Resources

Earnings Management

The accounting policy aims to present the net assets, financial position, and results of operations of an entity as positively as legally possible. Short-term and long-term policy objectives must be coordinated with strategic objectives and the interest of the various stakeholder:

- Stakeholders with contract income, i.e. creditors, suppliers, employees, focus on financial stability (credit risk)

- Stakeholders with residual income, i.e. shareholders, stock options holders, focus on profitability (income risk)

- Internal addressees, i.e. management/supervisory/advisory boards focus on decision-making and behavioral control

Accounting Policy / Earnings Management vs. Financial Statement Analysis

- Accounting policy / earnings management: Management intentionally uses recognition, measurement, timing, and presentation options within GAAP to influence how stakeholders judge the firm and how contracts based on accounting numbers (e.g. covenants, bonuses) are settled. (p. 2)

- Financial Statement Analysis (FSA): Analysts use the published financial statements and reports to assess the company’s current situation and future development. Accounting policy choices must be decoded when interpreting ratios and trends; see Financial Statement Analysis.

Financial-Based Accounting Policy aims to demonstrate future solvency (and influence financial-based analysis) through the balance sheet and cash flow statement: investments, financing, liquidity.

Performance-Based Accounting Policy aims to demonstrate future profitability (and influence performance-based analysis) through the income statement: profitability, earnings sources, earnings structure.

Incentives

- Performance-Based Compensation: Bonus payments are often linked to accounting numbers.

- Raising Capital: Firms may want to present better financials to attract investors before IPOs or SEOs.

- Meeting Targets: Managers may want to meet or beat forecasts, internal targets, or peer results to maintain/increase firm valuation and managerial reputation.

- Avoid Debt Covenant Violations: To avoid breaching financial KPIs agreed on with banks/investors, like having at least 30% equity.

- Quiet Life: A smooth accounting performance is less likely to attract scrutiny from board, auditors, regulators → Less to explain.

Instruments

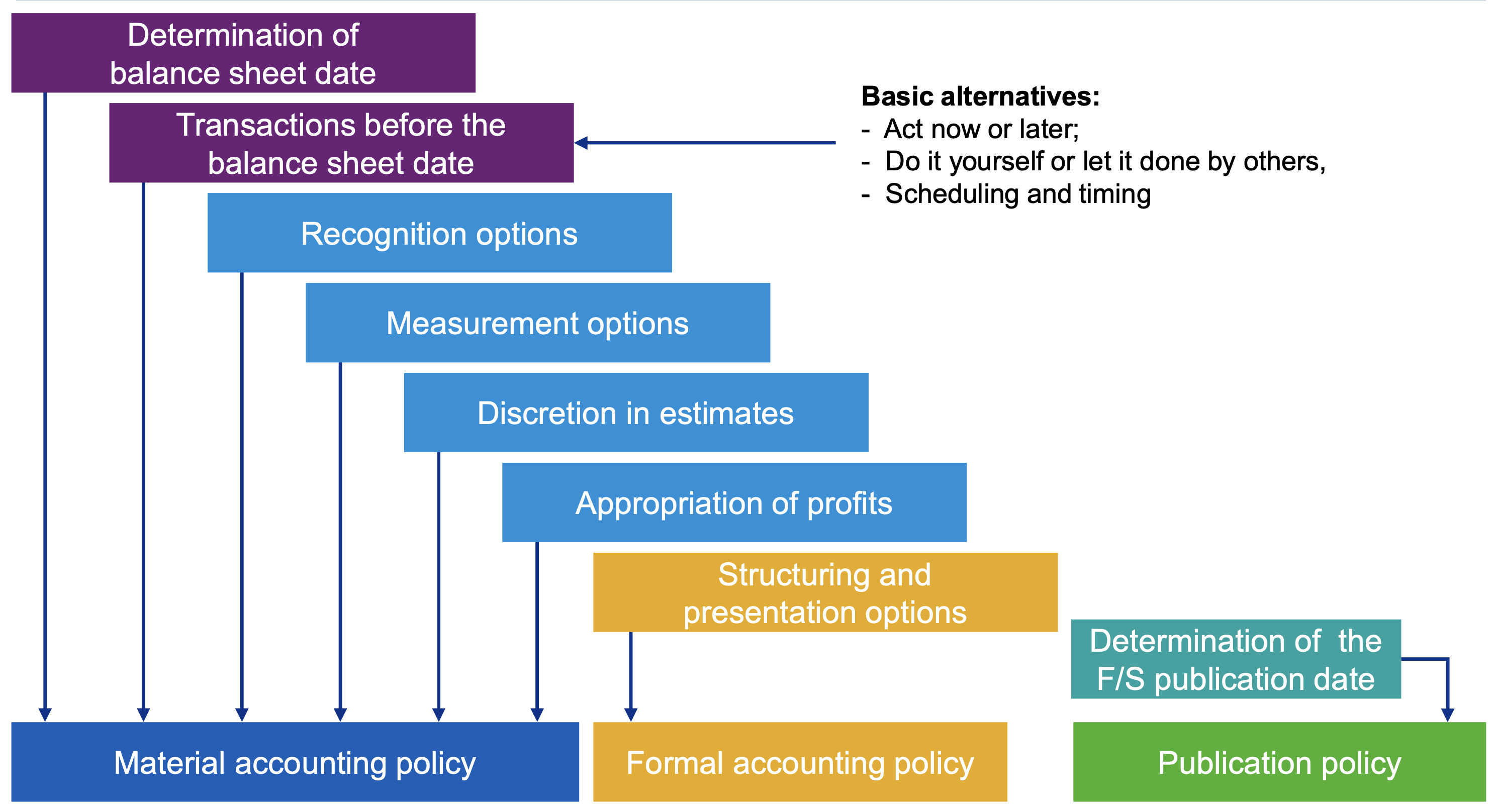

Methods to achieve earnings management are generally classified into types of accounting policy and into timing (before/after the balance sheet date).

Types of accounting policy

- Material accounting policy: Real economic decisions and accounting choices that change what is recognized and how it is measured.

- Formal accounting policy: Structuring and presentation choices that change how information is displayed without changing underlying cash flows.

- Publication policy: Timing and form of publication of financial statements and related information (earnings announcements, press releases, etc.). (p. 21)

Material Accounting Policies

These policies involve choices that directly affect the recognition, measurement, and reporting of financial transactions. It includes:

- Measures taken to influence the structure of assets and capital positions before the balance sheet date

- Recognition and valuation options given by the applicable accounting standards and the use of discretionary margins in estimates

- Appropriation of profits during the preparation of financial statements

- Time-related measures, such as setting the balance sheet date

Formal Accounting Policies

In addition to material policies, formal policies refer to using structuring and presentation options to influence stakeholders’ perceptions of the firm’s financial health.

Some instruments must be applied before the balance sheet date (ex-ante), while others can be applied after (ex-post).

Before the balance sheet date, economic facts can be designed:

- Determination of the balance sheet date

- Transactions before the balance sheet date

After the balance sheet date, economic facts can be presented differently:

- Recognition options

- Measurement options

- Discretion in estimates

Also after the balance sheet date, profits may be appropriated differently:

- Formation and dissolution of open reserves (retained earnings)

- Formation and dissolution of silent reserves

A stock-traded company may delay the publication date of their financial figures for up to a year, this may hide negative or positive developments.

Determining the Balance Sheet Date

While choosing a different balance sheet date than the fiscal year-end adds complexity to the accounting process due to having to report multiple periods, it can be used to manage earnings. For example, a company might select a balance sheet date that captures favorable financial results or avoids recognizing losses. However, there are additional reasons why a company may choose a different date:

- Financial year of the parent company: Subsidiaries often align their fiscal year with that of the parent company for consolidated reporting.

- Seasonal processes: Companies in seasonal industries (agricultural, forestry, sports) may choose a balance sheet date that reflects their typical business cycle.

- Adaption to industry: Companies may adapt to the competitive environment and align their balance sheet date with industry peers, for example audit companies or airlines.

- Use of maintenance shutdowns: Companies may record inventory and report the balance during scheduled production reductions or stops.

- Avoiding seasonal peaks: Seasonal peaks are often avoided, e.g. in Christmas industries or tax advisors.

Transactions Before the Balance Sheet Date

Companies may engage in transactions before the balance sheet date to influence their financial statements. These transactions can be asset swaps / liability swaps or balance sheet extensions / reductions, as explained in Balance Sheet Changes.

Connection to the general business cycle

In the general business cycle (market → industry → company; financing → allocation → investment → realization), the policy areas act at different stages (p. 13):

- Financing policy: Acts at the financing stage (choice and timing of equity and debt).

- Investment / procurement / production policy: Act at the investment and allocation stages (how funds are transformed into non-current assets, inventories, and work in progress).

- Sales policy: Acts at the realization stage (turning products/services into revenues and cash).

- Corporate structure policy / innovation: Shape the business model and the company’s position within market and industry, affecting all stages over time.

Possible policies include:

Financing Policy: Adjusting financing strategies, such as issuing new debt or equity, to improve balance sheet position before the reporting date.

- Timing of capital increases and scheduling of borrowing

- Determining the optimal level of indebtedness and sale of receivables (factoring)

Corporate Structure Policy: Restructuring operations or assets to present a more favorable financial position.

- Legal independence of business sectors

- Spin-off production and service sectors, outsourcing research and development activities

Innovation: Timing the launch of new products or services to coincide with the balance sheet date to boost revenues.

- Pre-/postponement of measures for the development of products as well as manufacturing and information technologies

- Decision on in-house or external development

Investment: Accelerating or delaying investment decisions to influence financial statements.

- Investment in new manufacturing/information technologies, logistical optimization of factories

- Purchase/rent/leasing/sale-and-lease-back strategies

- Date of replacement investments

Procurement Policy: Adjusting procurement strategies to manage costs and inventory levels before the balance sheet date.

- Timing of material and consumables purchases, agreements on longer payment terms

Production Policy: Adjusting production levels to manage inventory and cost of goods sold.

- Change stock targets or maintenance/repair time on production equipment

- Accelerate completion of long-term contracts

Sales Policy: Timing sales activities to influence revenue recognition.

- Acceleration of sales, offering discounts for early payments or otherwise offering special conditions

- Abandoning advertising campaigns or sales promotions

Recognition Options

Companies can choose when to recognize certain revenues or expenses, which can significantly impact reported earnings. Options are recognizing development cost, disagio (difference between nominal value and issue price of debt), or deferring tax assets.

Recognizing development costs works by capitalizing them as an asset on the balance sheet rather than expensing them immediately. This spreads the cost over several periods, improving current earnings.

Measurement Options

Measurement options involve choosing different methods to value assets and liabilities.

- For semi-finished and finished goods, administrative costs may be included or excluded from production costs, affecting inventory valuation and cost of goods sold.

- Similar inventory items can be measured using different methods to determine the acquisition cost.

- Pension discount interest rates can be influenced to affect pension liabilities.

- PPE and Intangible Assets may be measured or depreciated differently.

- Financial assets can be depreciated in a different way (reduced principle of lower value) in case of likely temporary impairment.

Causes of Depreciation

- Substance reduction: Raw material stock reduction, i.e. in mining or a gravel plant.

- Wear & tear: Physical deterioration due to usage, e.g. machinery, vehicles.

- Technical overhaul: Possibility to use new, more effective technology.

- Economic overhaul: Decreased plant revenue, declining sales, increase in operating costs.

- Expiry dates: Expiry of acquired intellectual property rights, i.e. patents, licenses, concessions.

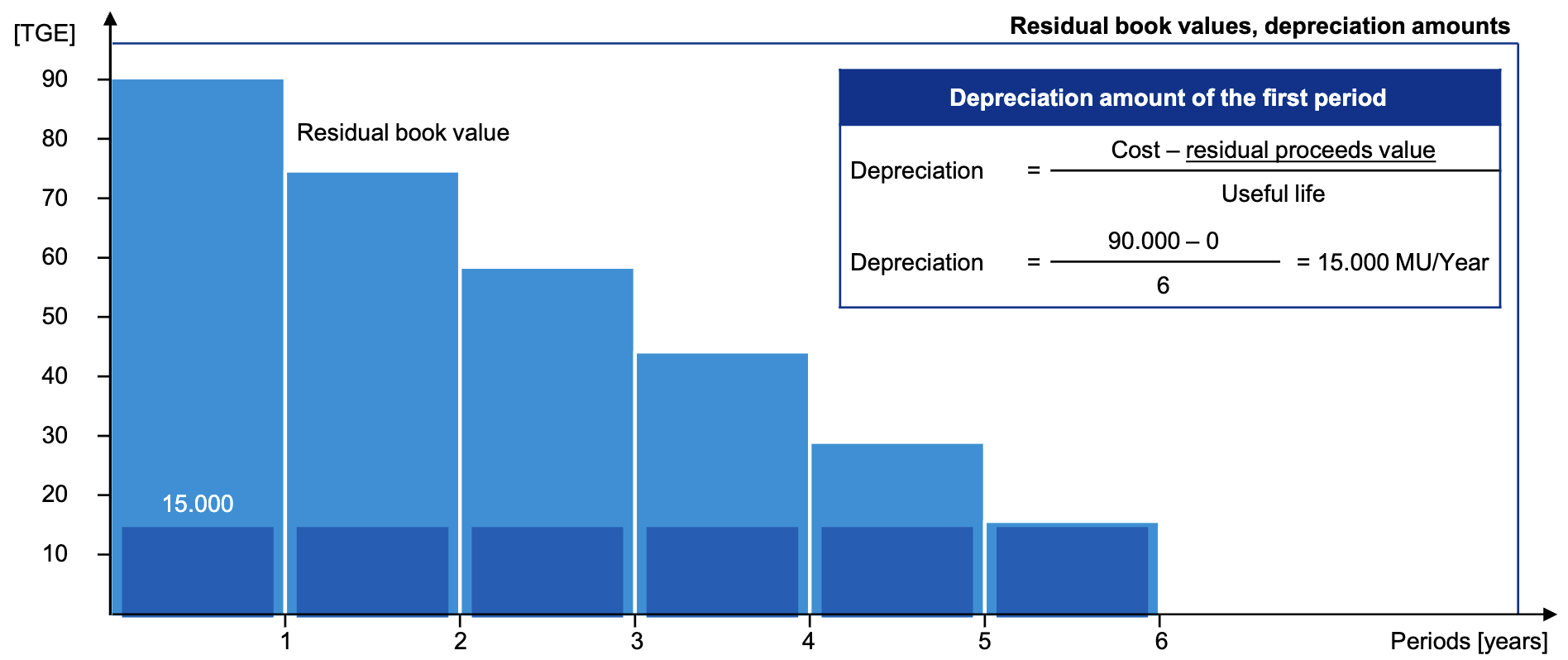

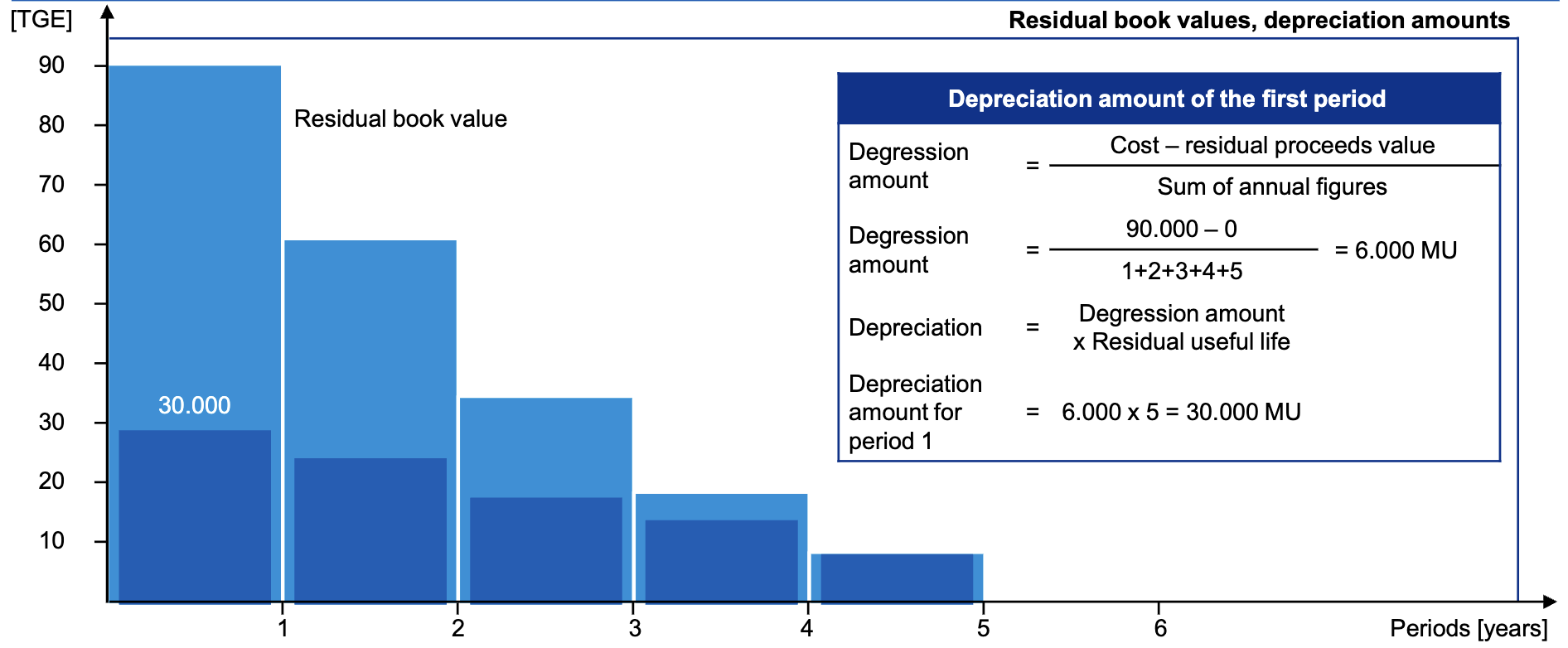

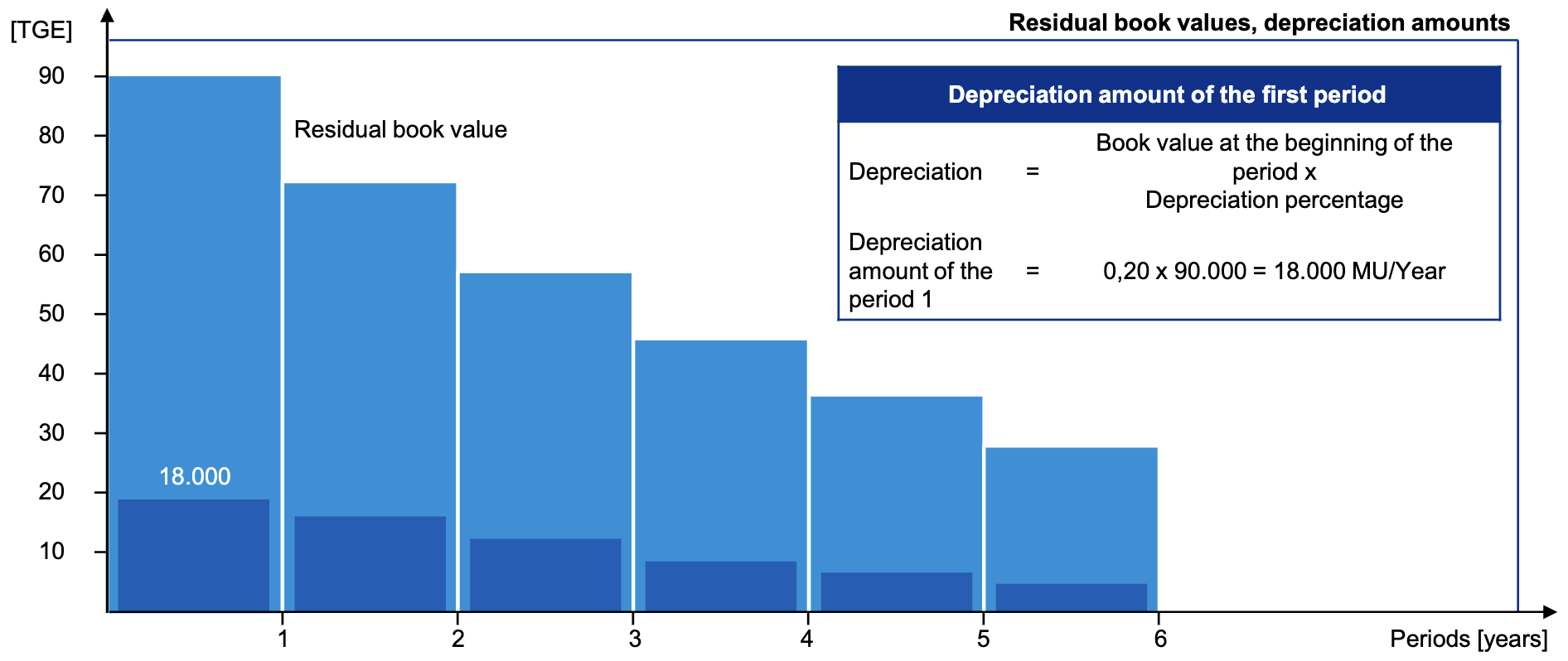

Depreciation Methods (internal)

Depreciation can be bound to performance (units of production), time, or hybrid. For time-based depreciation, there are three main methods:

| Linear | Arithmetic-Degressive | Geometric-Degressive |

|---|---|---|

| The Depreciation Percentage is chosen somewhat freely | ||

|  |  |

rsp: Residual Proceeds Value, the expected value at the end of useful life

annsum: Called Sum of Annual Figures, this is just the years summed up:

Discretion in Estimates

Estimates are used in accounting when exact values are not available. Companies can exercise discretion in these estimates to influence reported earnings. Common areas where estimates are used include:

- Provisioning: Estimating future liabilities, such as warranty costs or legal settlements, within reasonable commercial assessment.

- Scheduled depreciation: Estimating the useful life and residual value of assets.

- Reduced lower value principle for financial assets: Following this principle, depreciation is only required when a decline in value is expected to be permanent. Companies can use discretion in assessing the likelihood of recovery of asset values.

- Impairment calculations: Estimating the recoverable amount of assets to determine if impairment is necessary.

- Activation of production costs: Including appropriate overheads.

Where an Obligation is Presented

- If an obligation is virtually certain (+90%) in timing and amount, it’s presented on the statement of financial position (balance sheet) as liability.

- If its timing and amount are uncertain, but more likely than not (>50%), it’s presented in the same statement as provision.

- If it’s less likely than not (<50%), it’s disclosed in the notes only (contingent liabilities).

Types of Provisions

- Tax provisions: Expected tax payments, but uncertain in amount or timing.

- Disposal provisions: Costs for dismantling and removing assets, restoring sites (e.g. reforestation, disposal of nuclear power plants).

- Pension provisions: Obligations from occupational pension commitments to employees.

- Warranty provisions: Expected costs from warranty obligations on sold products.

- Litigation provisions: Expected costs from ongoing legal disputes.

- Other provisions: Annual audit costs, holiday/social plan obligations.

Impairments

When the remaining book value of an asset exceeds its recoverable amount, an impairment loss is recognized (p. 53). This is an unscheduled depreciation and reduces the useful life of the asset. An example is goodwill impairment, where the carrying amount of goodwill exceeds its recoverable amount, leading to a write-down.

Goodwill

Goodwill is the premium paid for unidentifiable intangible assets during a company acquisition. It represents the excess of the purchase price over the fair value of the identifiable net assets acquired. Goodwill is not amortized but is tested annually for impairment.

Goodwill on the balance sheet should be much lower than the company’s equity, because goodwill might have to be impaired at some point during bad economic times. For example, BMW has a balance of just 0.01, whereas Eon is at 1.36.

Appropriation of Profits

Earnings can be appropriated by forming or dissolving reserves, which affects reported profits, or by distributing dividends.

Profit Appropriation by Board of Management and Supervisory Board

These boards distribute a positive net result for the year through:

- Compulsory adjustments to reserves required by law

- Compulsory adjustments to statutory reserves

- Compulsory adjustments to the reserve for shares in a dominant or majority-participating company

They may then optionally settle up to 50% of what remains to retained earnings (for future managerial discretion). Appropriation of the remaining profit, including profit carried forward from previous years, is handed over to the Annual General Meeting.

Profit Appropriation by Annual General Meeting

The Annual General Meeting may appropriate profits by:

- Distributing dividends to shareholders

- Adding to existing retained earnings (as equity, managed by management)

- Profit carry forward to the next year (decided on by the AGM in the next year)

Structuring and Presentation Options

Companies can use various structuring and presentation options to influence stakeholders’ perceptions of their financial health. Different companies apply different structuring and presentation options. This includes:

- Structure of the profit/loss statement: Total Cost Method hides profit margins, Cost of Sales Method hides cost structure.

- Special netting options: Subtracting certain items from each other to present a single item.

- Company size and type dependent reliefs: Structure/presentation of the balance sheet and the profit/loss statement.

- Formation of valuation units: Underlying hedging instruments may be presented as a single item.

Netting Options

Some items may be netted against each other, i.e. presented as a single item, if allowed by law:

- Deferred taxes against tax assets/liabilities

- Received prepayments against liabilities

- Planned assets against pension liabilities

These nettings have to be disclosed in the notes.

Determination of Financial Statement Publication Date

Companies must publish their financial statements within specific timeframes after the balance sheet date, depending on whether they are stock-listed or not:

- Stock-listed companies have to publish figures every quarter, with final financial statements at the end of the fiscal year, latest 3 months after the balance sheet date.

- Other companies have to publish their figures yearly and within 12 months after the balance sheet date.

Counter Measures

To ensure earnings management stays within legal boundaries and does not mislead stakeholders, multiple agencies oversee the process:

- Supervisory Board and Audit Committee must approve the financial statements.

- Financial Auditors independently evaluate the financial statements in regards to rules and standards.

- Enforcement Bodies like the DPR/BaFin in Germany or the SEC in the US enforce laws.

- Additional corporate governance mechanisms like internal audits ensure compliance.