Resources

Market Failure

Definition

Market failure occurs when the individual optimization of consumers and firms leads to an outcome that is not optimal from a collective (societal) perspective. This failure to maximize welfare can justify government intervention (p. 3).

Common sources of market failure include:

- Market Power (e.g., Monopoly)

- Externalities

- Public Goods

Welfare Loss Summary Table

| Market Structure | Equilibrium | Social Optimum | Welfare Loss Formula |

|---|---|---|---|

| Perfect Competition | |||

| Monopoly | |||

| Negative Externality | |||

| Positive Externality | |||

| Public Goods |

Market Power: Monopoly

A monopoly market is served by a single firm (the monopolist) (p. 4).

Key Characteristics:

- Price Setter: The monopolist has market power; its output choice determines the market price given the downward-sloping demand curve.

- Information: The monopolist is perfectly informed about market demand but cannot identify individual consumer demands (p. 4).

- No Price Discrimination: The monopolist charges every consumer the same price for all units of the good (p. 4).

Natural Monopoly

A natural monopoly occurs when a single firm can supply the entire market at a lower cost than multiple competing firms, typically due to high fixed costs and economies of scale. Examples include utilities like water and electricity providers.

This is the case if average total costs decline over the relevant range of output:

In such cases, regulation or public ownership may be necessary to prevent monopolistic pricing and ensure efficient service provision.

Patent Monopoly

Patents grant exclusive rights to an inventor to prevent others from utilizing an invention.

- Rationale: If fixed costs for the inventor are higher than for imitators, patents are necessary to ensure non-negative profits and incentivize innovation (p. 11).

- Trade-off: Balances prospective welfare (future inventions) against present welfare (gains from trade from existing inventions).

Profit Maximization

The objective is still to maximize profit, which is revenue less total cost, however price is a function of quantity Q.

First-order condition for profit maximization:

Or expanded:

This condition can be solved for to find the the monopoly quantity . The monopoly price is then found by plugging into the demand function .

The Trade-off: A marginal increase in output has two effects on revenue (p. 5):

- Revenue Increase: Price charged for the marginal unit.

- Revenue Decrease: Price reduction aggregated over all inframarginal units (previous units sold).

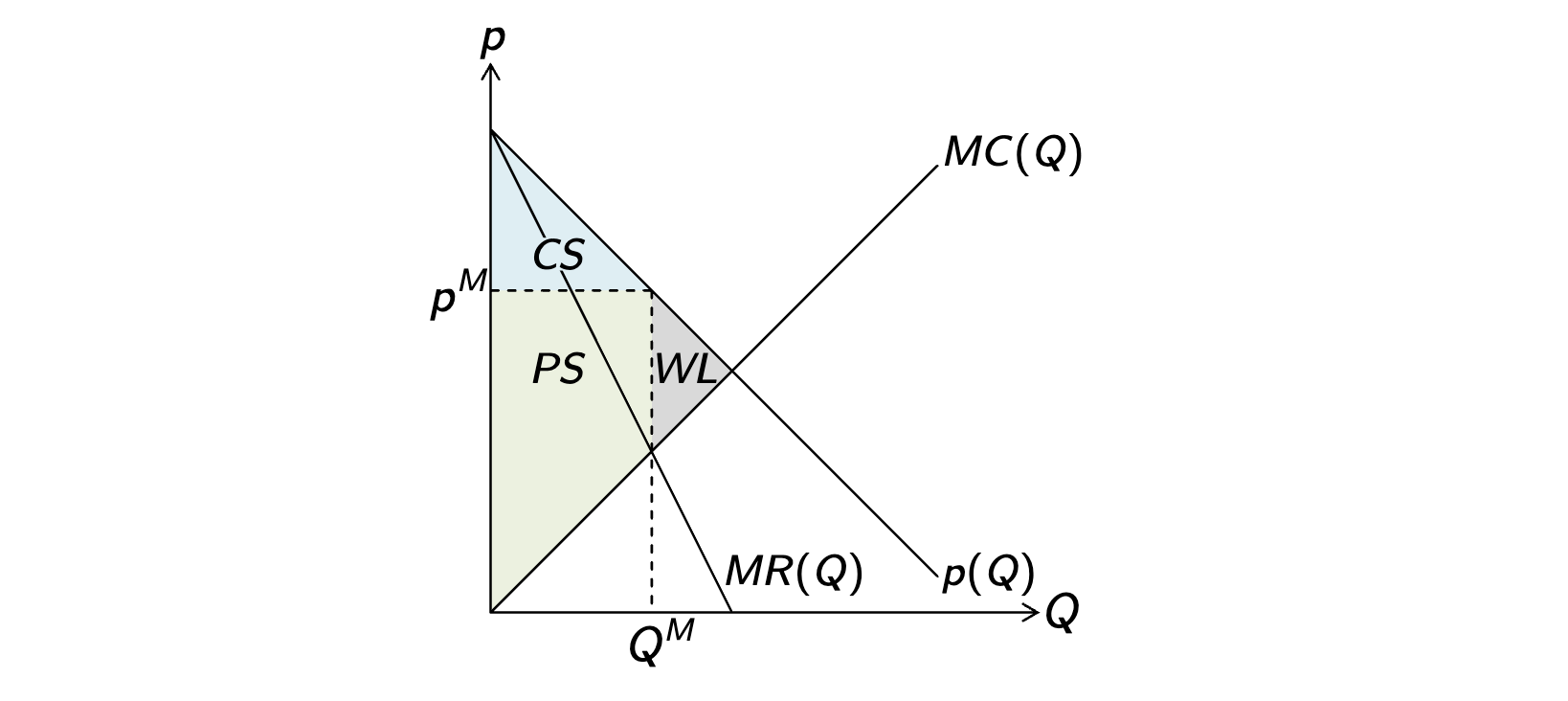

Equilibrium and Welfare

- Equilibrium: Occurs at quantity (where ) and price (p. 6).

- Welfare Loss: Because , not all potential gains from trade are realized. The result is a deadweight loss (WL) and reduced consumer surplus compared to perfect competition (p. 7).

Where is the competitive quantity, is the monopoly quantity, is the monopoly price, and is the marginal cost.

The producer surplus in monopoly is the area above the marginal cost curve and below the monopoly price up to the monopoly quantity. This is a rectangle (price minus marginal cost times quantity) plus the triangle between the demand curve and the monopoly price up to the monopoly quantity.

Monopoly Regulation

Government can use Price Control (Price Ceiling) to increase welfare (p. 12).

- Optimal Ceiling: Set price where inverse demand equals marginal cost: to eliminate deadweight loss by increasing output to the competitive level.

- Natural Monopoly Issue: At the welfare-maximizing price (), a natural monopolist may incur losses (since ). This requires subsidization or nationalization.

Externalities

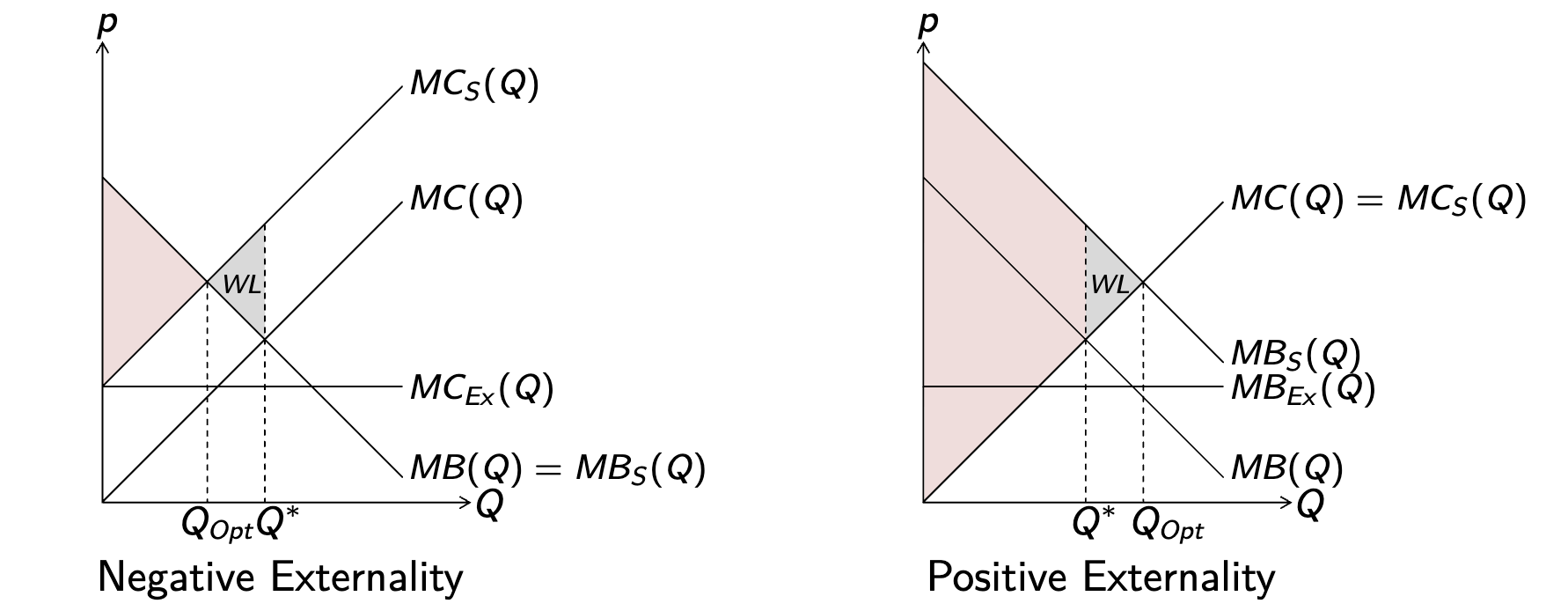

Externalities are uncompensated costs or benefits resulting from production or consumption choices that affect third parties (p. 13).

-

External Costs: Uncompensated effects negatively impacting third parties (e.g., pollution). Private marginal costs are only internal cost and represent the marginal willingness to accept of the producer (inverse market supply). Social marginal costs include external costs :

-

External Benefits: Uncompensated effects positively impacting third parties (e.g., vaccination). Private marginal benefits are only internal benefits and represent the marginal willingness to pay of the consumer (inverse market demand). Social marginal benefits include external benefits :

Welfare Loss from Externalities

The welfare loss is the area between the social and private curves from the market quantity to the optimal quantity (p. 14). With external costs, the market produces more than the socially optimal quantity, while with external benefits, it produces less.

Externalities Regulation

- Quantity Regulation: Force production/consumption to choose .

- Requirement: Information on social marginal costs and benefits (p. 15).

- Corrective Taxation (Pigouvian): Tax or subsidy to align private incentives with social welfare.

- Requirement: Information on external marginal costs or benefits.

- A Piguovian tax per unit for negative externalities (or subsidy for positive externalities) internalizes external costs (or benefits), leading to the socially optimal quantity .

- Bargaining (Coase Theorem): If property rights are well-defined, parties can negotiate the optimal outcome regardless of who holds the rights.

- Limitation: Often hindered by transaction costs.

Public Goods

Goods are classified by Rivalry and Excludability (p. 16):

| Excludable | Non-Excludable | |

|---|---|---|

| Rival | Private Goods | Common Resources |

| Non-Rival | Club Goods | Public Goods |

- Rival: Consumption by one diminishes consumption possibilities for others.

- Excludable: Individuals can be prevented from consuming the good.

- Public Good: Neither rival nor excludable.

Welfare Loss

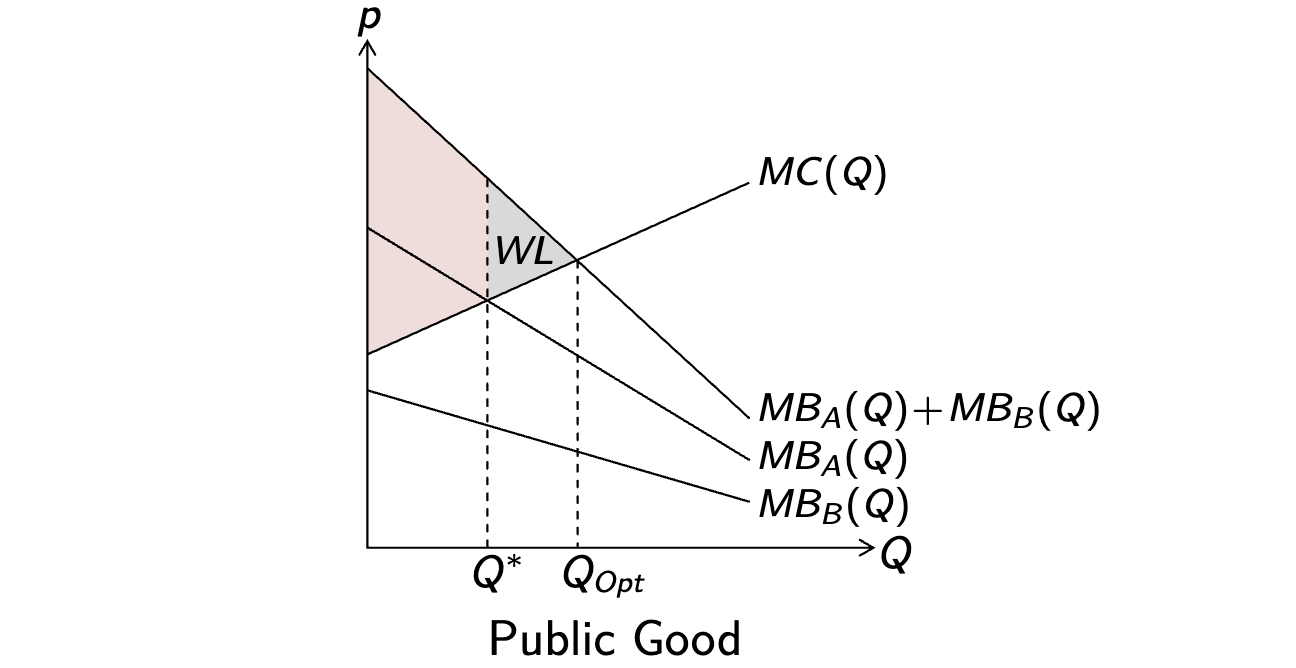

- Free-Rider Problem: Individuals rely on others to provide the good, leading to undersupply () (p. 17).

- Private Provision: Individuals provide where .

- Social Optimum (Samuelson Condition): The sum of marginal benefits equals marginal cost (p. 18).

Requirement: Collective provision requires info on marginal benefits of all consumers and marginal costs.

The welfare loss from under-provision of public goods is the area between the combined marginal benefit curve (sum of individual marginal benefits) and the marginal cost curve from the actual quantity to the optimal quantity.

Example Problem

These are the market failure problems from exercise exam 2 and exercise 5 with some questions from exercise exam 1.

Monopoly

Market demand is:

The monopolist has total costs:

Preparation

Inverse Demand: Price Function

Marginal Cost, Revenue, Marginal Revenue

Questions

What are the monopoly equilibrium quantity and price, as functions of and ?

Set to find , then plug into to find :

What is the minimum fixed cost such that the monopolist produces a positive quantity?

Set profit to find :

What is the welfare loss due to monopoly pricing?

and are known, find using , then apply WL formula:

Assume and . What’s the profit after a tax of per unit?

Set to find new , then find profit:

Externalities

There are 2 identical firms producing a good with market demand:

Each firm has total costs:

Preparation

Inverse Demand: Price Function

Marginal Cost, Social Marginal Cost

Questions

Individual profit maximization results in an equilibrium where each firm’s profit is?

Set for individual firms to find , then find and profit. This is the same as in Perfect Competition, only that

What is the welfare-maximizing quantity and price?

Set to find , then find and (assuming ):

What is the welfare loss through individual profit maximization?

Welfare-maximizing and individual profit-maximizing quantities are given above: now apply WL formula:

With a Pigouvian tax applied, what subsidy is required for each firm to maximize profit at the welfare-maximizing quantity?

The Piguovian internalizes external costs. Therefore, add tax to costs and subsidy to profit, set , where C(q) includes costs arising from other’s external costs ().

, then find subsidy :

Public Goods

There are 5 individuals with costs of:

and marginal benefits:

Preparation

Marginal Cost, Sum of Marginal Benefits

Questions

What is the welfare-maximizing quantity of the public good?

Set to find :

What is the welfare loss through individual provisioning of the public good?

Each individual provides the good up to , then use WL formula:

Approaches

Monopoly

- Find Monopoly Equilibrium ():

- Determine the inverse demand function from market demand .

- Calculate Total Revenue and Marginal Revenue .

- Set to solve for , then plug into to find .

- For welfare-maximizing, use the competitive equilibrium at

- Profit & Entry Condition:

- The monopolist produces only if . To find the maximum fixed cost , solve .

- Welfare Loss (WL):

- Find the competitive quantity where .

- Calculate .

Externalities

- Social Optimization:

- Identify private marginal costs () and external marginal costs ().

- Set price equal to Social Marginal Cost: to find .

- Welfare Loss:

- Find the difference between market quantity and socially optimal quantity .

- Apply the formula .

- Pigouvian Tax:

- Set tax (at ) to internalize the external cost.

Public Goods

- Samuelson Condition (Social Optimum):

- Sum individual marginal benefits vertically: .

- Set to solve for .

- Individual Provision (Free-Riding):

- Find the equilibrium where an individual’s private benefit equals marginal cost: . If is always higher than , .

- Welfare Loss:

- Calculate using .