Resources

- Slides

- Basics of VAT, Chart of Accounts

- Learning Path Double-Entry Bookkeeping

- Recording of part 1 is not available, part 2, part 3, part 4

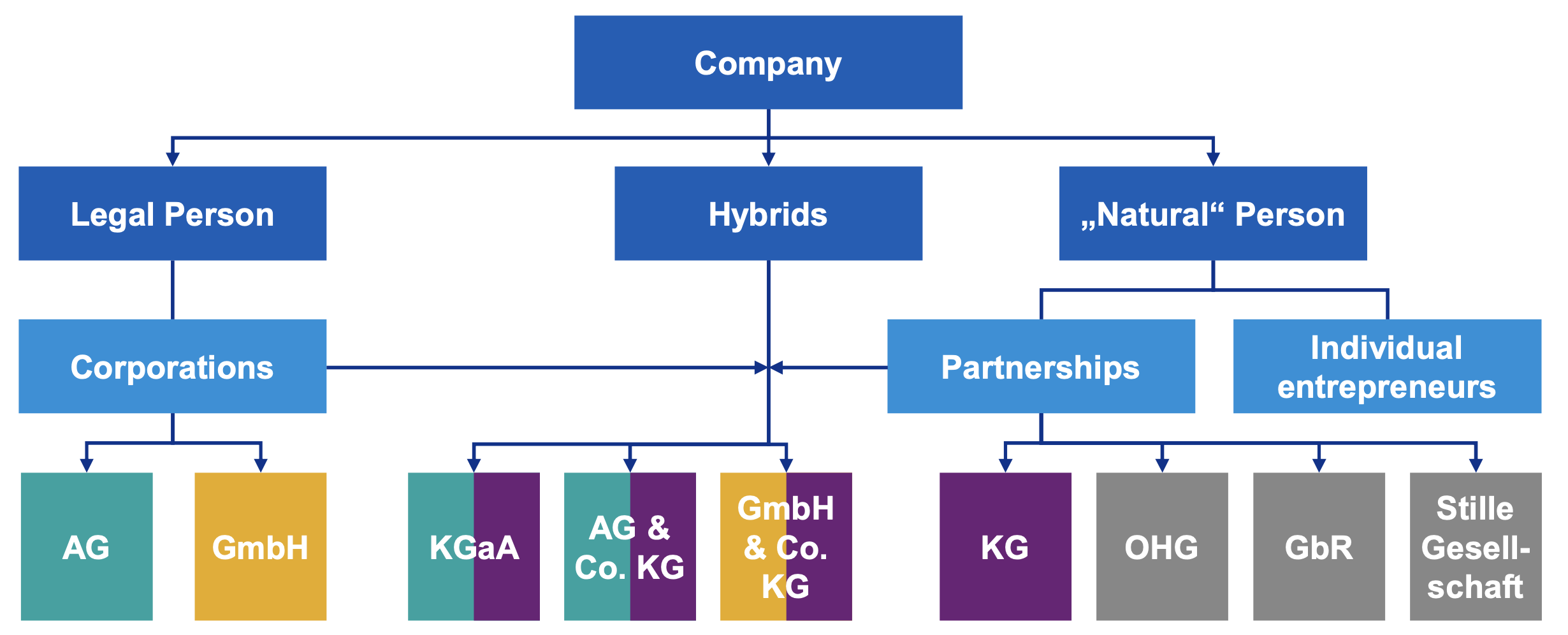

Companies and Merchants

Company Definition

While there’s no uniform definition in German law, the “company” is differentiated as:

- Functional Term: A company exists if a legal or natural person is entrepreneurially planning and operating.

- Institutional Term: The Company requires a commercial activity in the economy and a minimum level of institutional means.

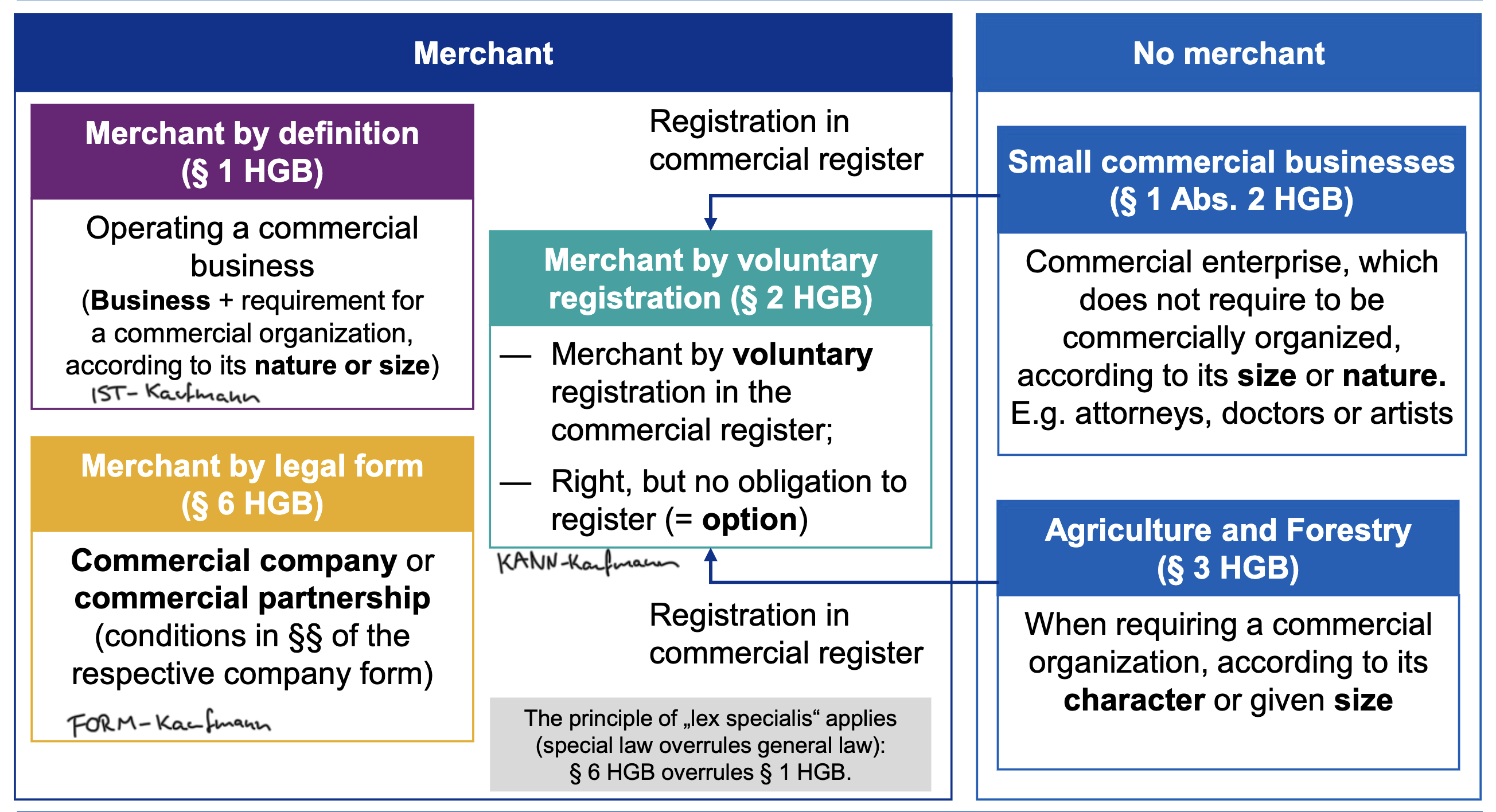

Merchant Definition

A merchant is someone who operates a commercial business. According to HGB §§1–3, merchants are classified as:

- Merchant by Definition (§1 HGB): Anyone who operates a commercial business as defined by law, requires a commercial organization according to its nature or size.

- Merchant by Registration (§2 HGB): Anyone who voluntarily registers their business in the commercial register.

- Merchant by Legal Form (§3 HGB): Certain legal entities (e.g., AG, GmbH) are considered merchants.

A registered merchant is obliged to follow all regulations of the HGB, including bookkeeping and retaining business correspondence, while unregistered merchants have limited obligations. Individual merchants with ≤80k€ net profit and ≤800k€ revenues are exempt from the bookkeeping rules of §§238-241 HGB and can use the net income method (profit = operating income - operating expenses) according to §4 sec. 3 EStG.

Forms of Capital

Apart from equity capital, provided by owners, companies can also be financed through debt capital, borrowed from third parties.

- Equity Capital: Personal contributions, retained earnings, reserves. No repayment obligation, but owners expect returns (dividends, profit shares).

- Debt Capital: Loans, bonds, credit lines, leasing, supplier credit. Must usually be repaid with interest, creating fixed obligations for the company.

- Special forms include crowdfunding, grants, and venture capital.

Bookkeeping Basics

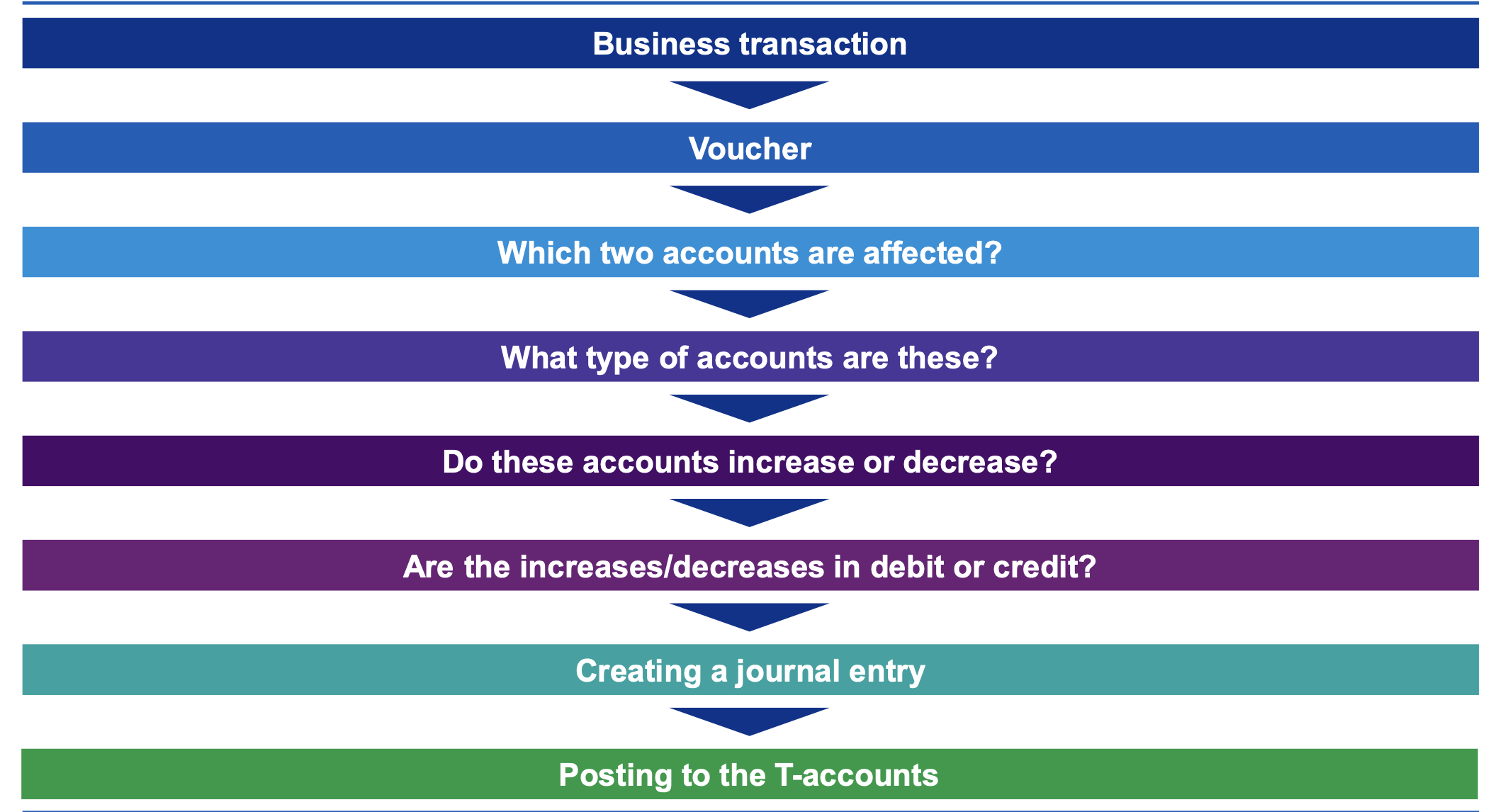

Vouchers: Posting Documents

Every transaction must be backed by a document, called voucher. There are to types:

External Documents: Received from a third party (e.g., incoming invoices, receipts, contracts), usually includes date, amount, parties involved, description of transaction.

Internal Documents: Created within the organization, e.g. outgoing invoices, payroll records, credit notes, material withdrawal slips.

Net and Gross Amounts

Net is the amount before taxes, gross includes taxes. In bookkeeping, transactions are recorded in net amounts, with taxes accounted for separately.

Recording a Transaction

To ensure auditors, tax authorities and managers can trace the origin and flow of financial movements, every transaction must follow a specific sequence in chronological and factual (type of transaction) order. The structure of journal and ledgers ensures meeting legal/regulatory requirements, informed decisions, a clear audit trail, and prepares for financial statements.

First, the transaction is recorded in the journal (book of original entry). Then, it is posted to the respective ledgers (books of final entry).

Journal

The journal is the primary book of entry, recording all financial transactions in chronological order. It includes

Opening Entries: Initial balances when starting bookkeeping, from previous period.

Ongoing Daily Transactions: Regular business activities; purchases, sales, payments, receipts, etc.

Pre-Closing Entries: Adjustments before closing the books, e.g. depreciation or accruals.

Closing Entries: Final adjustments to prepare financial statements.

Each entry must include date, voucher type and number, brief description, amounts debited and credited, references to accounts involved.

Ledgers

Ledgers are specialized books that categorize and summarize transactions recorded in the journal. The main types of ledgers are:

- General Ledger: As main accounting record, this summarizes all the financial transactions of a company. Organized by accounts like cash, inventory, receivables, payables, equity, revenue, expenses.

- Subsidiary Ledgers provide more detailed records for specific amounts and may include an Accounts Receivable Ledger (customer balances), an Inventory Ledger (detailed inventory records), and an Accounts Payable Ledger (supplier balances).

The ledgers are interconnected, with the general ledger providing a summary of all accounts, while subsidiary ledgers offer detailed insights into specific areas.

Journal Entry Syntax

Debit (account) / Credit (account) Amount

Means: Debit the first account and credit the second account with the specified amount.

Example: Buying material for 1000 cash: Material / Cash 1000; selling on credit: Accounts Receivable / Sales Revenue 1000

Account Structure

Companies use a standardized account assignment system to record transactions in a logical and parseable way. The accounting framework defines how accounts are structured and categorized.

Accounts are typically organized in four layers:

- Account Class: Highest level, grouping similar types of accounts (e.g. fixed assets, income)

- Account Group: Subdivisions within classes (e.g. land, buildings)

- Account Type: Further breakdown (e.g. undeveloped land)

- Individual Account: Specific account (e.g. specific plot)

In Germany, there are two main accounting frameworks:

- Industrial Account Framework: Common in manufacturing and industrial sectors and organized along HGB. Divides accounts by balance sheet structure: Assets, Liabilities, Income, Expenses, etc.

- Community Account Framework: Organized by process classification and more suited for companies focusing on internal processes. Categories include Investment, Financial Accounts, Materials, Stocks, etc.

Types of Accounting Systems

Cameralistic Accounting

Typically used by public institutions/governments, focuses only on recording receipts and expenditures (money in, money out).

It does not track assets, liabilities, or equity, and is primarily concerned with budget compliance and cash flow management, and therefore does not provide a clear picture of the company’s assets of profitability.

Simple Commercial Accounting

Used by small businesses with limited transactions, it records only cash inflows and outflows without tracking accounts receivable/payable or inventory.

There’s no proper income statement and profits can only be estimated by the net assets change over time through inventories.

Double-Entry Bookkeeping

Required for most companies, this system records each transaction in two accounts: a debit in one account and a credit in another. It links all transactions to the income statement and balance sheet, providing cash flow, assets, liabilities, income, and expenses.

This allows for accurate calculations of financial health, ensure that all transactions are recorded consistently, helps prepare financial statements, makes it easier to compare across companies, and supports both management and legal needs.

Double-Entry Bookkeeping

In DEB, debited amounts of a transaction must always equal credited amounts. This ensures the accounting equation stays balanced: .

Assets are debited when they increase, credited when they decrease. Liabilities and equity are credited when they increase, debited when they decrease.

Posting Records

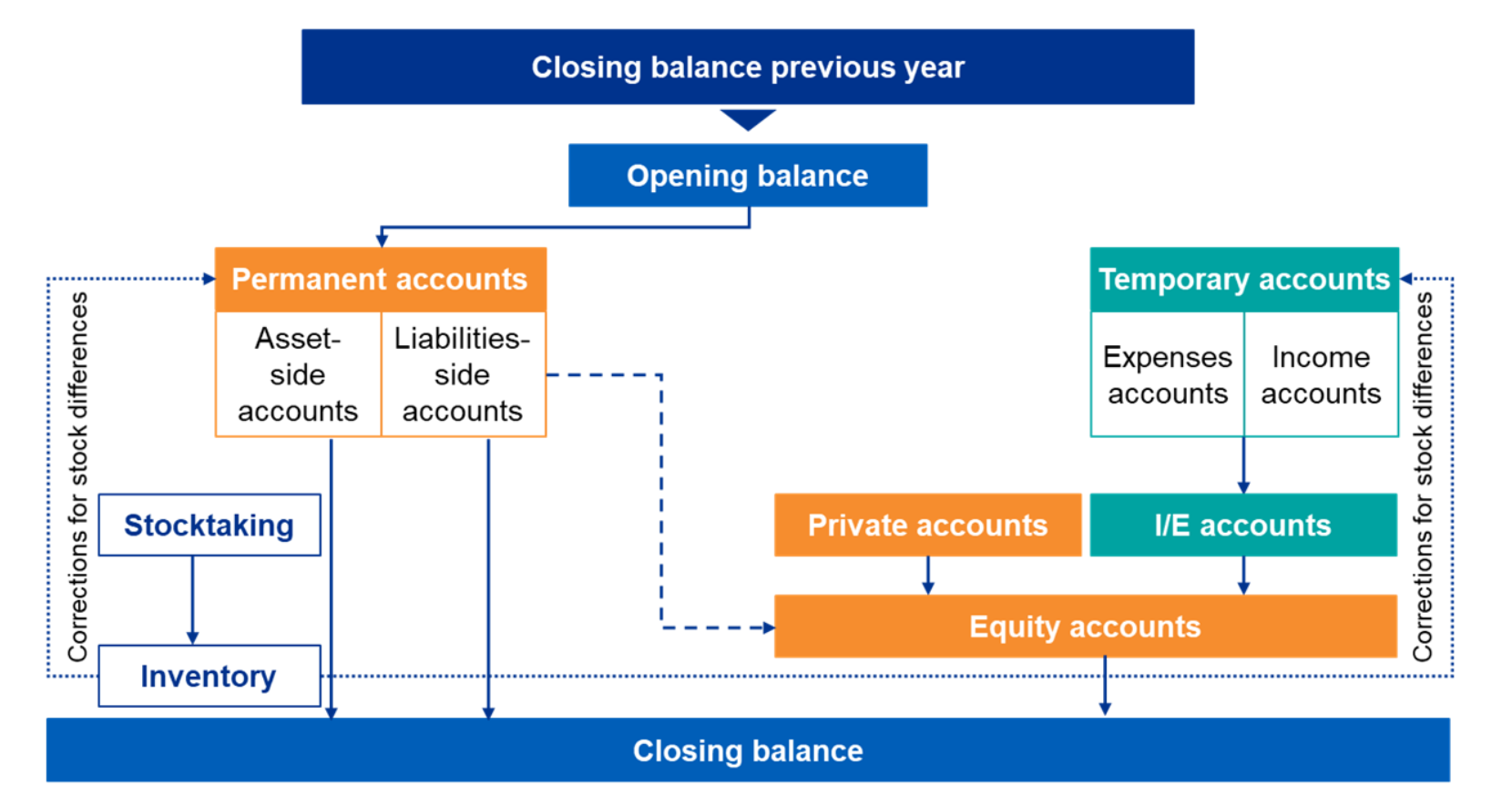

Each transaction is recorded in a single posting record or a composite posting record (multiple transactions at once). When permanent accounts are updated at the end of the financial year, the the postings for each account are summed up and added to the previous opening balance.

The clearing ban prohibits netting income and expenses (i.e. rent income and expense).

Accounts

Transactions are recorded in permanent (balance sheet) accounts and temporary (income statement) accounts.

- Permanent Accounts: Reflect stock values (assets, liabilities, equity) at a specific point in time. Their balances carry over to the next period.

- Temporary Accounts: Reflect flow values (income like sales or interest, expenses like wages or depreciation) over a period. Their balances are closed to equity (net profit/loss) at the end of the period.

Special accounts are used for periodization:

- Profit & Loss Account: A sub-account of equity to record all income-affecting transactions, both revenues and expenses. Once the period ends, the balance is transferred to equity.

- Result of the Period: Determined by the net of all transactions.

An additional Capital Account is used to visualize deposits and withdrawals by owners.

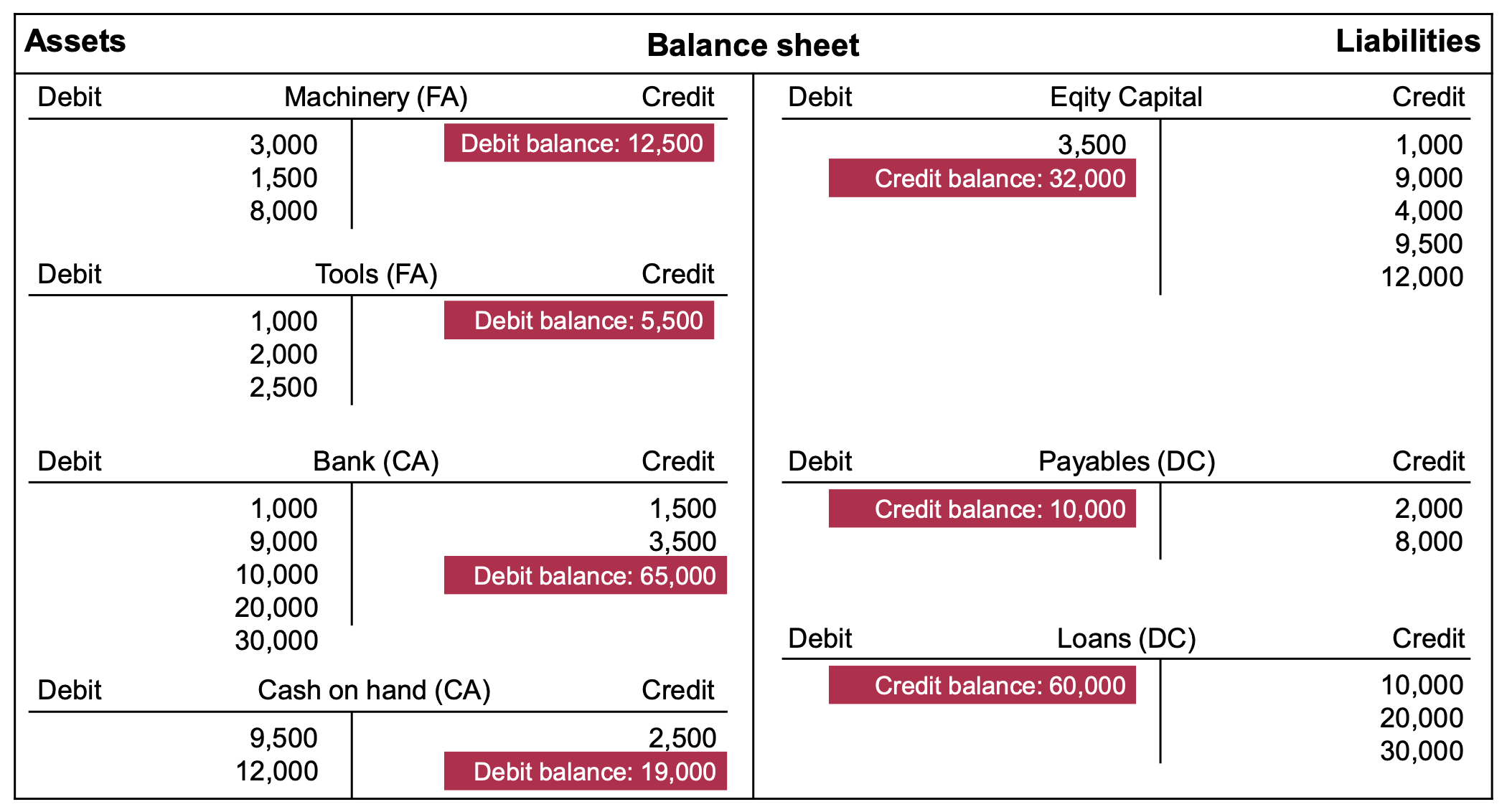

T-Accounts

A T-Account is a visual representation containing the opening balance (OB) and additions on one side, and the reductions and closing balance (CB) on the other side. It helps to understand how debits and credits affect account balances.

An example is the balance sheet: debit-side (assets) left, credit-side (liabilities) right; however other accounts can also be visualized as T-Account.

Closing Accounts

When closing a temporary account, the debit balance (positive when debit>credit on debit side) is credited to the credit side of an interim or non-temporary account, or the credit balance (positive when credit>debit on credit side) is debited to the debit side, resulting in a zero balance

The calculated balance is not part of the T-Account, but is noted separately.

When reopening permanent (balance sheet) accounts in the next period, the transfer is reversed to restore the opening balance as the previous debit/credit balance. Equity subaccounts start at 0 as they have been closed to equity.

Chart of Accounts

A systematic register of accounts for bookkeeping for certain industries. Accounts are structured hierarchically into classes, groups, and accounts.

Examples: page=74

- Common chart of accounts: Classes 0-9; follows process organizational principle; sequence of accounts corresponds to business processes.

- Industrial chart of accounts: Classes 0-9; follows balance sheet and income statement; dual purpose for financial/external accounting and cost/internal accounting.

Equity

Equity represents the owner’s claim on the company’s assets after liabilities. Changes in equity are a result of the statement of profit or loss, other comprehensive income, or transactions with shareholders (e.g. increase in share capital, dividends) or restatements (due to errors or changes).

Companies can finance themselves though equity:

- Internal Financing: Retained profits not paid out but reinvested

- Equity Financing: New capital brought in though issuing shares or attracting new shareholders

Under HGB, equity is broken down into:

- Subscribed Capital: The amount officially committed to be contributed by shareholders, must be shown in the balance sheet. A GmbH requires at least 25K€, AG 50K€

- Capital Reserves: Money from additional payments over the nominal value of shares (e.g. contributions for special rights) or converting bonds into shares.

Additionally, Retained Earnings are profits kept in the company rather than distributed as dividends. Under German law, these are divided into:

- Legally Required Reserves: E.g. mandatory 5% of annual profit for AGs

- Statutory Reserves: Set aside based on company statutes

- Other: More flexible leftover profit, can be used for reinvestment, dividends, or discretionary reserves.

In contrast to these Open Reserves (clearly identified in balance sheet), there are also Hidden Reserves, arising from undervalued assets or overvalued liabilities. These are not explicitly shown but can provide a financial buffer.

In contrast to HGB, IFRS introduces a statement of Other Comprehensive Income (OCS), which allows for equity changes without impacting profit or losses.

Equity sub-accounts include private accounts (withdrawals, investments), capital accounts (shareholder contributions), and income/expense accounts.

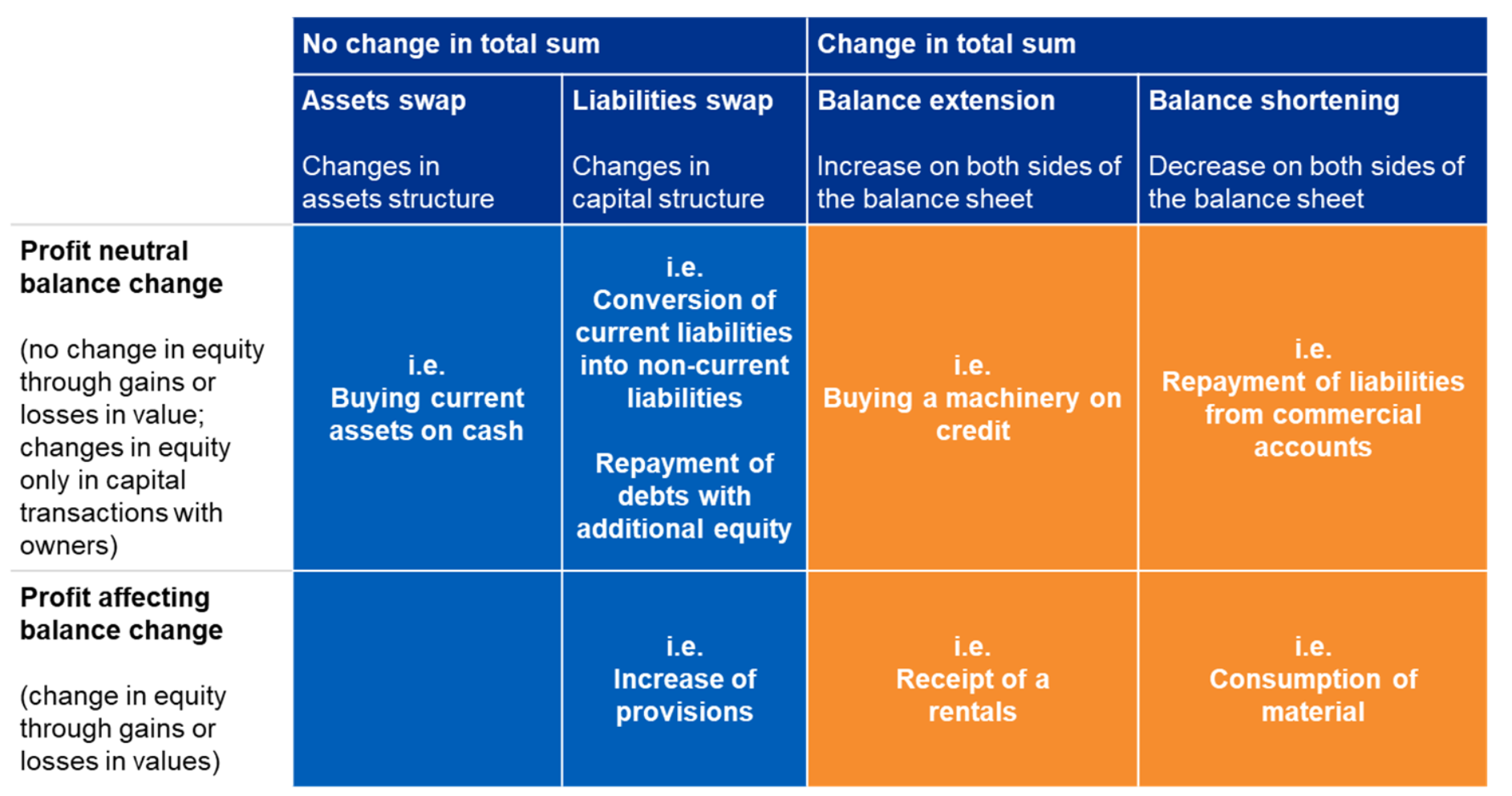

Balance Sheet Changes

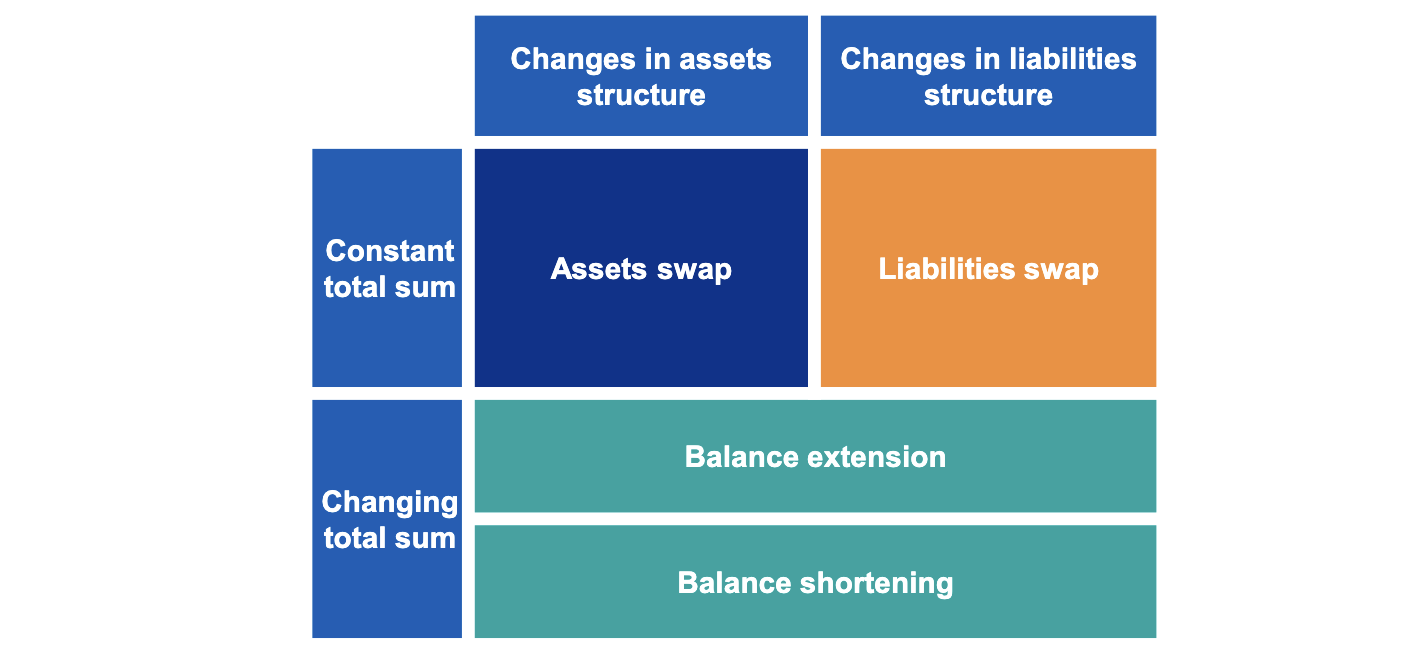

There are 4 types of balance sheet changes:

- Assets Swap (constant total sum): One asset increases while another decreases by the same amount (e.g. buying materials with cash).

- Liabilities Swap (constant total sum): One liability increases while another decreases by the same amount (e.g. debt restructuring).

- Balance Extension (total sum increases): Assets and a liabilities both increase (e.g. purchasing material on credit).

- Balance Shortening (total sum decreases): Asset and a liabilities both decrease (e.g. repaying debt with cash).

A hybrid transaction can be split up into a part that impacts profit and one that does not.

These changes may be profit-neutral when equity is not affected or profit-affecting when equity changes.

Adjusting Journal Entries

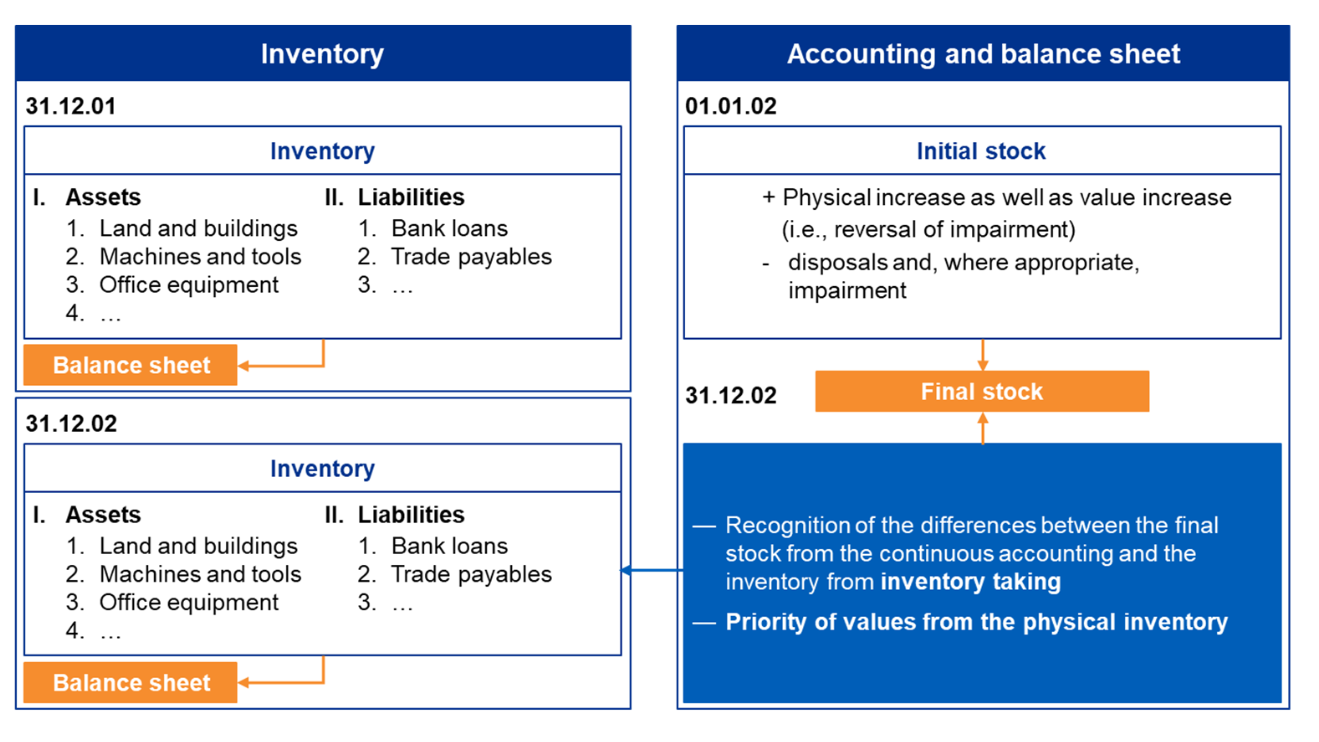

Inventory

Inventory is everything a business owns (assets) and owes (liabilities) on a specific date. Every year, businesses must create this inventory list based on the result of physical inventory taking.

Assets are sorted by liquidity:

- Non-Current Assets: Long-term, not easily converted to cash (e.g., property, equipment).

- Current Assets: Short-term, easily converted to cash (e.g., inventory, receivables, cash).

Liabilities are split into:

- Equity (net assets): Owner’s claims on assets after liabilities.

- Debt Capital: Obligations to third parties, split into long-term and short-term.

If , the company has positive equity (net worth). If , the company has negative equity, which can indicate financial distress.

More in Inventories.

Stocktaking

Inventory taking is a key step in accounting, ensuring accurate financial records. This can mean full physical stocktaking or simplified methods and aims at accurately tracking, valuing and categorizing what the company owns.

- Physical Inventory: Counting/weighing/measuring actual items like machines, tools, materials, …

- Book Inventory: Record untouchable things, e.g. debts, loans, intangible rights, documents, …

This process is mandatory for merchants.

Simplified Inventory Procedures

Full physical stocktaking is time-consuming, so companies often use simplified methods:

- Extended Cut-Off Stocktaking: Counting items in regular intervals, extrapolating to year-end.

- Pre-/Post-Dated Stocktaking: Counting within 2 months before/after reporting date, adjusting for known changes, with different types of assets potentially counted at different times.

- Permanent Stocktaking: Ongoing tracking of inventory through regular updates, suitable for high-value or fast-moving items, but must be verified physically at least yearly.

- Sampling with Statistical Methods: Using statistical sampling to estimate total inventory value, reducing the need for full counts. Includes Estimate of Differences, Ratio Estimate, Regression Estimation, but is only allowed if the result is as accurate as a full inventory.

Simplified Valuation Methods

To reduce effort, companies can use simplified valuation methods for inventory:

- Fixed Value Procedure: Used for items like tools, materials, office supplies, that are regularly replaced, low in total value, and stable in quantity and composition. A fixed value is set based on historical data and adjusted for inflation, while a physical inventory is only done every 3 years.

- Group Value Procedure: Used for similar assets, which are grouped and valued as one, based on average cost.

Depreciation

Depreciation represents the loss in value due to wear and tear of fixed assets over time. It allocates the cost of an asset over its useful life, reflecting its declining value due to usage, obsolescence, or age. Depreciation is generally based on (fiscal) depreciation tables, however some managerial discretion is involved.

Value Adjustment

Value adjustments are used to reflect changes in the value of assets or liabilities on the balance sheet. They can be either impairments (reductions in value) or revaluations (increases in value). This is based on buy/sell market prices (fair value).

A write-down can be an impairment. It’s a permanent reduction in the book value of an asset when its recoverable amount falls below its carrying amount. This is recognized as an expense in the income statement.

Deferred Income & Charges

Deferred income and charges are used to allocate revenues and expenses to the correct accounting periods, ensuring that financial statements accurately reflect the company’s financial performance.

Examples:

- Paying the January rent in December is a deferred expense, recognized in January when the service is used.

- A company receives payment in advance for services to be provided over several months. The payment is recorded as deferred income and recognized as revenue over the service period.

When there is no cash flow, these are recorded as other liabilities or other assets. For example when interest accrues but is not yet paid.

Provisions

Provisions are liabilities of uncertain timing or amount, set aside to cover future obligations. They are recognized when a present obligation exists, it is probable that an outflow of resources will be required, and the amount can be reliably estimated. These have to be recorded following the imparity principle.

More in Provisions.