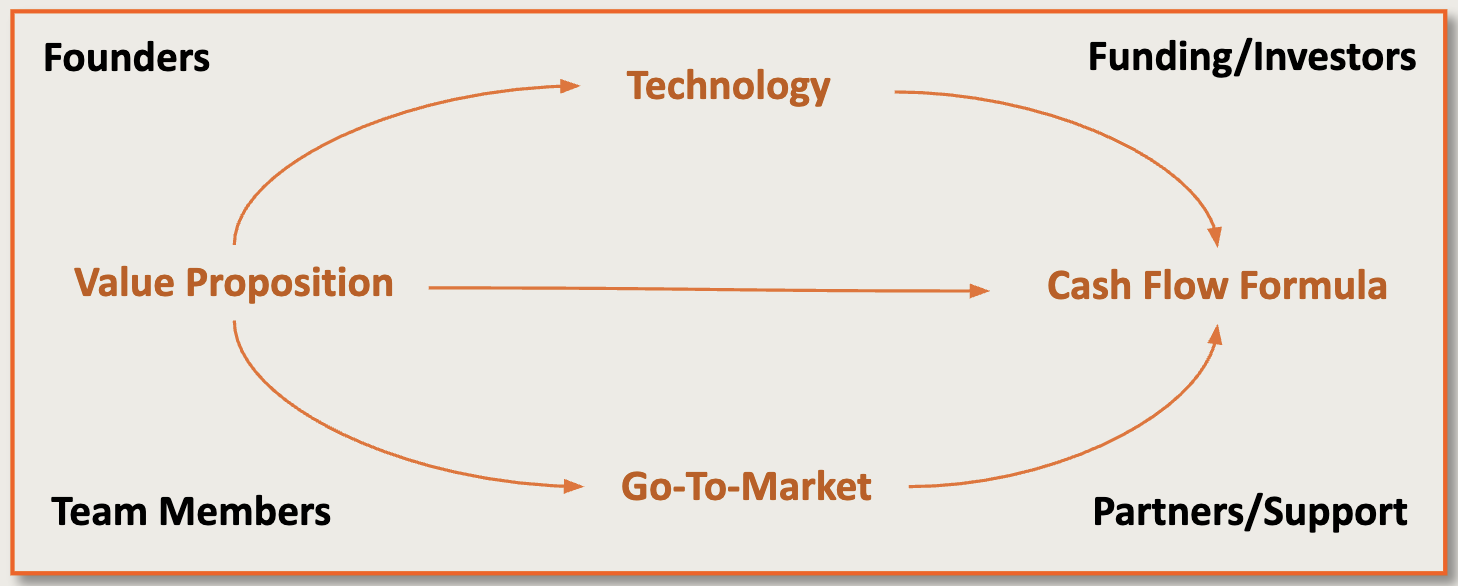

What They Look At In the Venture

Founders

- Team composition

- Commitment and ambition

- Domain expertise and ability to execute

Wider team - Capabilities beyond the founding team

- Complementary skills

Funding and investors - Existing investors

- Funding needs and runway

Partners - Collaborations with industry and ecosystem partners

Cash flow - Path to revenue and ability to generate cash flow

Value proposition - Distinctiveness vs. competitors

- Strong team and large market are not enough without a compelling value proposition

- They also talk to experts in the local industry (which works because they only invest in their ecosystem) and customers

Pre-Seed Capital

-

Process

- Team tries to be very lean and fast

- Typical process duration: 6–8 weeks

-

Instruments

- Convertible loans with “best-in-class” terms:

- No valuation cap

- No discount

- No interest

- Convert into equity after the first equity investment round

- Straight equity investments are also possible

- Convertible loans with “best-in-class” terms:

-

Application

- On a rolling basis via the UnternehmerTUM Funding for Innovators website

Questions

Q&A is transcribed and summarized by AI.

US vs. Europe for Startups

- US attracts startups: more investors, more money, one large, unified market, more risk‑friendly culture.

- Europe’s big advantage: abundant, high‑quality, cheaper talent and strong universities; good place to hire and scale teams before going to the US.

- You can stay a European/German company and still raise from US VCs; going to the US too early can cause inflated valuations and later down rounds.

Exits, Ownership, and Fund Strategy

- Ways investors “leave”:

- Trade sale/exit (sometimes very early, even pre‑Series A).

- Secondary sales in later rounds (Series B/C) when growth investors join.

- In small, early cases, founders can sometimes just pay back early investors if they switch to an SME/bootstrapped path.

- Hard to buy out investors once large equity rounds (1–3M+) have happened.

Due Diligence & Red Flags

- DD covers: team, market, product/tech; depth depends on how deep‑tech the startup is.

- They leverage professors, experts, other investors, and customers; often do 2–3 week deep dives on the tech/problem.

- VC world is small: funds talk to each other; don’t freely share which VCs you’re talking to, to avoid “networked no’s.”

- Key red flags:

- Single, inexperienced founder; bad behavior (lying, gossiping) in DD.

- Small or crowded market, unclear USP, “nice‑to‑have” not real pain point.

- Tech not well understood or not meaningfully better than state of the art.

- IP not actually controlled by the company; misaligned early strategic investor who might later try to buy cheap.

Valuation & Terms

- Early valuations are mainly negotiation + demand: multiple experts/investors, but no hard formula at pre‑seed (often no revenue).

- Don’t chase the highest valuation; choose the best investors to reduce down‑round risk later.

- Market norm: very early pre‑seed investors often target ~20% of the cap table.

- They use founder‑friendly convertibles (no cap, no discount, no interest), converting at the first equity round valuation—worse for them, better for founders.

- Typical market (not them): convertibles with a valuation cap so early investors convert at a lower valuation and get rewarded for taking early risk.

- Later‑stage growth investors more often use financial metrics (e.g. ARR multiples) to set valuations; early‑stage deep tech is mostly qualitative and future‑oriented.

Pitching

- Most important: practice a lot (friends, family, low‑stakes investors) and collect feedback.

- Explain tech so simply “your grandma” would get it; keep core pitch short, with depth in Q&A.

- Always cover the key boxes: team, tech, market/pain point, market size, go‑to‑market; not only tech and not only business.

Defaults, Risk, and Hype

- Current observed insolvency in their young fund is about 10%, but it’s early in the fund life; outcomes range from up‑rounds to flat/down rounds and pay‑to‑play.

- Deep tech/hardware has higher insolvency risk due to long paths to profitability; profitability is becoming more important to reduce dependency on capital.

- VC is a “game of outliers”: a few big winners pay for many losses, but they still care about not losing teams and talent.

- Many startups, especially in hype waves (e.g. 2021–22 and in AI), are likely overvalued; some can justify it with strong ARR, but many will face down rounds/insolvencies.

- Hype is double‑edged: it drives innovation and capital inflow but also creates bubbles that later correct.

Support, Legal, ESG, Entities

- They help portfolio (and sometimes non‑portfolio) startups with intros to legal/regulatory experts, customers, fundraising contacts, and programs.

- Founders should always hire a good lawyer; early legal mistakes in contracts are expensive or impossible to fix later.

- ESG and reporting are required mainly to force early reflection and prepare startups for later investor expectations; specifics vary by industry, and they look more at mindset than fixed checklists.

- Funding sources: mix in general (HNWIs, institutions, corporates); in their case, money ultimately comes via Unternehmertum, owned by entrepreneur Susanne Klatten (incl. BMW stakes).

- Legal entities:

- No entity required for very small prototyping grants (up to ~€5k).

- Pre‑seed investments require a legal entity; so far they invest only in German entities, EU might come later but is complex.