Resources

Motivation

Technical skills, knowledge of the accounting terms is fundamental to understanding bookkeeping, accounting rules, impacts of business transactions to financial statements, the relationship of group and individual financial statements, to understanding financial statement analysis, and the instruments of accounting policy

Accounting also refers to soft skills of understanding stakeholder expectations, communication and presentation of financial figures, understanding the relationships of a company’s activities and its economic environment impact. Lastly, accounting is about telling stories around financial figures.

The Role of Accounting

Accounting is the “language of business,” transforming economic activity into useful information for decision-making. (p. 2)

Purpose of Accounting

The primary purpose of accounting is to provide useful information to stakeholders for making good decisions, which ultimately contributes to a prosperous society. (p. 13) This involves three main roles:

- Valuation Role: Provides information about the ex-ante prospect of a company, forming a basis for financing.

- Stewardship Role: Provides information about the ex-post performance of a company, used for managing the firm and holding managers accountable. Example: Bad accounting is a top reason for insolvencies. (p. 16)

- Contracting Role: Provides a basis for contracts between the company and other parties (e.g., debt covenants, performance-based compensation). (p. 17)

Accounting in the Company Structure

This lecture focuses on accounting for enterprises/companies, which are distinct from public budgets or private persons. (p. 4) A company can be defined in two ways:

- Functional: A legal or natural person operating in an entrepreneurial manner.

- Institutional: An entity with commercial activity and a minimum level of institutional means. (p. 5)

Accounting functions as a core part of the Management Information System (MIS), which processes data from all functional areas of the company (e.g., procurement, production, sales) to support management decisions. Its key functions within the MIS are documentation, planning, and forecasting. (p. 9)

Types of Accounting

Accounting can be divided into different areas, each answering central questions for stakeholders. (p. 3)

External: Financial Accounting

Focuses on reporting to external stakeholders (investors, creditors, employees, tax, etc.).

Financial Accounting

Uses income and expenses to determine the success of the company over a period.

Flow values: Income / Expenses

Level of information: Changes in net assets of the period

Central question: How successful has the company performed within the last period?

Internal: Management Accounting

Provides information for internal decision-making.

Cost Accounting

Uses performance and costs to evaluate the benefit of individual short-term measures. Also cost-and-performance-accounting.

Flow values: Performance / Costs

Level of information: Operating profit

Central question: How beneficial are individual measures in the short-run?

Financial Planning

Uses cash inflows and outflows to assess future solvency.

Flow values: Cash inflows / Cash outflows

Level of information: Increase and decrease of cash and cash equivalents of the period

Central question: Is the future solvency secured?

Investment Planning

Uses cash inflows and outflows to assess investment profitability.

Flow values: Cash inflows / Cash outflows

Level of information: Present value

Central question: Are the planned or realized investments profitable?

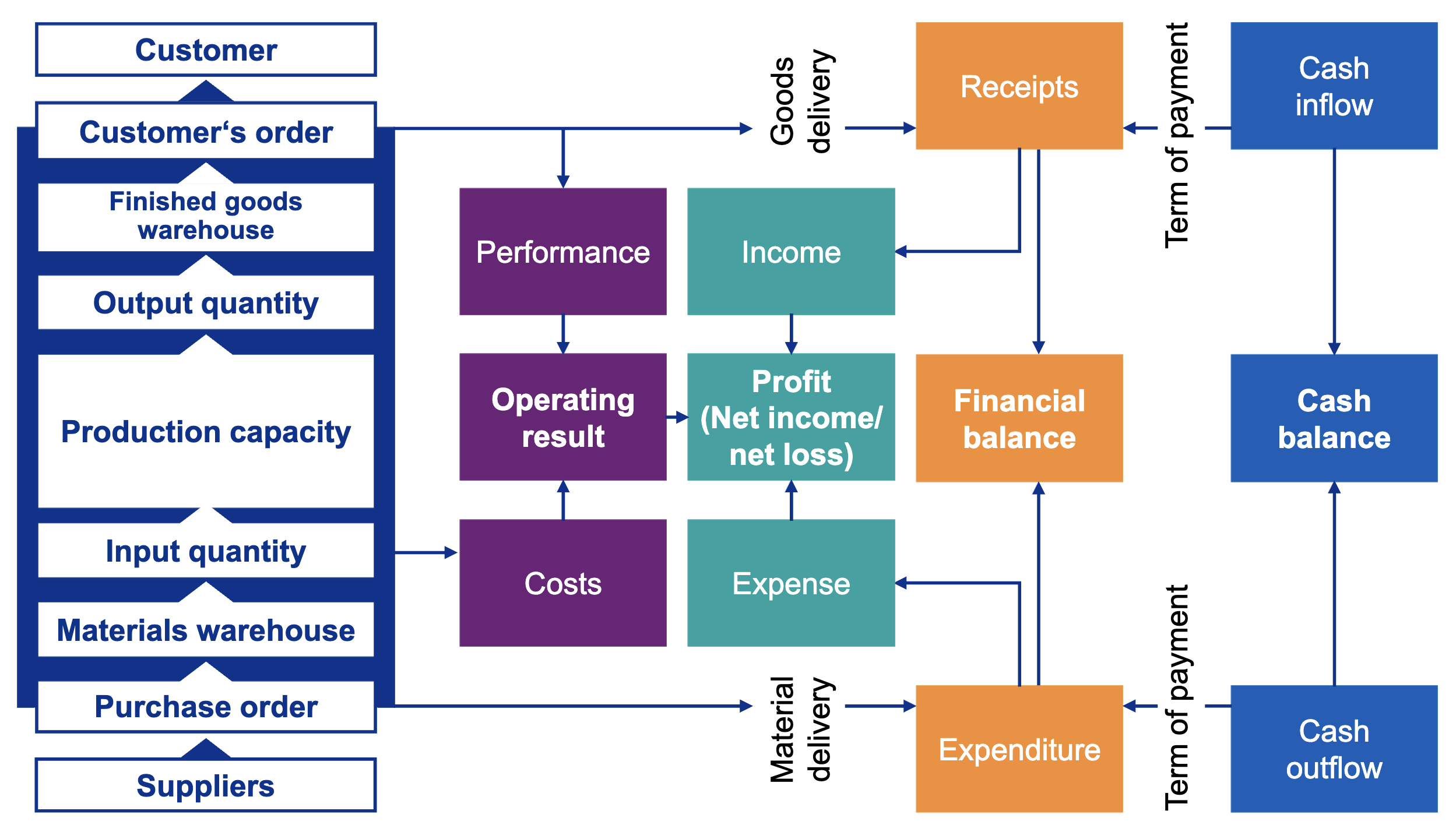

Fundamental Accounting Terms

Business transactions are recorded using a set of defined terms that measure different aspects of the flow of value. The relationship between these terms is crucial. (p. 2)

Cash Outflow and Inflow

Measures the change in cash and cash equivalents. Answers the question: “Is future solvency secured?” (p. 3)

- Outflow: A decrease in cash/equivalents.

- Inflow: An increase in cash/equivalents.

- Statement: Cash Flow Statement

- Balance: Payment Balance

Expenditure and Receipt

Measures the value of goods and services acquired or delivered, independent of the payment timing.

- Expenditure: Monetary value of goods/services acquired in a period.

- Receipt: Monetary value of goods/services delivered in a period.

- Balance: Financial Balance

Expense and Income

Measures the consumption or increase of economic value within a period, affecting net income. Answers the question: “How successful was the company last period?” (p. 3)

- Expense: Periodized, net-income-affecting expenditure. Represents the value of economic goods consumed in a period.

- Income: Periodized, net-income-affecting receipt. Represents the realized increase in value in a period.

- Statement: Income Statement / Profit & Loss Account

- Balance: Profit / Net Income

Cost and Performance

Measures the value consumed and created in the process of providing goods and services for the company’s primary operations. Answers the question: “How beneficial are individual measures in the short-run?” (p. 3)

- Cost: Monetarily assessed consumption of goods and services for operational purposes.

- Performance: Monetarily assessed increase in value from operational activities.

- Balance: Operating Result

Distinctions and Relationships

The timing of cash flow, value exchange, and consumption determines how a single transaction is classified across these different terms.

- Cash Outflow vs. Expenditure: An expenditure occurs when goods are acquired, while a cash outflow occurs when they are paid for. These can happen in the same period, or different ones. (Terms p. 5)

- Expenditure vs. Expense: An expense is the consumption of a good. An expenditure may become an expense in the same period it was acquired, or in a future period (e.g., depreciation of a machine). (Terms p. 6)

- Expense vs. Cost: Costs are a subset of expenses related to the core operating purpose of the business. Some expenses are non-operating (e.g., a loss from selling a machine) and are therefore not costs. Imputed costs (e.g., entrepreneurial salary in a sole proprietorship) are costs but not expenses. (Terms p. 11)

- Receipt vs. Income: A receipt occurs when goods are delivered. Income is the realized increase in value. A sale can be a receipt and income at once, or income can be recognized without a receipt (e.g., creating goods for inventory). (Terms p. 14)

- Income vs. Performance: Similar to the expense/cost distinction, performance is a subset of income related to core operations. (Terms p. 17)

Standard Business Processes

Accounting systems are built around standard processes that capture business transactions.

Purchase-to-Pay (Purchasing)

This cycle covers the acquisition of goods and services, from ordering to payment. It primarily involves expenditures, cash outflows, and expenses.

Examples of different timing scenarios for this cycle are detailed in the slides. (Terms p. 9-12)

Order-to-Cash (Sales)

This cycle covers the sale of goods and services, from receiving an order to collecting payment. It primarily involves receipts, cash inflows, and income. (p. 26-27)

Examples of different timing scenarios for this cycle are detailed in the slides. (Terms p. 15-16)

Fixed Assets Accounting

Manages the lifecycle of a company’s long-term assets (e.g., buildings, machinery), including acquisition, depreciation, and disposal.

General Ledger

The central repository for all accounting data from subprocesses. It contains all the accounts needed to generate financial statements.

Master Data Management

Ensures the accuracy and consistency of core business data (e.g., customer, vendor, and product information) used across all accounting processes.

Legal Framework & Principles

Double-Entry Bookkeeping is mandatory in most jurisdictions. Every transaction affects at least two accounts, maintaining the balance of the accounting equation: . This is contrary to single-entry bookkeeping.

- Germany’s accounting system is regulated mainly by the Commercial Code (HGB) and generally accepted framework principles (GoA).

- For specific company types (GmbHG, AktG, PublG), additional regulations apply and take precedence (primacy of application).

- IFRS is a globally recognized standard used for consolidated financial statements of listed companies in the EU.

- In the US, US-GAAP applies

Framework Principles (GoA - Principles of Proper Accounting)

Completeness: All transactions are recorded.

Accuracy & Neutrality: Records reflect true economic substance.

Transparency & Understandability: Information is clear and accessible.

Accruals Principles

Accruals Principle: Recognize activity when it is incurred, not when cash is exchanged.

Realization Principle: Recognize revenues only when they are earned and realizable.

Imparity Principle: Recognize unrealized losses when they are probable, but do not recognize unrealized gains.

Complementary Principles

Prudence: Avoid overstatement of assets/income. This encompasses the realization and imparity principles.

Consistency: Use the same accounting methods over time for comparability.

Going Concern: Assume the business will continue operating in the foreseeable future.

Single-Asset Valuation: Each asset and liability must be valued individually and not netted against others.

IFRS vs German GAAP

| Aspect | IFRS | German GAAP (HGB) |

|---|---|---|

| Major Principle | True and fair view | Prudence |

| Type of standards | Rules & Principle based | Principle based |

| Fair value orientation | High | Low |

| Statement of performance | Income + OCI | Income |

| Level of disclosure | High | Low |

Relevant Standards

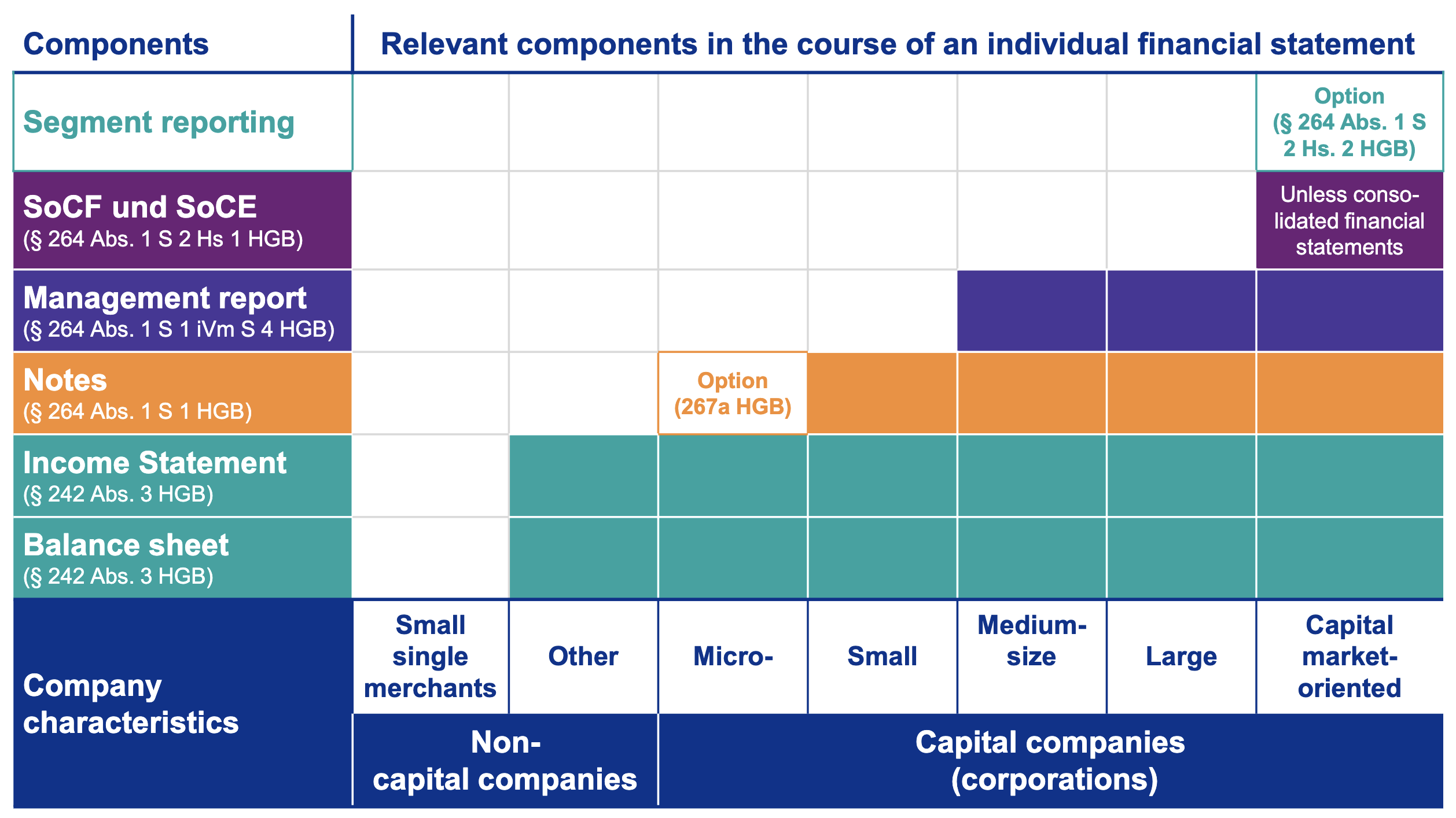

For Individual companies:

- Individual companies and partnerships have to comply with the common rules in the third book of HGB: §§ 238–263

- Capital companies / commandit partnerships: additional regulations in §§ 264–289 HGB

For consolidated financial statements:

- Non-capital market oriented parents companies have to comply with §§ 290–315d HGB; or provide consolidated accounting in accordance with IFRS (§ 315e HGB)

- Capital market oriented parent companies have to follow IFRS due to EU law

Company Structures

Unincorporated vs. Incorporated Companies

- Unincorporated Companies: These are not separate legal entities from their owners. Examples include sole proprietorships and partnerships. The owners are personally liable for the company’s debts.

- Incorporated Companies: These are legal entities separate from their owners (shareholders). This structure provides limited liability, meaning the owners’ personal assets are protected from business debts. Examples include corporations (like a German AG or GmbH).

| Criteria | Partnership | Capital companies |

|---|---|---|

| Position of partners | Personality of partners is paramount, they are responsible for daily business | Partners recede into the background in respect of daily business, the company itself is coming to the fore |

| Representation | Each partner has power of representation | Only management board has power of representation |

| Legal independence | Legal independence (capacity to enjoy rights and be subject to obligations) | Legal independence (capacity to enjoy rights and be subject to obligations) |

| Legal personality | Acting in legal communication is attributed to the natural persons behind | Acting in legal communication is attributed to the company, since it has its own legal personality (legal person) |

| Liability | Partners bear liability personally and unlimited for the company’s liabilities (Exception: limited partners) | Separation of company assets and partners (Partners do not bear liability for the company‘s liabilities) |

| Examples | OHG, KG, GbR | AG, GmbH, KGaA, GmbH & Co. KG |

Capital Market Oriented

- A company is considered capital market oriented if its equity instruments (e.g., shares, bonds) are publicly traded on a stock exchange or other regulated market.

- It is considered listed if its shares are admitted to trading on a stock exchange.

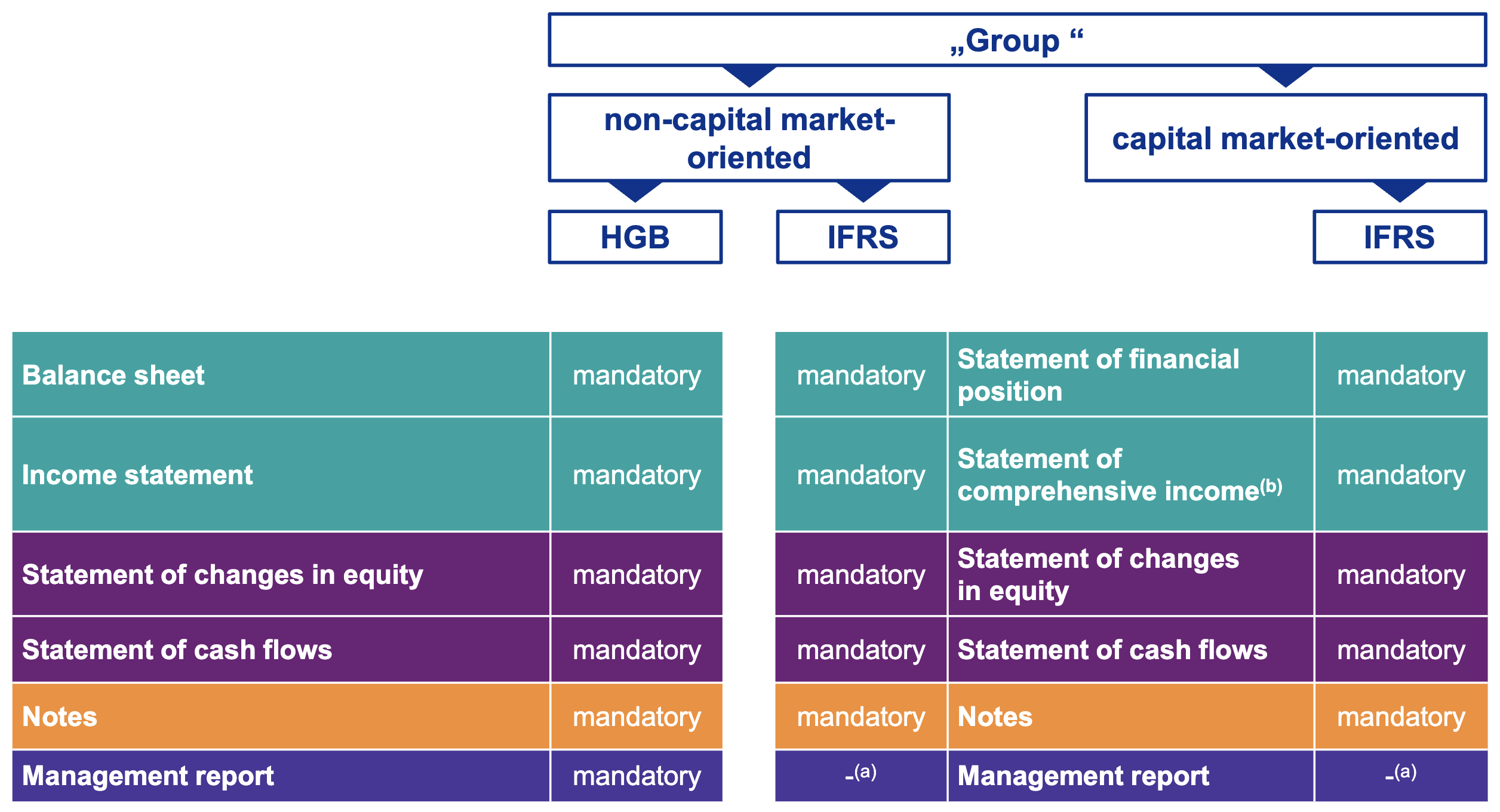

Financial Statements

Financial statements are the primary output of financial accounting, summarizing a company’s performance and position. More information in Financial Statement Components.

Balance Sheet

Presents a snapshot of a company’s financial position at a specific point in time.

- Assets: What the business owns (cash, inventory, equipment).

- Liabilities & Equity: What the business owes (loans, accounts payable) and what remains for owners (share capital, retained earnings).

Must be given: Assets = Liabilities + Equity

Income Statement

Shows the company’s financial performance over a specific period; also called Profit & Loss Statement.

- Revenues: Income from sales of goods/services.

- Expenses: Costs incurred to generate revenues (COGS, operating expenses, taxes).

Net Income (or Loss) = Revenues - Expenses

Cash Flow Statement

Provides information about cash inflows and outflows over a period, assessing liquidity and solvency.

- Operating Activities: Cash from core business operations.

- Investing Activities: Cash from buying/selling long-term assets.

- Financing Activities: Cash from borrowing/repaying debt and issuing stock.

Statement of Changes in Equity

Details changes in owners’ equity over a period due to net profit/loss, capital contributions, and dividends/withdrawals. Understanding this can help track owner’s interests.

Notes to the Financial Statements

Provide additional context, explanations, and disclosures related to the financial statements, helping users understand accounting policies, assumptions, and risks.

For consolidated statements, these are required by law.

Financial Statement Components

Consolidated Financial Statement Components

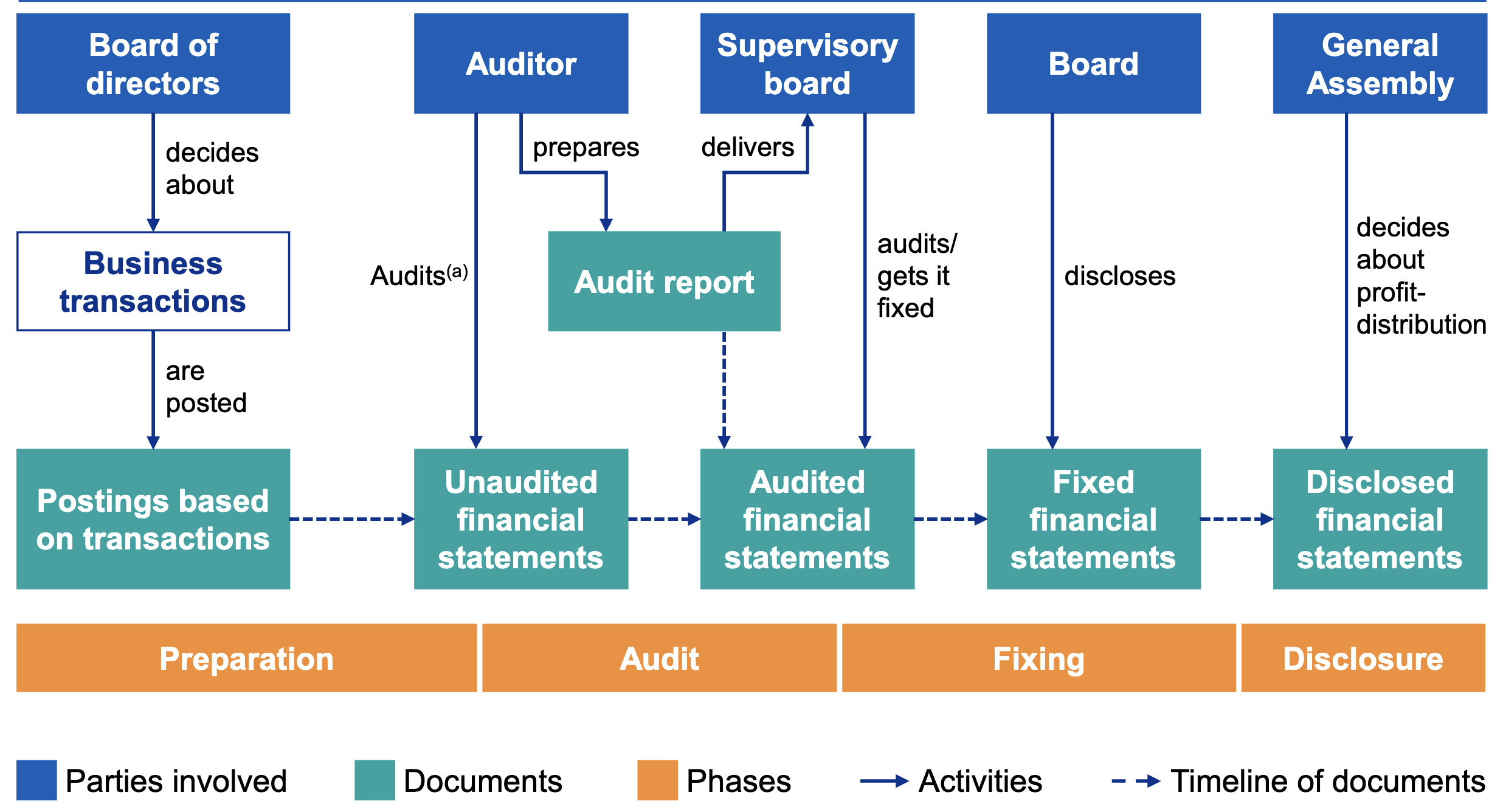

Annual Closing Process

Consequences of Accounting

Earnings Management

Accounting rules require judgment. These judgments can be influenced by their expected consequences, leading to earnings management: influencing reported earnings through accounting choices (within the boundaries of GAAP) to achieve specific objectives. (p. 30)

- Objectives: Meeting performance targets, influencing compensation, or “smoothing” income to report more stable growth, for example when raising capital.

- Methods: Decreasing discretionary spending, delaying projects, offering customer incentives to pre-book revenue, or drawing on reserves.

- Counter-parties: This behavior is monitored by boards, auditors, and enforcement bodies.

Earnings management is further discussed in Accounting Policy.