Resources

- Learning Path as PDF

- Dinh et al, Signaling or Earnings Management? (p. 373-376, 2nd paragraph)

Intangible Assets are abstract, contrary to Tangible Assets.

Intangible Assets

An asset is intangible if it is (IAS 38):

- Identifiable: separable or arises from contractual or legal rights; it could be sold or transferred individually. Assets arising from contractual rights are e.g. temporary licenses or construction permits.

- Non-monetary: does not represent a claim to cash or another financial asset

- Without physical substance: does not have a physical form

Examples include patents, copyrights, trademarks, customer data, brand names, software, and videos. Today, most assets are intangible, especially in the tech industry.

Goodwill is a special case of intangible assets under IFRS that arises when a company acquires another company for more than the fair value of its net identifiable assets.

Capitalized intangible assets are recognized as assets instead of expensed, meaning they are recorded on the balance sheet as assets and amortized over their useful life.

Evaluating Potential for Innovation

While intangible assets can be an outcome of successful innovation, they cannot serve as the only indicator. Most R&D is expensed immediately in the income statement (often shown either as R&D expense, within operating expenses, or sometimes within cost of goods sold) and does not lead to intangible assets (as capitalized R&D expenses). Furthermore, R&D costs also include the depreciation/amortisation of capitalized R&D from previous periods.

Recognition

An intangible asset is recognized if:

- It is probable that future economic benefits attributable to the asset will flow to the entity

- The cost of the asset can be measured reliably

Acquired Intangible Assets

These criteria are assumed to be fulfilled upon acquisition, therefore all acquired intangible assets are recognized in the balance sheet.

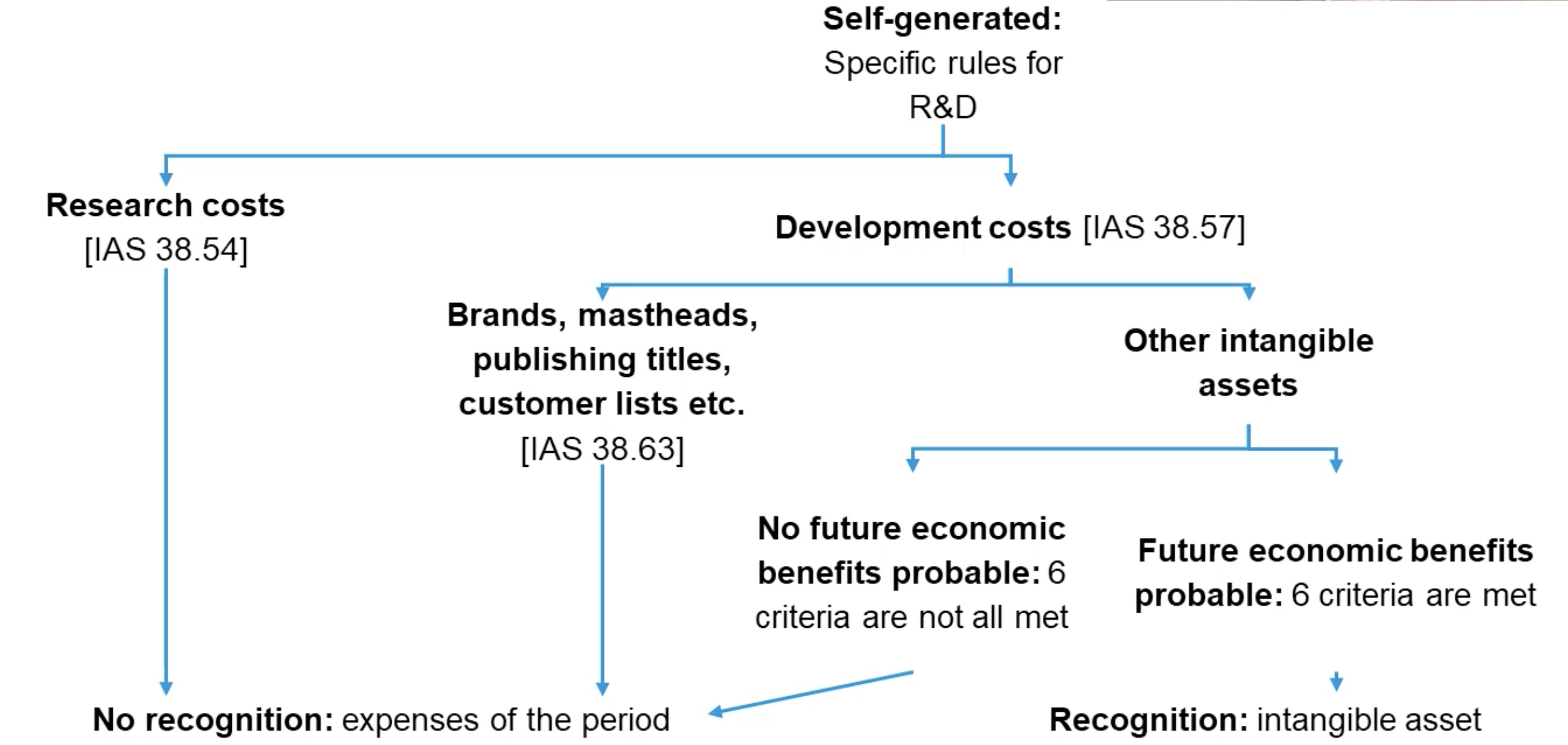

Self-generated Intangible Assets

For self-generated intangible assets, specifically research and development activities, specific requirements apply:

- Research costs are not recognized and are expensed in the period.

- The same applies to marketing-related intangible assets (brands, customer lists, publishing titles), referred to as prohibited internally generated assets because they do not meet the recognition criteria and must be expensed.

- For the remaining other intangible assets, there are 6 recognition criteria must all be met for capitalization:

- technical feasibility of completing the intangible asset for use or sale

- intention to complete it

- ability to use or sell

- availability of resources: technical, financial, etc

- probable future economic benefits: existence of market or usefulness for internal purposes

- ability to measure costs reliably

- Assets matching these criteria must be capitalized under IFRS, under German GAAP it is optional to capitalize development costs.

Research vs. Development

Research expenses cannot be capitalized. Therefore, when deciding whether to capitalize or expense costs, it’s important to differentiate between research and development activities. If research and development cannot be separated, the entire activity is expensed (not capitalized).

- Research is the original and planned investigation undertaken with the prospect of gaining new scientific or technical knowledge and understanding.

Examples: activities aimed at obtaining new knowledge, searching for alternatives for materials, products, processes, systems, or services, looking for a path to commercialization - Development is the application of research findings or other knowledge to a plan or design for the production of new or substantially improved materials, products, processes, systems, or services before commercial production or use.

Examples: design, construction, and testing of pre-production prototypes and models

Prohibited costs that must be expensed include:

- Advertising and promotional activities, including customer data

- Start-up costs, including pre-opening and pre-operating costs

- Training costs

Initial Measurement

Intangible assets are initially measured at cost. Therefore,

-

for purchased intangible assets, the same principles as for tangible assets apply: purchase price plus directly attributable costs to prepare the asset for use

-

for self-generated intangible assets, only costs incurred during the development phase that meet the recognition criteria are capitalized, including e.g. materials, services, employee costs, and an appropriate portion of overheads. Costs incurred during the research phase and other prohibited costs must be expensed as incurred.

Subsequent Measurement

For subsequent measurement, an entity can choose between the cost model and the revaluation model.

The models are very similar to those used for tangible assets, however:

- Instead of calling it depreciation, intangible assets are amortized over their useful life (same concept).

- The revaluation model can only be applied if there is an active market for the asset, which is less common for intangibles. An active market cannot exist for brands, publishing rights, patents or trademarks, therefore the cost model is applied.

- Intangible assets may have finite or infinite useful lives. For the latter, an impairment-only approach is used instead of amortization.

Under German GAAP, intangible assets are not revalued, but amortized over their useful life (cost model only). In case of an infinite useful life, it is amortized over 10 years.

Intangible Assets with Infinite Useful Lives

Under IFRS, when there is no foreseeable end to the period over which the asset generates cash flows, the asset is considered to have an infinite useful life. In this case, amortization cannot be applied. Instead, impairment tests must be conducted annually and on indication.

Influence on Earnings Management

Intangible assets provide managers with significant discretion, especially through R&D capitalization decisions, which directly affect reported profit, asset values, and performance ratios.

Managers can influence earnings through:

- Capitalization vs. Expensing of Development Costs: Capitalizing development increases current assets and defers expenses into future periods (via amortization), raising current profit. Expensing immediately lowers current profit but avoids future amortization.

- Judgment in Meeting Recognition Criteria: The IAS 38 development criteria require managerial assessment (technical feasibility, economic benefits, resource availability). This judgment gives room to accelerate or delay capitalization, influencing earnings when benchmark pressure is high.

Earnings Management Implications

- Capitalizing R&D can boost current-period profit and increase total assets, improving ratios such as RoA or helping firms beat earnings benchmarks.

- Expensing R&D keeps profit conservative but may be used when poor performance is unavoidable, or to create reserves for future periods.

- Because capitalization involves discretion, it can serve both signaling (credible information about successful projects) and opportunistic earnings management. Markets often penalize capitalization when it appears opportunistic, especially when used to just meet earnings targets, but may reward it when fundamentals independently indicate strong performance.