How are objectives of companies set?

Resources

- Slides

- Literature: Cyert, March 1963, Freeman 20

Conceptual Views of the Firm

Production View

The production view describes the firm as a simple transformer of inputs from suppliers into outputs for customers, where satisfying these two groups is seen as sufficient for success, typically in small, owner-managed firms and stable environments.

Managerial View

The managerial view emphasizes the separation of ownership and control, sees the firm as a resource-conversion entity measured in monetary terms, and focuses managers on balancing the interests of owners, employees, suppliers, and customers through internal structures and control systems, but it underestimates the growing complexity of the external environment.

Stakeholder View

The stakeholder view understands the firm as a network or coalition of stakeholder relationships, including shareholders, employees, suppliers, customers, governments, NGOs, media, and others, and it focuses management on creating and distributing value among multiple interdependent groups in a turbulent environment.

Stakeholder Relationships

- Stakeholders are groups or individuals who can affect or are affected by the achievement of the organization’s objectives.

- Key stakeholders include shareholders, sources of supply (employees, creditors, suppliers), customers, and the public (country, society, regulators). (p. 4)

- Management’s role is to manage the relationships with these stakeholders, guided by corporate governance. (p. 9)

- Different groups can have a different impact on the corporation, regulated by the corporate governance (usually US: 1 tier, Germany: 2 tier - supervisory & management board).

Shareholder (p. 7)

- Contribution: Provide currency and information.

- Interest: Expect profits and information about the corporation.

Sources of Supply (p. 6)

- Contribution: Provide production factors like labor, material, and currency.

- Interest: Expect currency, interest, and information about the corporation.

Customers (p. 5)

- Contribution: Provide currency and information.

- Interest: Expect products, services, and information about the corporation.

Public (p. 8)

- Contribution: Provide infrastructure, legal systems, and information.

- Interest: Expect market participation, contributions to development, and information about the corporation.

Objectives

- Objectives of a corporation are normatively set for the entire organization.

- Objectives for a corporation are individual goals of stakeholders.

- As different stakeholders have different objectives, objectives for a corporation may differ. They can be congruent, independent, or conflicting. (p. 13)

- (Slide 12)

Prioritization and Instrumentalization

- Prioritization: When objectives of different stakeholders conflict, management must prioritize which objectives to pursue.

- Instrumentalization: Management may use certain stakeholders/objectives as means to achieve the objectives of other stakeholders (for example, sustainable systems in a circular economy).

Setting Objectives

- Objectives can be maximizing (assuming homo oeconomicus) or satisfying. (p. 15)

- Maximizing: Best possible outcome (highest profit, market share).

- Satisfying: “Good enough”, meeting aspiration levels or constraints.

- Aspiration levels are determined by comparing goals with the company’s own past performance, the performance of others, and unexpected events. (p. 16)

- Top management facilitates a political process to determine the company’s objectives. (p. 18)

- Aspiration levels are inherently relative and therefore path dependent. If the peer group becomes more profitable, aspiration levels tend to move up, even if own performance remains constant.

- Path Dependent: Based on past decisions and history; past performance.

- Path Independent: External influences; unexpected shocks or regulatory changes.

- (in contrast to path independent: unexpected shocks, regulatory changes).

Aspiration Level Theory (Cyert & March)

Firms and managers satisfice: they aim to reach aspiration levels rather than strict maximization. Aspiration levels are shaped by:

- Own past performance

- Performance of relevant others (peers, competitors)

- Expectations and available information about the environment

Performance below aspiration triggers problemistic search and strategic change; performance above often stabilizes current strategy.

Organizational Slack

The difference between resources available and minimum payments needed to keep the stakeholder coalition together.

This can be higher wages or benefits than strictly necessary, extra budgets and comfortable cost levels, perks and status goods for managers, or prices/dividends more generous than required to retain buyers/investors.

Organizational slack works as buffer and stabilizer, cushioning the firm against environmental variability.

Objective Systems

Shareholder Approach (p. 20)

- Perspective: Companies exist to create welfare for their owners.

- Definition of Success: Maximization of discounted future cash flows for owners.

- Primary Objective: Shareholder Value.

- Consequence: Instrumentalization of other stakeholders to achieve owner objectives.

: Payments to Owners (in t), : Pay-Offs to Owners (in t), : Cost of Equity (expected return)

Stakeholder Approach (p. 20)

- Perspective: Companies are coalitions of stakeholder groups.

- Definition of Success: Maximization of the benefits for all groups.

- Primary Objective: Stakeholder Value.

- Consequences: Requires interpersonal benefit-cost comparisons and prioritization. May be socially questionable.

- Example: Relocating a factory may benefit shareholders but harm employees and the local community.

: Stakeholder, : Benefits (to j, in t), : Costs (to j, in t), : Discount rate (of j) (expected return)

Because of the interpersonal benefit-cost, the stakeholder approach is difficult to operationalize, requiring value judgements. The shareholder approach, on the other side, is comparatively easier to operationalize via discounted cash flows and WACC.

Corporate Social Responsibility (CSR) & Triple Bottom Line

- CSR: A management concept where firms align strategy and operations with the societal and environmental expectations of their stakeholders, not just shareholders.

- Triple Bottom Line (TBL): Extends success beyond profit to people, planet, profit and fits a stakeholder-oriented objective system.

- In practice, CSR initiatives and TBL metrics translate broad stakeholder expectations into concrete objectives and criteria for governance and performance measurement.

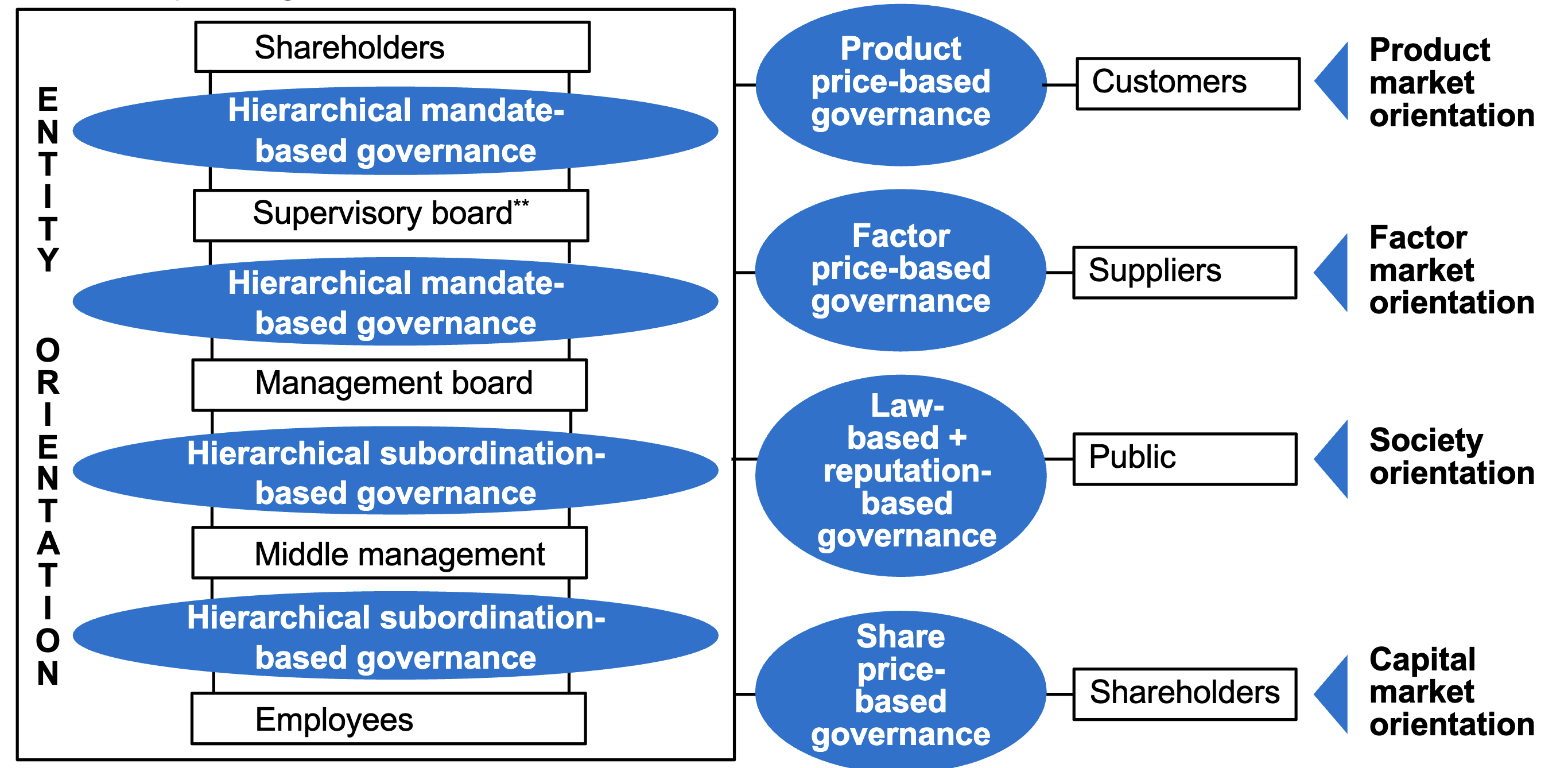

Governance

- Governance mechanisms regulate the relationships between the firm and its stakeholders.

- These mechanisms can be hierarchical (mandate-based or subordination-based), market-based (product or factor price), or based on laws and reputation.

- The firm is an entity that combines stakeholder contributions to achieve its purposes under uncertainty.

(Slide 26)

Principal–Agent Theory

The theory describes how a principal (owner/shareholder) delegates decision-making to an agent (manager) to run the firm on their behalf. With separated ownership and control (managerial view), differences in interests and information asymmetries can lead agents to act not fully in line with owner objectives.

- Governance mechanisms (boards, incentive pay, reporting, control systems) aim to align agent behavior with the principal’s goals and reduce conflicts.

- Agency Costs: Economic losses / additional expenses caused by principal–agent conflicts, including:

- Monitoring costs: Efforts by principals to oversee/control agents (e.g. audits, board oversight, reporting requirements).

- Bonding costs: Commitments by agents to reassure principals (e.g. contracts, share ownership, non-compete clauses).

- Residual loss: Remaining welfare loss when agent decisions still diverge from what would maximize principal value.

Managerial Responses to Stakeholder Pressure

Managers may cope with environmental and stakeholder pressures in different ways:

- Inactive: Ignore signals and continue business as usual.

- Reactive: Respond only when external pressure or crises emerge.

- Proactive: Anticipate trends and adjust early.

- Interactive: Engage stakeholders and co-shape future rules and outcomes.

It’s not helpful to “blame the stakeholder”, deny their legitimacy, or project demands as irrational. Instead, managers should “own” stakeholder problems by accepting their reactions as part of the strategic environment and using their concerns to revise objectives, policies, and governance.