Consolidated vs. Annual Financial Statements

- Annual Financial Statements: Pertain to a single legal entity.

- Consolidated Financial Statements: Combine the financials of a parent company and its subsidiaries into a single economic entity (a “group”). Capital-market oriented companies in Germany must prepare IFRS consolidated financial statements.

Overview

The mandatory IFRS components are:

- Statement Of Financial Position: A snapshot of assets, liabilities, and equity at a point in time.

- Statement Of Profit Or Loss: Reports financial performance over a period.

- Statement Of Other Comprehensive Income: An addition to the statement of profit or loss where certain income and expenses are recorded that bypass profit or loss but affect equity.

- Statement of Cash Flows: Shows cash movements from operating, investing, and financing activities.

- Statement of Changes in Equity: Details changes in the owners’ stake in the company.

- Notes To The Financial Statements: Provide crucial context, accounting policies, and detailed breakdowns of the figures in the statements.

Additional reports often include:

- Management Report: Provides management’s perspective on performance, strategy, risks, and future outlook.

- Auditor’s Report: Offers an independent opinion on the fairness and accuracy of the financial statements.

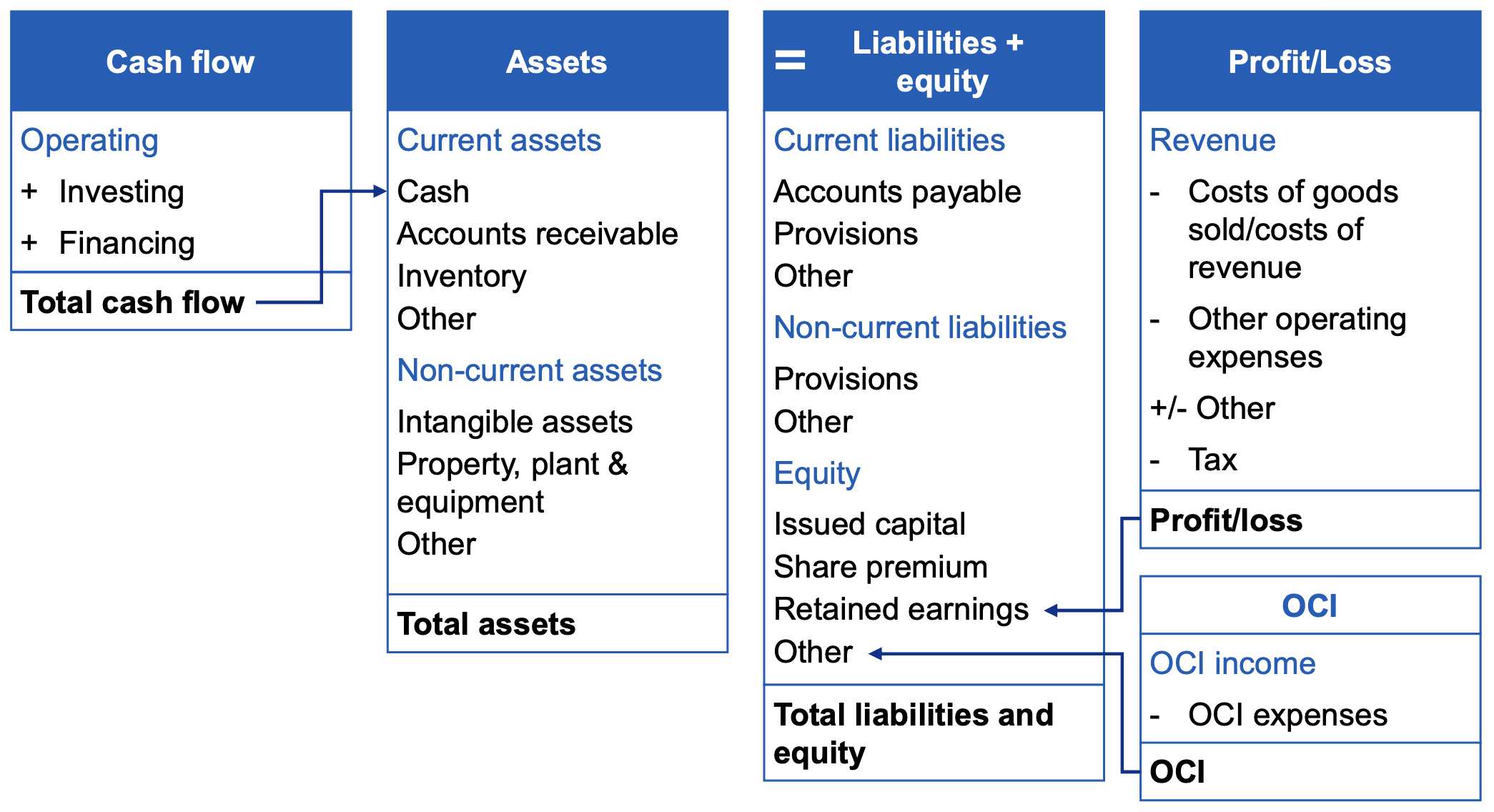

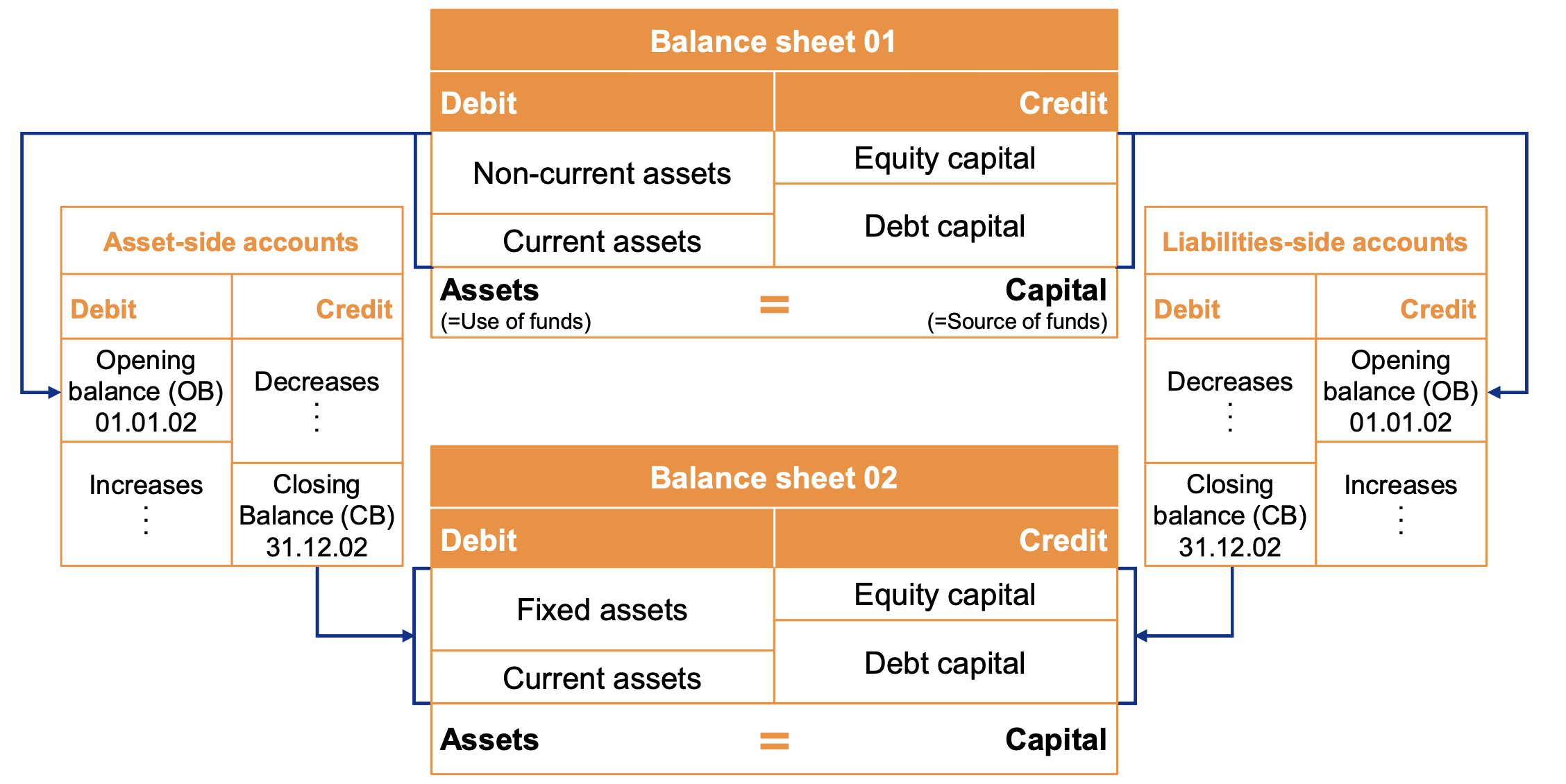

Statement Of Financial Position

Also called Balance Sheet

Purpose: Provides a snapshot of the company’s financial position at a specific point in time.

Bottom line: Total equity and liabilities

This document is prepared for a specific point in time – often 31.12.

The statement represents the accounting equation (Assets = Liabilities + Equity):

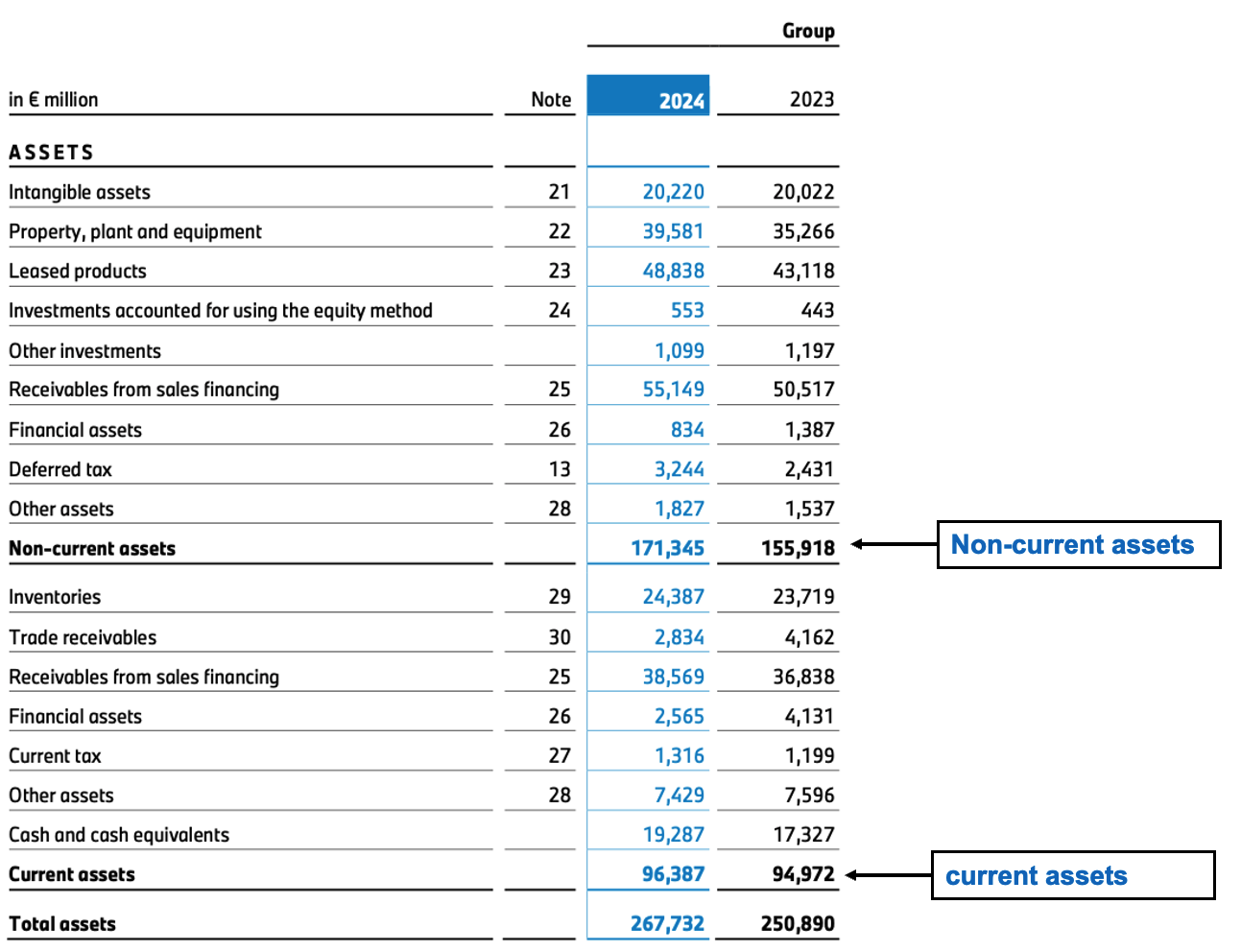

- Assets: Resources owned by the company (e.g., cash, inventory, property)

- Current Assets: Short-term resources (e.g., cash, inventory)

- Non-current Assets: Long-term resources (e.g., property, plant, equipment)

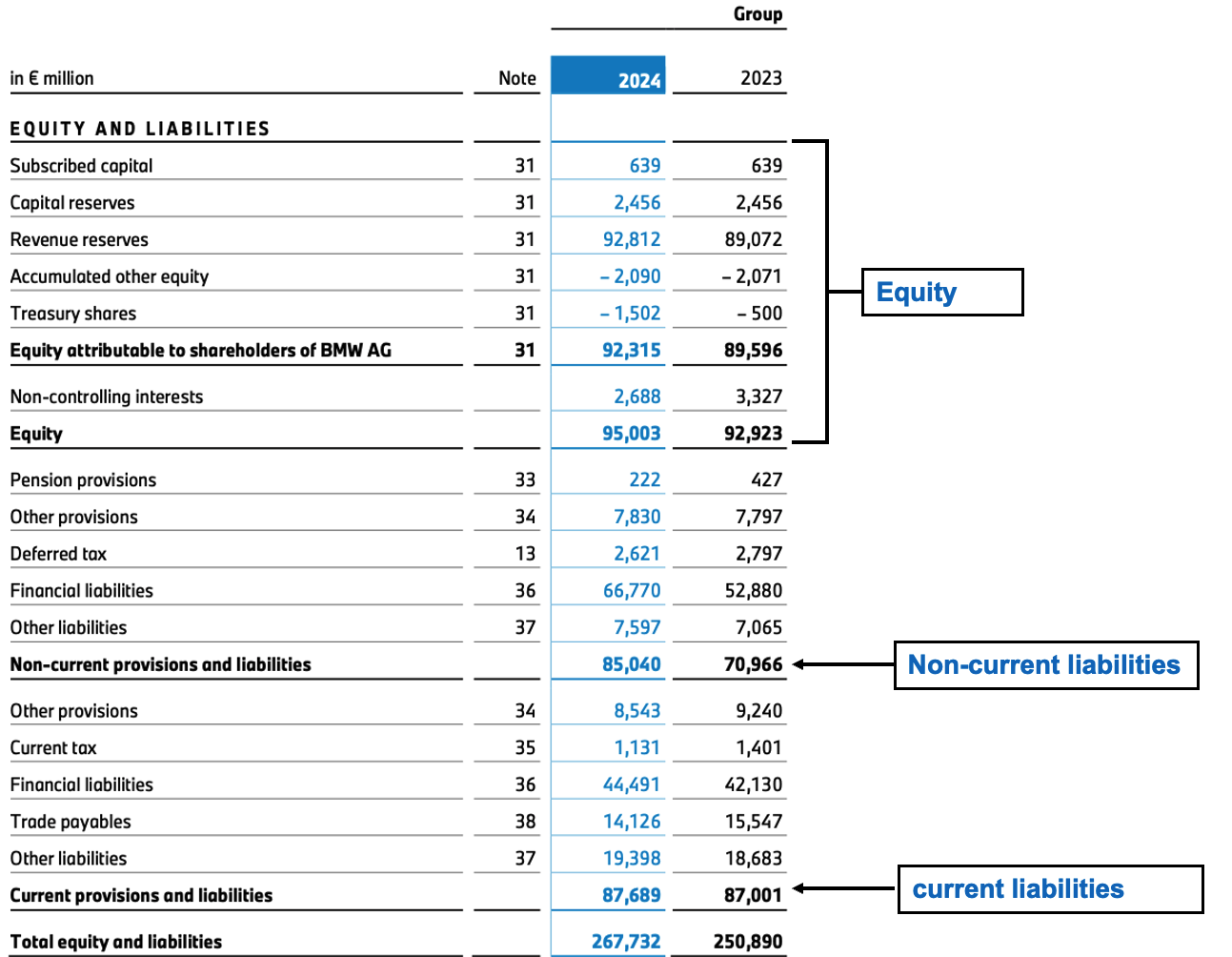

- Liabilities: Obligations owed to outsiders (e.g., loans, accounts payable)

- Current Liabilities: Short-term obligations (e.g., accounts payable)

- Non-current Liabilities: Long-term obligations (e.g., bonds payable)

- Equity: Owner’s residual interest in the company (e.g., share capital, retained earnings)

Resources and investments are on the left assets side, financing is on the right side (liabilities and equity).

German GAAP Difference

In German GAAP, the balance sheet format is more rigid, with specific line items and order. IFRS allows more flexibility in presentation and classification.

Assets Definition

Based on the IFRS Conceptual Framework, assets are rights that have the potential to produce economic benefits for the entity. They are controlled by the entity as a result of past events. This may be a right to use a physical object or the right to receive money or other benefits, or even preventing cash-outflow in the future.

Typical Assets

- Property, plant, and equipment (PPE) → fixed assets

- Intangible assets (patents, licenses, goodwill)

- Financial assets (long‑term investments)

- Inventories (raw materials, work‑in‑progress, finished goods)

- Accounts receivable

- Marketable securities

- Cash and cash equivalents

Typical Owner’s Equity

- Share capital / common stock

- Capital reserves / capital surplus

- Retained earnings

- Profit or loss carried forward

- Net income for the period (until it is closed into retained earnings)

Typical Liabilities

- Pension reserves and other provisions

- Overdraft loans and other short‑term bank debt

- Long‑term financial debt (bonds, bank loans)

- Accounts payable (suppliers, etc.)

- Accrued liabilities (e.g. wages, interest, taxes due)

The statement of financial position may be prepared before or after the appropriation of earnings.

- Before Appropriation: Equity is split into net earnings, and earnings carried forward.

- After Appropriation: Unappropriated profit is the result of net earnings plus earnings carried forward, adjusting for withdrawals or allocations to capital, subtracting transfers to reserves. This figure shows the remaining profit available for distribution to shareholders or future retention.

|  |

|---|

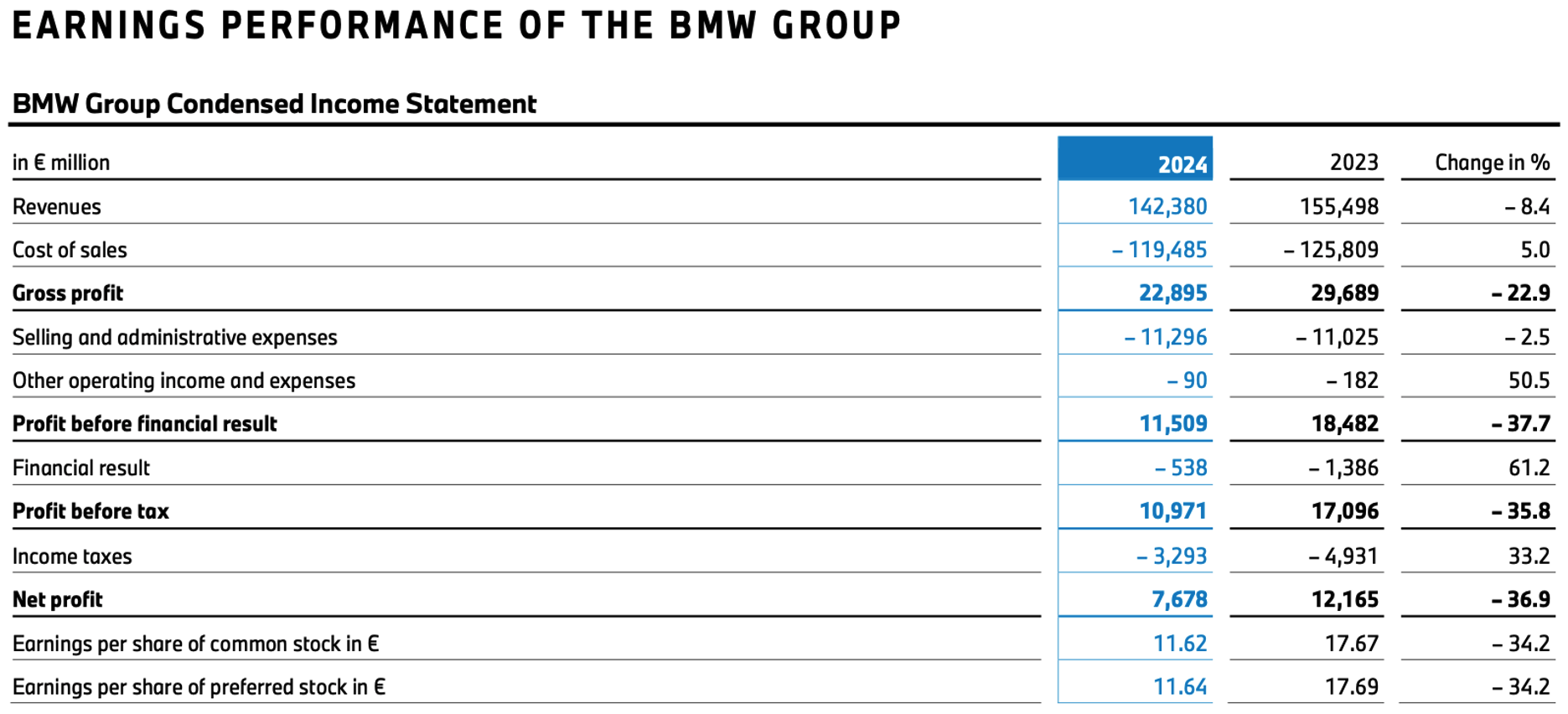

Statement Of Profit Or Loss

Also called Income Statement or P&L Statement

Purpose: Shows the company’s financial performance over a specific period (e.g., quarter, year).

Bottom line: Net profit/loss after tax

Typical Income Statement Items

- Sales revenue / sales income

- Material expenses / cost of goods sold (COGS)

- Wages and salaries, personnel costs

- Depreciation and amortization

- Interest expenses and interest income

- Income taxes

- Extraordinary income/expenses

Income Statement Presentation Variations

Different companies may present their income statements in various formats, with different ratios being used for analysis. No matter the method used, the result is calculated in a similar order: Operating Result (EBIT), Financial Result, EBT, and finally Net Income/Loss.

Two common methods:

- Total Cost Method: The company’s total performance during the period is shown, including changes in inventories and capitalized own services

- Cost of Sales Method: Revenues are compared with the production costs of the products or services sold during the financial year

Total Cost Method

Revenues are compared with the total costs incurred during the financial year, including changes in inventories and capitalized own services.

Costs are presented by nature (e.g., raw materials, personnel expenses, depreciation), obscuring the gross profit.Predominating method in Germany.

- Changes in the stock of finished and unfinished goods

- Capitalized own services

- Operating expenses (materials, personnel, depreciation)

Structure:

Revenues

- Changes in Stock & Capitalized Own Services

= Operating Performance not gross profit

- Material Expenses

- Personnel Expenses

- Deprecation & Amortization

+ Other Operating Income

- Other Operating Expenses

= Operating Result (EBIT in a broader sense)This method classifies costs by their type:

- Personnel costs (wages, salaries),

- Material costs (raw materials, supplies),

- Depreciation (value loss of machines, furniture, etc.),

- And other general operating expenses.

It also includes changes in stock levels and internally generated services (e.g., software development for internal use), which can increase the revenue side. For example, if a company produces goods that are not yet sold but stay in inventory, these are still considered a value created during the year and are reflected in the income statement.

Cost of Sales Method

Revenues are compared with the production costs of the products or services sold during the financial year.

Costs are presented by function (e.g., cost of sales, selling expenses, administrative expenses), obscuring the material expense ratio.Predominating method globally.

- Production cost of services sold

- Selling/distribution cost

- Administrative cost

Structure:

Revenues

- Cost of Sales

= Gross profit

- Selling & Distribution Expenses

- Administrative Expenses

- Research Expenses

+ Other Operating Income

- Other Operating Expenses

= Operating Result (EBIT in a broader sense)This method is more aligned with how products are sold. Instead of classifying costs by type, it breaks them down based on functions:

- Production costs (i.e., what it costs to make the product),

- Selling expenses (e.g., advertising or distribution expenses),

- Administrative expenses (e.g., office costs, accounting staff).

Only the costs directly related to what was actually sold during the year are included. So, inventory that wasn’t sold doesn’t get accounted yet.

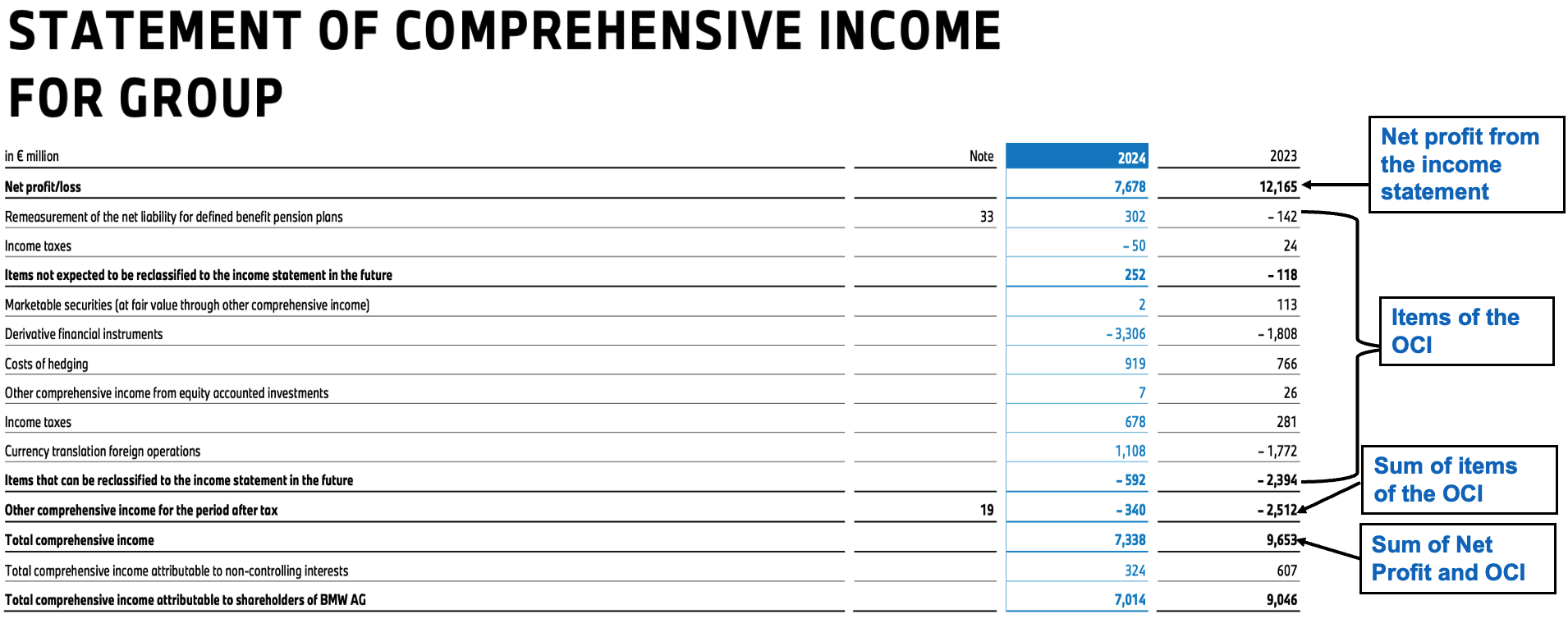

Statement of Other Comprehensive Income

Purpose: Records income/expense items not recognized in the profit/loss statement, but affecting equity.

It presents income/expenses in the group and changes in equity that are not the result of the transactions with owners. This could include:

- Unrealized gains or losses on available-for-sale financial assets

- Foreign currency translation differences

- Gains/Losses on derivate instrument designated as cash flow hedges

This table splits the income statement into two parts:

- Items not expected to be reclassified to profit or loss (e.g., revaluation of property, plant, and equipment)

- Items that may be reclassified to profit or loss (e.g., foreign currency translation differences)

Unfortunately, there is no consistent concept (yet) for differentiating between items that are included in or excluded from the profit or loss statement. Instead, the OCI spans a wide range of accounting topics and can be useful for earnings management, as it receives less attention than the income statement.

German GAAP Difference

In German GAAP, Other Comprehensive Income does not exist. Instead, all income and expenses are recognized in the profit or loss statement.

Typical Other Comprehensive Income Items

- Revaluation of property, plant, and equipment

- Foreign currency translation differences

- Gains/losses on cash flow hedges

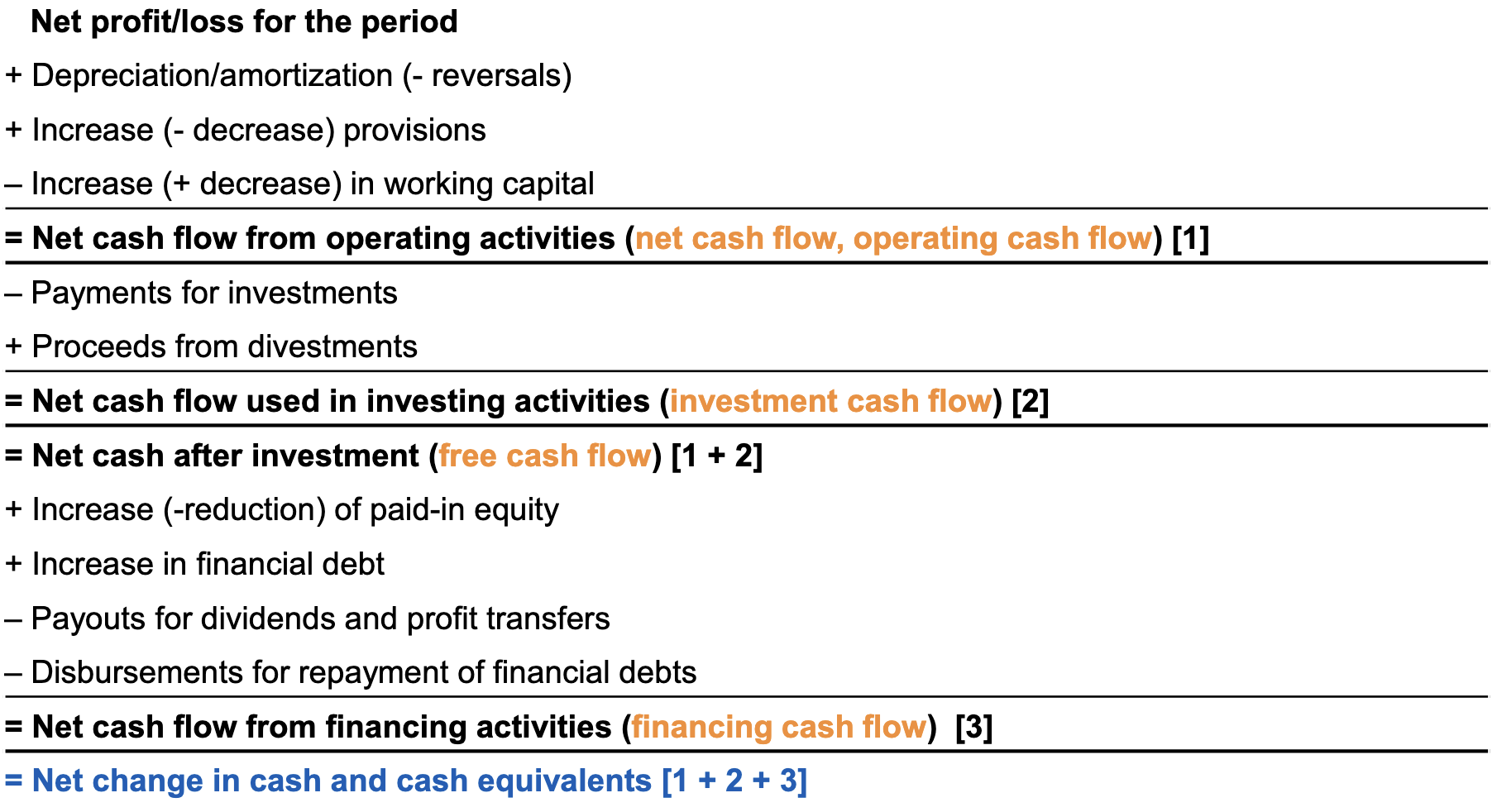

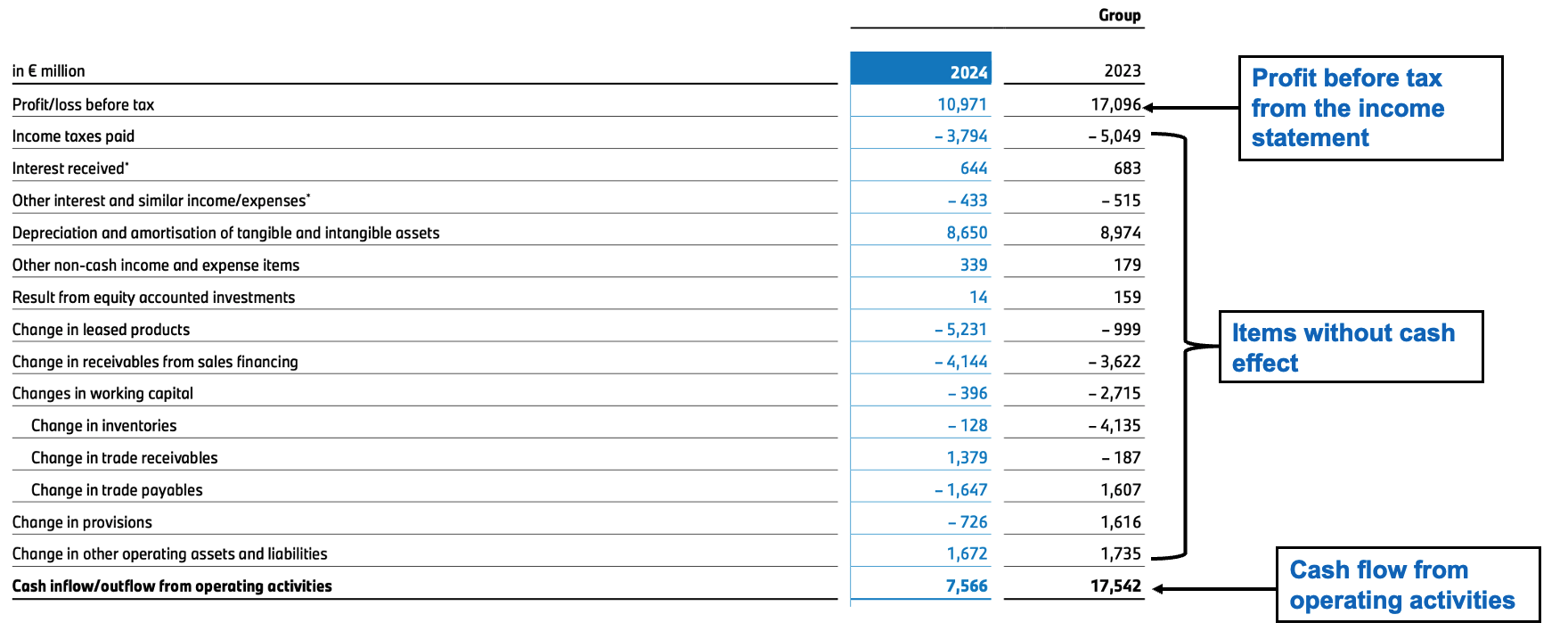

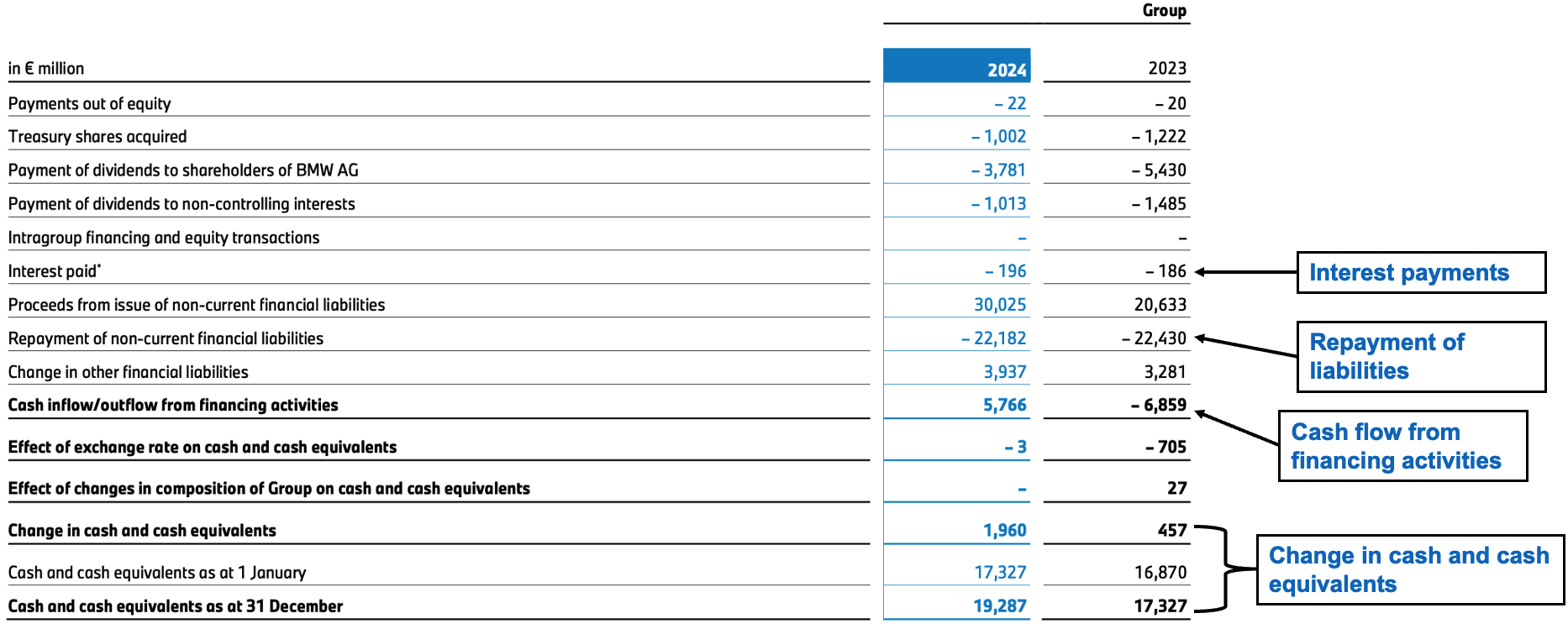

Statement of Cash Flows

Purpose: Shows how changes in the balance sheet and income affect cash and cash equivalents.

Bottom line: Net increase/decrease in cash and cash equivalents

The cash flow statement is divided into three sections:

- Operating Activities: Cash flows from the core business operations (e.g., cash received from customers, cash paid to suppliers)

- Investing Activities: Cash flows from buying and selling long-term assets (e.g., purchase of equipment, sale of investments)

- Financing Activities: Cash flows from transactions with owners and creditors (e.g., issueing shares, repaying loans)

The resulting cash difference affects the cash and cash equivalents reported on the balance sheet. The cash flow statement is a vital tool for assessing liquidity, solvency, and financial flexibility.

Simplified Structure of Cash Flow Statement:

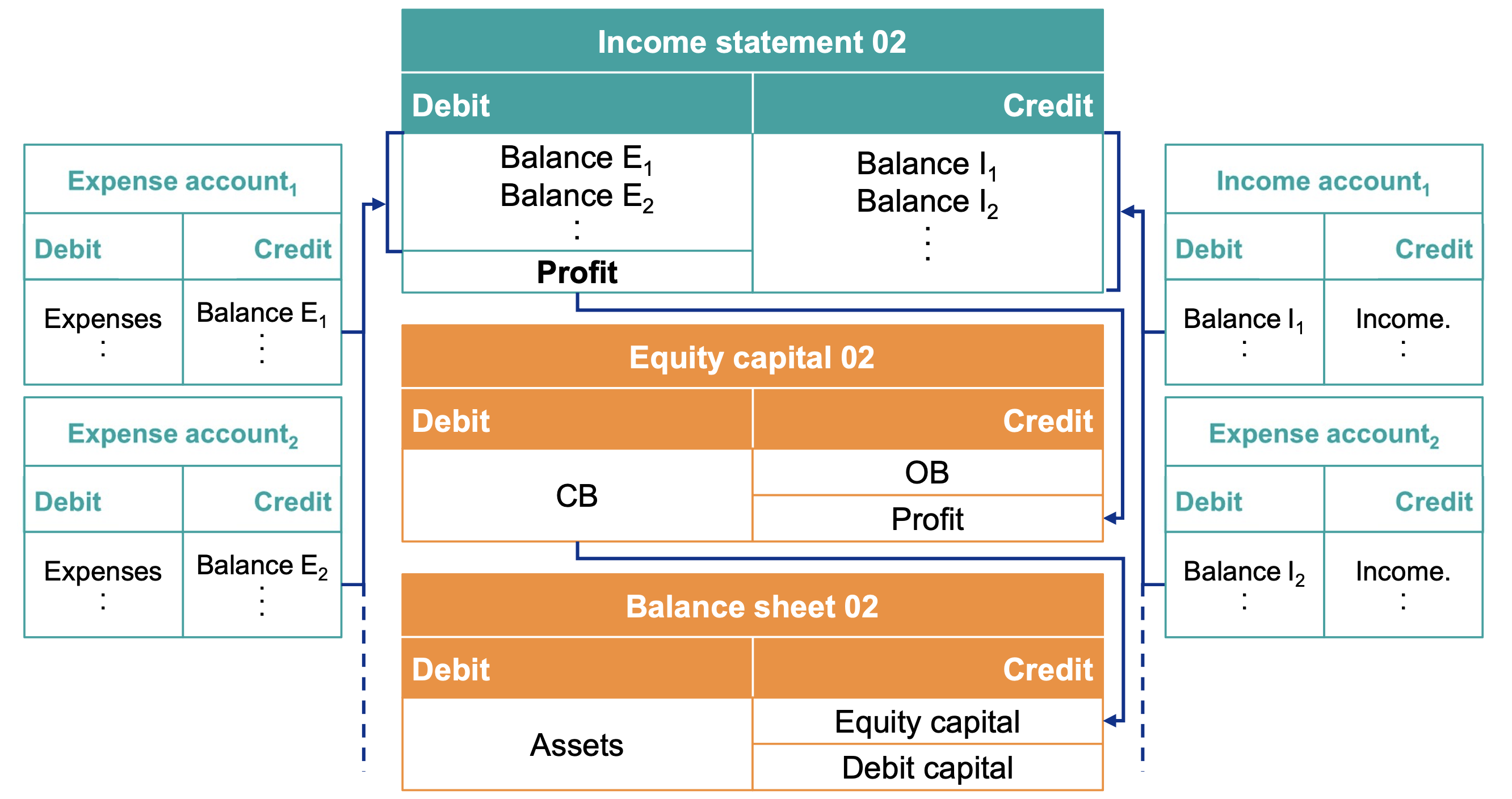

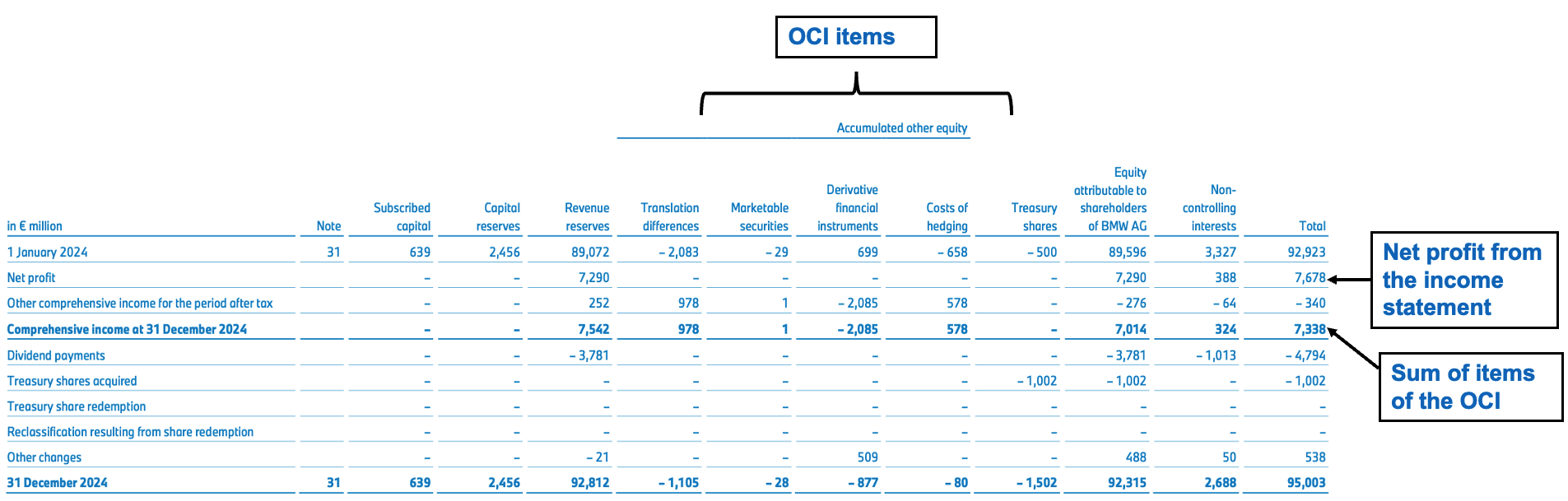

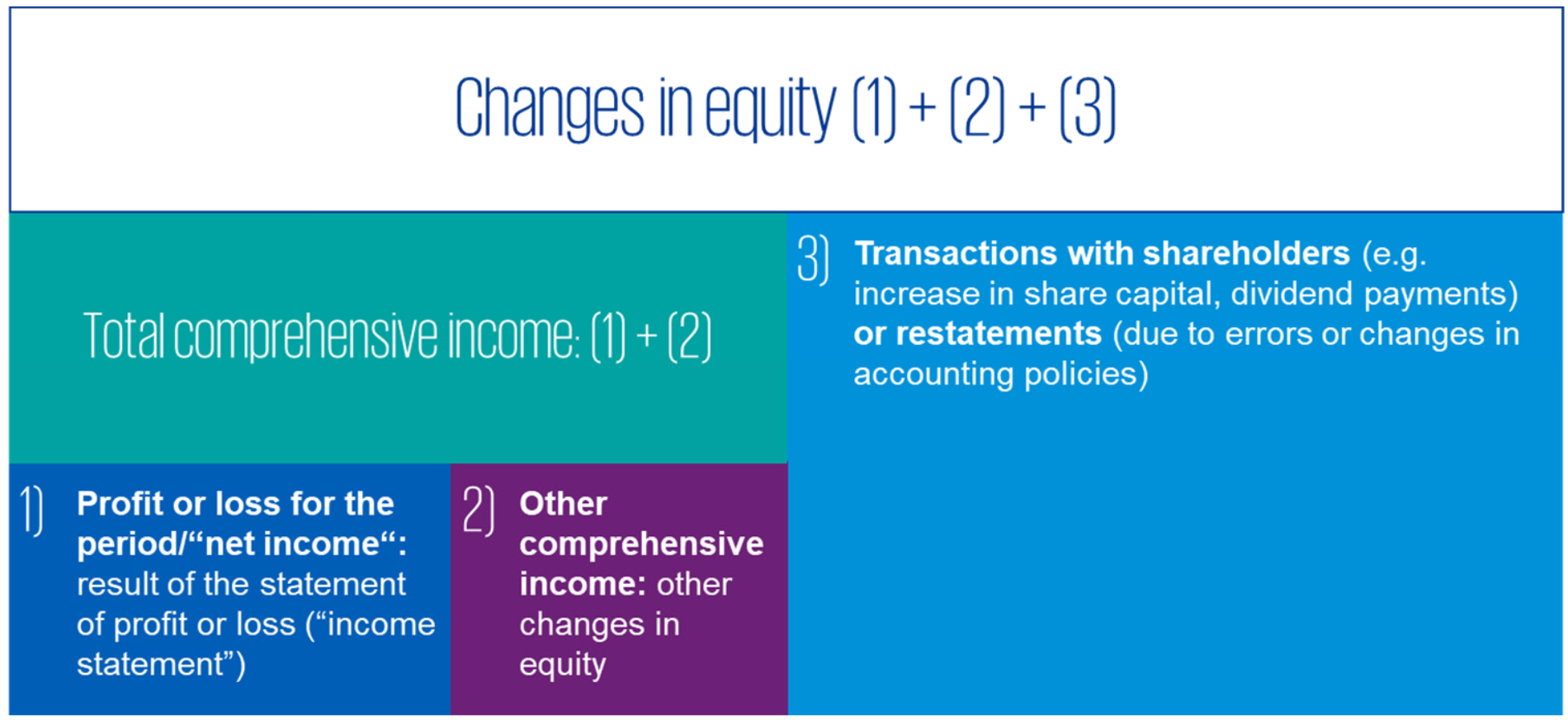

Statement Of Changes In Equity

Purpose: Shows how profits, dividends, shares, or other factors have affected shareholders’ equity during the period.

Bottom line: Total equity at the end of the period.

Equity represents the residual interest in the assets of the entity after deducting all its liabilities. It includes:

- Subscribed Capital: The capital a company receives from shareholders for the sale of shares.

- Capital Reserves: Additional paid-in capital from shareholders above the nominal (par) value of shares.

- Retained Earnings: Cumulative net income retained in the company rather than distributed as dividends.

- Treasury Shares: Shares that the company has repurchased from shareholders (this acts as a “contra-equity” account, reducing total equity).

There are three main factors that impact equity:

- Profit or Loss for the Period The net income or result from the regular income statement. This is the most direct operational way equity increases (profit) or decreases (loss).

- Other Comprehensive Income (OCI) Equity changes that bypass the income statement. They affect the company’s financial position (e.g., unrealized gains on certain investments or foreign currency translations) but are shown separately to keep the operational profit/loss “clean.”

- Transactions with Shareholders Changes not related to business operations, but rather to ownership structure or policy. This includes capital increases (issuing new shares), dividend payments, or restatements (corrections of past accounting errors).

Notes To The Financial Statements

Purpose: Provides additional context and explanations for the figures in the financial statements.

The notes include:

- Accounting standards (HGB, IFRS) applied

- Detailed descriptions of accounting policies

- Changes in the scope of consolidation

- Explanation of significant items in the financial statements

- Principles: Basic information like year-end date, presentation currency, company name, statement type

Notes are referenced from the table. They are an essential part of the financial statements, providing transparency and clarity, and may reveal earnings management practices. However, they are often lengthy and cover a wide range of topics.

The notes always start with the basis of preparation, including the applied accounting standards (e.g., IFRS, HGB) and significant accounting policies, explaining how specific items are measured and recognized. The third section, additional information, provides detailed breakdowns and explanations of significant items in the financial statements.

Additional Reports

Management Report

Purpose: Provides management’s perspective on the company’s performance, risks, and future outlook.

The report provides information on the group’s results and economic situation, opportunities and risks, and foreward-looking forecasts.

The management report includes, according to German Accounting Standard No. 20 (DRS 20):

- About the Group: Business model, strategy, objectives, value-drivers, internal management system

- Economic Report: Business performance, financial position, net assets, results of operations, financial and non-financial performance indicators

- Post-Balance Sheet Events: Significant events after the reporting period

- Expected Developments, Opportunities and Risks: Future outlook, risk management, comparing forecasts with actual developments

- Supplementary Report: E.g. internal control system

Independent Auditor’s Report

Purpose: Provides an independent opinion on the fairness and accuracy of the financial statements.

The auditor ensures compliance with the relevant accounting standards, identifies any material misstatements, and provides assurance to stakeholders. It includes components like:

- Audit Opinion

- Key Audit Matters