Resources

Context

Multiple firms compete by selling identical products to many buyers. Firms are price takers, meaning they cannot influence the market price and must accept it as given. This combines demand and supply analysis.

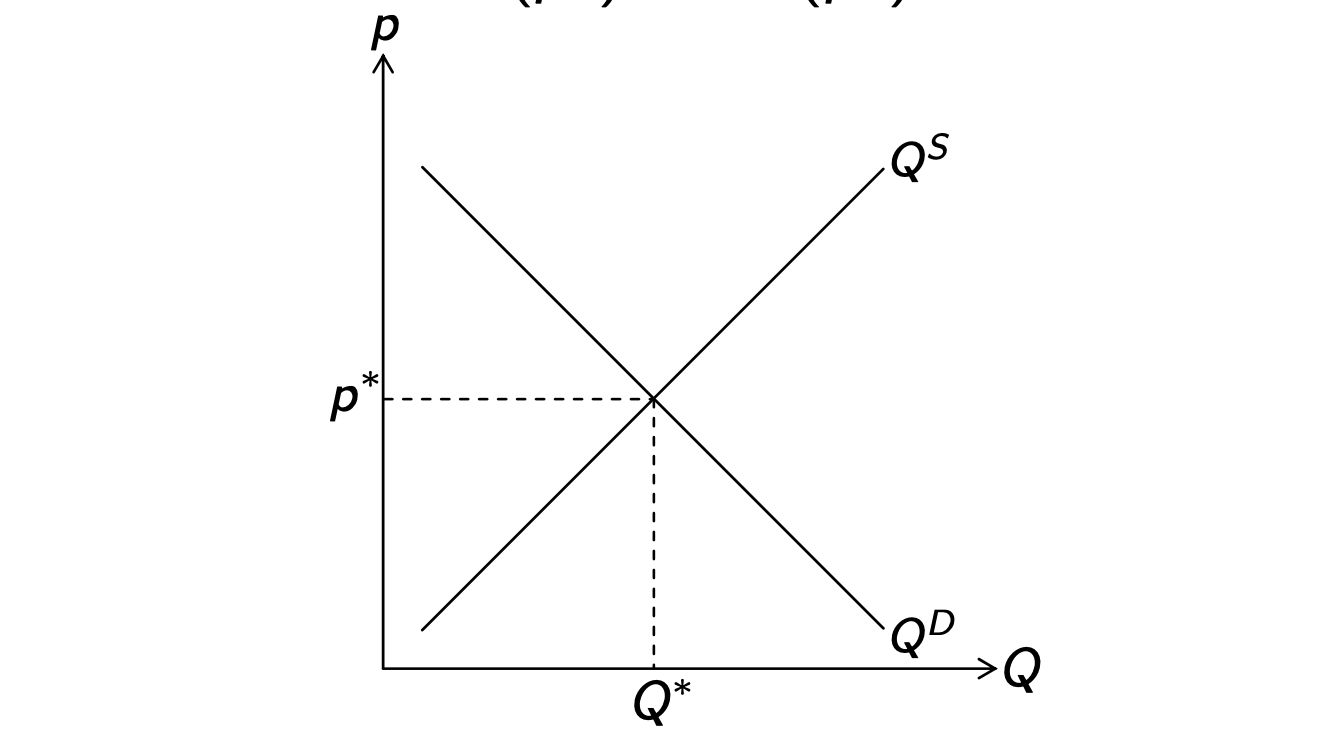

An individual firm’s output is , the market quantity (traded) is , market supply and demand are and , and the market price is .

- The demand function is typically downward sloping: as price decreases, quantity demanded increases

- The supply function is typically upward sloping: as price increases, quantity supplied increases

- Equilibrium occurs where quantity demanded equals quantity supplied

Perfect Competition Assumptions

- All producers and consumers are price takers

- Firms are identical

- There is an integer number of firms in the market

- Firms are free to enter and leave the market

- Perfect information is available to all participants

- An ordinary good is supplied (downward sloping demand)

- Firms produce at increasing marginal costs (upward sloping supply)

Equilibrium

The goal is to find the equilibrium price and equilibrium quantity where market demand equals market supply:

For many problems, it is crucial to determine the minimum average cost (or average variable cost). The minimum occurs at a quantity satisfying:

Market Equilibrium

The market is in equilibrium for a given price when market demand equals market supply :

is called the clearing quantity.

In the long run, competitive equilibrium requires:

In the short run, the relevant condition is often:

Market Imbalance

If no market equilibrium exists at a given price, there is either excess demand or excess supply:

- Excess Demand (Shortage): If price is below the equilibrium price , quantity demanded exceeds quantity supplied .

- Excess Supply (Surplus): If price is above the equilibrium price , quantity supplied exceeds quantity demanded .

In both cases, the quantity traded is less than the equilibrium quantity .

Number of Firms

Short Run: The number of firms is fixed.

Long Run: Additional firms enter the market if this yields non‑negative profits or exit the market if they make losses.

Long‑run equilibrium requires:

Given the equilibrium price, the number of firms is:

Market Supply

Market supply is the sum of all individual firms’ supplies.

- Short Run:

- Long Run:

Firms enter the market as long as profits after entry are non‑negative or exit if they make losses .

Reservation Prices

Marginal Willingness to Pay: Demand Side

Given a quantity , the inverse market demand is the maximum price that consumers are willing to pay for an additional unit of the good. It is the inverse demand function, i.e. solved for :

Marginal Willingness to Accept: Supply Side

Given a quantity , [[Production and Supply#|marginal costs]] measure the minimum price that producers are willing to accept for an additional unit of the good. It is the inverse supply function, i.e. supply solved for :

Competitive Equilibrium

If consumers and producers face the same market price, the market is in equilibrium at the clearing quantity :

Welfare

Welfare analysis evaluates the efficiency of market outcomes by examining the distribution of benefits among consumers and producers.

Surplus

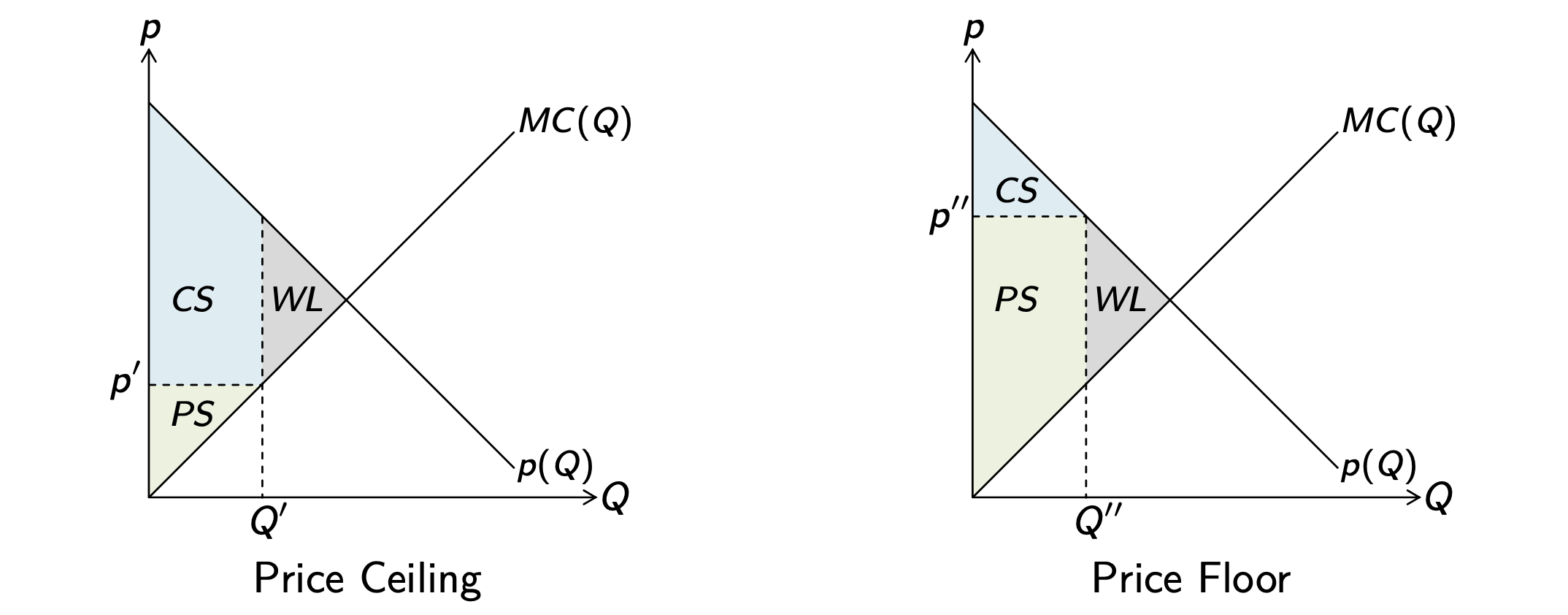

Consumer Surplus (CS): The difference between what consumers are willing to pay (marginal willingness to pay, or the inverse market demand) and what they actually pay (the market price). It represents the net benefit to consumers.

Producer Surplus (PS): The difference between the market price and the minimum price producers are willing to accept (marginal willingness to accept, or marginal costs). It represents the net benefit to producers.

Total Surplus (TS) is the sum of consumer and producer surplus:

Here, is the choke price (maximum price at which demand falls to zero), is the minimum price for supply (e.g. from ), and and are the equilibrium price and quantity.

Welfare Maximum and Loss

Welfare Maximum: Welfare is maximized if the market is in competitive equilibrium, so total surplus is maximized. At the market clearing quantity , all potential gains from trade are realized.

Welfare Loss: A welfare loss occurs when the inverse market demand (marginal willingness to pay) exceeds marginal cost at the traded quantity. This indicates a market that is not in equilibrium, leading to unrealized gains from trade. Untraded quantities can also lead to welfare loss, but this is not part of perfect competition.

Market Interventions

Price Control

Price Control

An upper or lower limit on the market price is called a price ceiling or price floor, respectively.

- Price Ceiling at implies:

- Price Floor at implies:

Both lead to welfare loss due to unrealized gains from trade, if the price control is binding (i.e., effective).

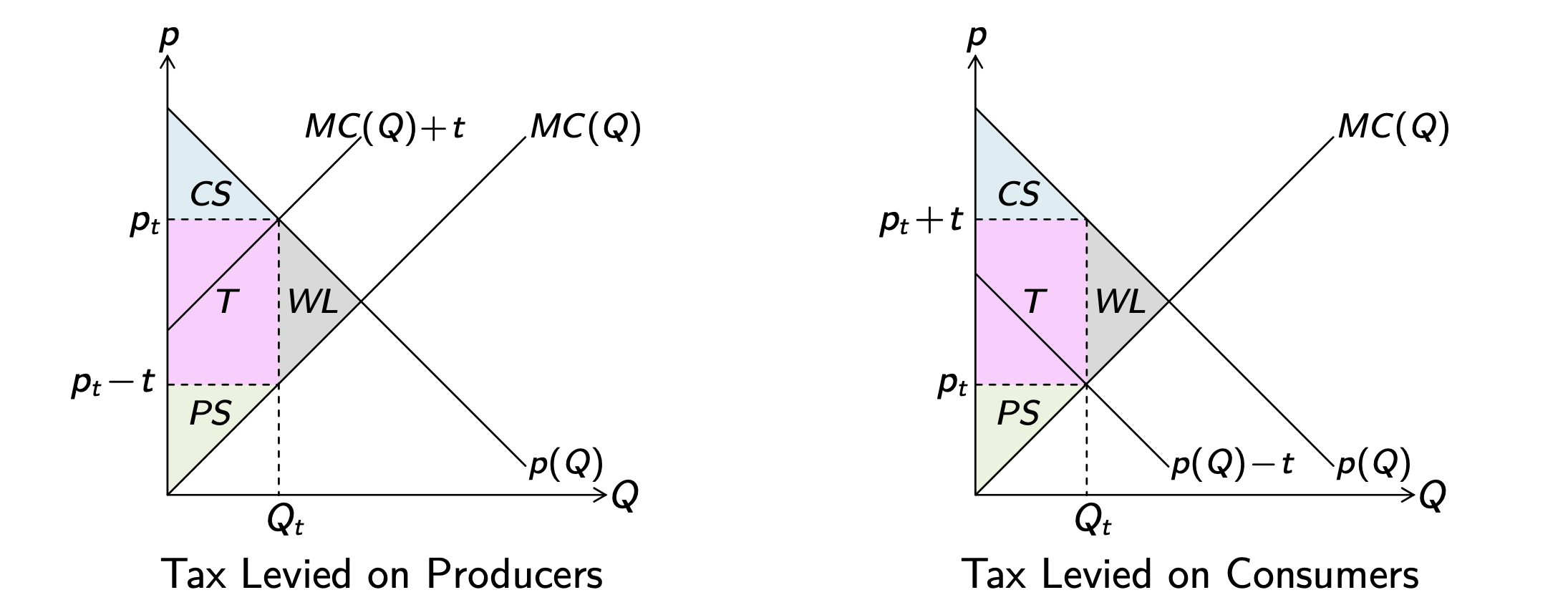

Taxation

Taxation

A tax imposed on consumers or producers affects the market equilibrium in the same way: it drives a wedge between the price paid by consumers and the price received by producers, and it decreases both consumer and producer surplus.

For a per‑unit tax :where is tax revenue and is the traded quantity under the tax.

In equilibrium, the tax wedge satisfies:where is the traded quantity with the tax.

Welfare loss under taxation:

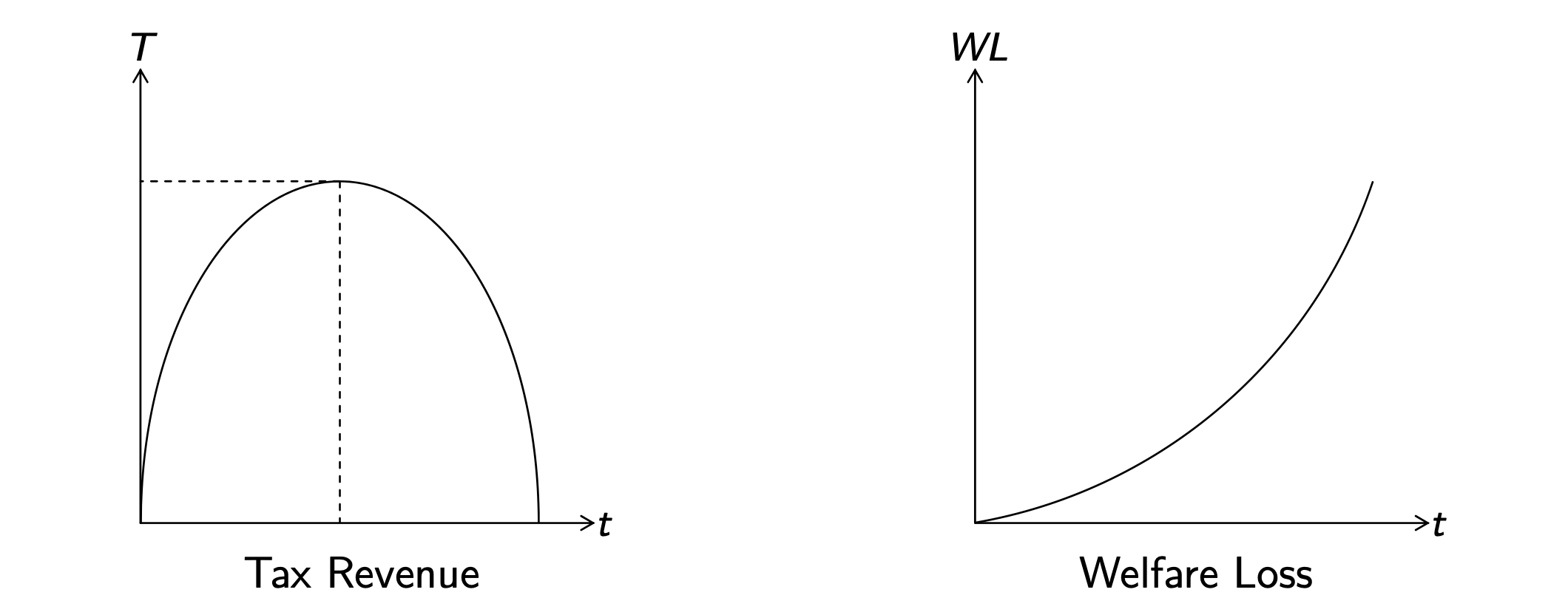

Change in Tax Rate

If an increase in the tax rate decreases the traded quantity (the tax base), this results in:

- An increase in tax revenue if the tax rate is sufficiently small, and a decrease in tax revenue if the tax rate is sufficiently large

- A higher welfare loss due to taxation as the tax rate rises

Example Problem

This is the perfect competition problem from exercise exam 2 with questions from Exercise 4 and exercise exam 1.

Market demand:

Each firm has total costs:

Preparation

Marginal and Average Costs

Individual supply , break‑even quantity , and long‑run equilibrium price

Questions

Equilibrium number of firms is . What is ?

Note:

Long‑run number of firms in equilibrium at ?

We must then check the profit condition: if at , no firm would produce.

Therefore, the long‑run number of firms is .

Producer surplus in equilibrium at ?

Since is not an integer in the unconstrained calculation, the actual equilibrium price is not exactly at (see above). Therefore, there is a positive producer surplus.

Consumer surplus in equilibrium at ?

Given , what is the welfare loss from a tax of ?

Before the tax:

After the tax:

At , what is the welfare loss from a price ceiling at ?

Before the price ceiling:

After the price ceiling:

However, since (18 < 20), the market shuts down, since no firm can produce without losses. Therefore, the welfare loss equals the entire surplus before the price ceiling:

If firms would still produce, the welfare loss would be the difference between total surplus before and after the price ceiling, or half the difference in quantity traded times the price difference.

At , if a tax rate of is introduced, what is the equilibrium output per firm?

Since must be an integer, we check the equilibrium price at :

Thus, equilibrium output per firm is:

Approaches

Equilibrium & Firms

- Find Long-Run Equilibrium Price (): Solve for the minimum average cost by setting (or ). The price in the long run must satisfy .

- Find Short-Run Equilibrium Price (): If the number of firms is fixed, set market demand equal to market supply: (or ).

- Find Number of Firms ():

- In the long run: , where is the total market quantity and is the firm quantity.

- Since must be an integer, if the result is a decimal (e.g., 5.25), round down to the nearest integer (e.g., ) and recalculate the actual using the short-run method to ensure profits are non-negative ().

Welfare & Surplus

- Consumer Surplus (CS): Calculate the area of the triangle: . Find by setting .

- Producer Surplus (PS):

- If free entry and is perfectly divisible, in the long run.

- If is fixed (short run or integer constraint), (Total Revenue minus Variable Cost), where is the price at which the individual supply curve begins ( or ).

- Total Surplus (TS): Sum of .

Market Interventions

- Taxation ():

- The new price paid by consumers becomes (assuming a perfectly elastic supply in the long run).

- New quantity: .

- Welfare Loss (Deadweight Loss): .

- Price Ceiling ():

- If : The market shuts down () because no firm can cover costs. Welfare loss is the entire potential Total Surplus.

- If : Calculate the quantity supplied at that price. Welfare loss is the area of the triangle formed by the untraded units between the demand and supply curves.

Reservation Prices

- Marginal Willingness to Pay: Solve the demand function for to get the inverse demand function .

- Marginal Willingness to Accept: This is the inverse supply function, which is the Marginal Cost curve: .